2025 Annual Letter

Most investors will remember this year for the headline number: the S&P 500 up 17.9%. Fewer will remember how close it came to breaking them along the way. A brutal -20% drawdown didn’t just test portfolios; it exposed who had a repeatable process and who was

Most investors will remember this year for the headline number: the S&P 500 up 17.9%. Fewer will remember how close it came to breaking them along the way. A brutal -20% drawdown didn’t just test portfolios; it exposed who had a repeatable process and who was relying on hope, headlines, and luck. Markets like this don’t reward intelligence; they reward preparation, discipline, and emotional control.

This is the first edition of a year-end series where we break down how we navigated the chaos. We break down what we believed when conviction was uncomfortable, how we positioned when risk felt highest, what worked, what didn’t, and what we’re changing going forward. Consider this our official year-end statement, not just on markets, but on how we operate. So let's go.

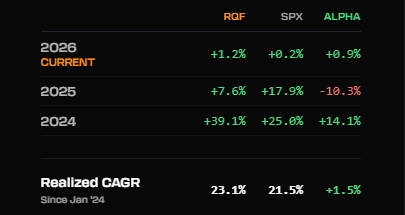

In 2025, our Radar Quant Fund (RQF) finished the year with a return of +7.61%. While that’s below our longer-term expectations, there were several clear drivers behind the slower performance, and just as importantly, several enhancements to our systematic process that came from navigating this environment. Even in a difficult year for systematic trend strategies, we still finished in the green and continue to outperform the S&P 500 since we began tracking RQF live.

The way markets closed out 2025 also felt notably similar to how 2024 ended: a strong equity bull trend eventually shifting into Risk-Off, followed by choppy, whipsaw price action into year-end. What made 2025 especially challenging wasn’t market structure in the traditional sense; it was the speed and frequency of sentiment reversals, many of which were driven by political and policy uncertainty. Rapid headline cycles repeatedly disrupted trend persistence, creating a difficult backdrop for systematic trend-following approaches across the industry, including ours.

Looking ahead, with major tariff and election-driven uncertainty now largely behind us, we believe the environment may become more favorable in 2026, not necessarily because volatility disappears, but because sentiment can form more durably. For systematic strategies, persistence matters, and we expect persistence to improve as markets transition out of a heavily systemic tape-bomb-style politically dominated headline regime.

Let’s take a look at a few of the key trades we made this year, not just to review performance, but to extract lessons that improve the process. Before diving in, it’s important to reflect on what went right, what went wrong, and where our macro regime model (the System) and portfolio strategies can be strengthened. The goal isn’t to overfit to a handful of bad trades. Instead, we want to refine the process around repeatable hedging themes, which are the types of risks that show up across many market regimes. More on that below.

Q1 of 2025: We spent most of the quarter in cash as the System remained Risk-Off and bonds were in a bearish trend, which helped us avoid the worst of the drawdown heading into Liberation Day, with our relative outperformance largely coming from simply not being exposed. That said, shortly after Liberation Day, TLT briefly flipped bullish for about a week, triggering a position that quickly reversed as bonds sold off sharply while global capital rotated away from U.S. duration. The trade was painful, but it exposed a key limitation in our defensive framework, since bonds can fail to function as a reliable haven in certain environments. As a result, we implemented a major robustness upgrade by adding gold as a fallback allocation whenever bonds are not acting as a haven, which does not materially change long-term backtest results outside of the most recent regime, since bonds have historically been the more stable and effective Risk-Off allocation for most of the past two decades. This fallback is not meant to replace bonds, but to hedge a specific future failure mode. In a traditional stress environment, we still expect bonds to behave conventionally, but if stress is driven by U.S. credibility, fiscal sustainability, or de-dollarization dynamics, gold can take the role of the idiosyncratic hedge it was designed to be, and in those circumstances bonds are likely to remain bearish on our DDAP trend model while gold turns bullish, allowing gold to take the defensive allocation slot when it matters most.

🚀 Join the Radar Community

Get free access to MacroBase and notifications about new posts and updates.

Q2 of 2025: During the market recovery in Q2, the System entered a Slowdown regime, which allocated us fully to utilities since both bonds and health care were in bearish trends. This worked exactly as intended, producing a slow but consistent grind higher as the market stabilized and risk began to come off the table. It is easy to view this as an underperformer relative to SPY during a sharp rebound, but the probability of growth rolling back into Risk-Off was still meaningful and could have happened just as quickly. When operating with this degree of leverage, short-term relative underperformance is far less important than preserving capital and maintaining defensive optionality if conditions deteriorate. The protection utilities provided during that transition period were worth the trade-off, and any minor lag can be quickly recovered once stronger trend persistence and higher conviction return, which is exactly what played out in the next trade.

Q3 of 2025: Our favorite regime, Inflation, triggered in early July and quickly brought RQF back from its bond trade drawdown in Q1. Following this pivot, a steadier and persistent stream of gains returned in the market. This was your traditional Risk-On environment where you really wanted to be long risk assets; charts went up and to the right as expected. This regime allowed us to play some catch-up and provided some easy returns up until the early start of Q4. This trade was a testament to how RQF works; any drawdowns seen earlier in the year were quickly wiped out, and any underperformance was hastily made back. Letting the winning trades run while cutting the losers early is key to a successful strategy.

Q4 of 2025: China. That is the simplest way to summarize the quarter. Our macro regime model was already showing meaningful deterioration in early October, with severe strength decay in growth impulses and weakening trend persistence. We were only days away from a natural shift out of Risk-On even without a headline catalyst, and it was unlikely at the time that tariffs would re-emerge in a way that meaningfully disrupted markets. The surprise China tariff headlines simply accelerated what the model was already leaning toward and pushed the regime fully over the edge. One of the more notable flips we made during this stretch was exiting our leveraged Bitcoin exposure shortly after the October 10 tariff tape-bomb, selling into the rebound around $117k. Even as of writing this, Bitcoin remains roughly 20% lower on an unleveraged basis, reinforcing how quickly the risk landscape deteriorated after that inflection point. Defensives were the theme into the end of the year, but things look like they are shifting here early in Q1 of 2026.

The adjustments we made this year can be distilled into a few key inflection points. The first was addressing a future scenario where the U.S. enters a Risk-Off macro regime without the rest of the world, at least initially. In that setup, de-dollarization pressures can intensify, global capital may rotate away from U.S. Treasuries, and gold can become a more effective defensive hedge. The enhancements we made to our defensive allocation framework are designed to hedge precisely these types of regimes going forward.

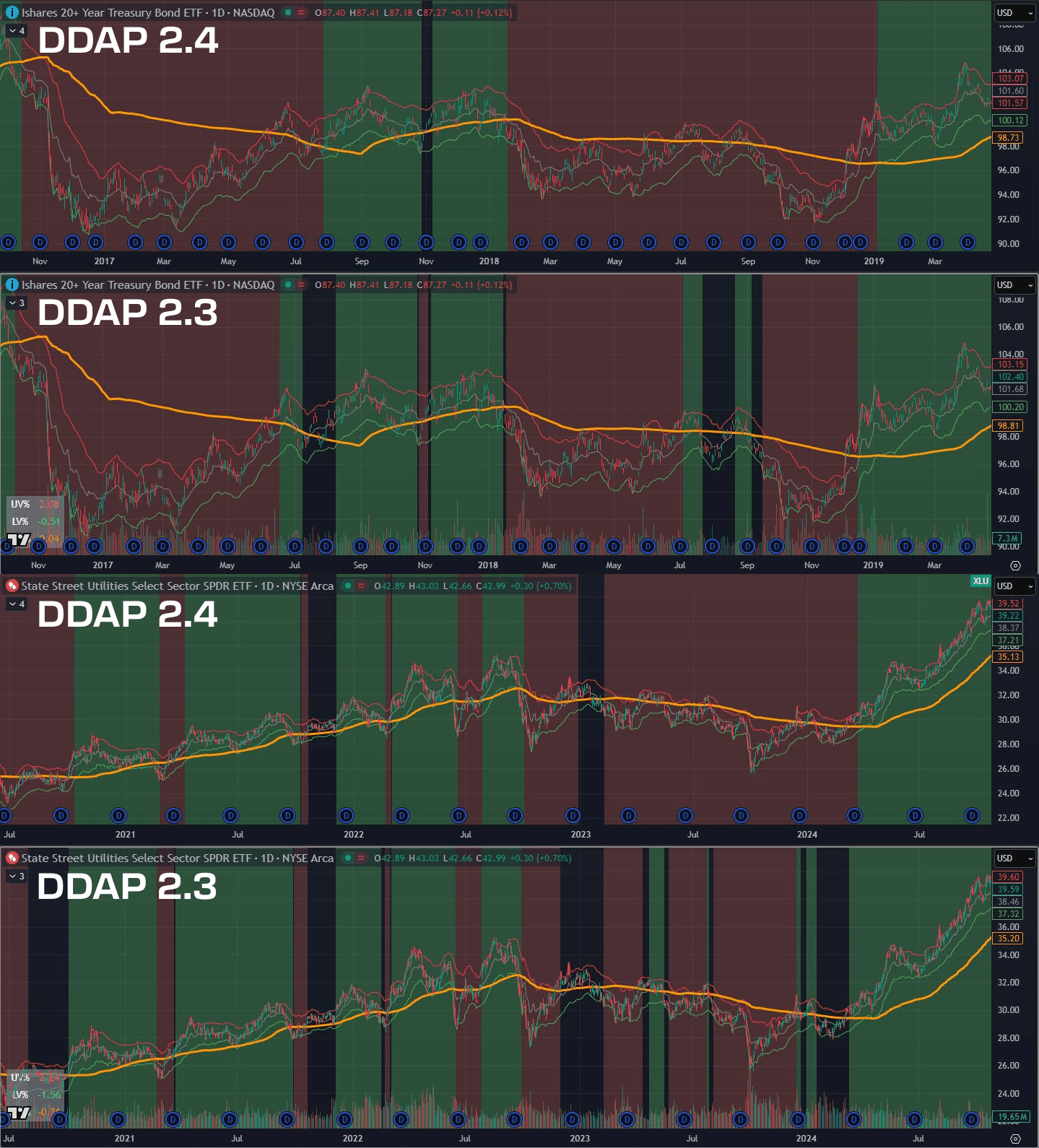

The second major adjustment came in the final stretch of 2025, where we implemented upgrades to our DDAP trend algorithm. These improvements enhance trend state recognition, reduce noise in the process, and allow persistent trends to emerge more cleanly. Taken together, these changes represent a meaningful step forward in system robustness and long-term performance potential. Due to the way we feed trends into our portfolio strategies like RQF, improving trend state recognition led to improvements in volatility-adjusted returns and overall better strategy backtests, which we aim to monetize moving forward.

Here are some examples of the improvements in trend states within our DDAP algorithm:

To everyone who stuck with us through this year of volatility, uncertainty, and hard-earned lessons, we sincerely appreciate you. 2025 was not a year where discipline felt easy, or where systematic approaches worked on autopilot, and we know that can test conviction, especially in a headline-driven market.

But this is exactly why we operate systematically. Our edge is not about winning every quarter. It is about staying consistent through every regime, protecting capital when conditions deteriorate, and compounding through cycles without carrying emotion from one period into the next. Most importantly, while 2025 lagged the index, RQF continues to outperform the S&P 500 since we began tracking live results, and we believe the refinements made this year meaningfully improve our long-term performance potential. If you are a long-term investor looking for process, discipline, and an edge built to persist across regimes, this is exactly what Market Radar was built for. We look forward to going through all the challenges and successes 2026 has to offer with every one of you; none of this would have been possible without this incredible community.