Bullish Risk-Off - 7.01.2024

OVERVIEW Navigating the current economic landscape can feel like deciphering an intricate puzzle. As we transition into a Risk-Off environment amidst the onset of a Stagflation regime, the stakes are high and the signals mixed. Unlike the severe stagflation of

OVERVIEW

Navigating the current economic landscape can feel like deciphering an intricate puzzle. As we transition into a Risk-Off environment amidst the onset of a Stagflation regime, the stakes are high and the signals mixed. Unlike the severe stagflation of the 1980s, today's landscape presents a unique set of challenges and opportunities. Our System has switched gears, highlighting the importance of adapting to these nuanced conditions. We delve into the complexities of the current economic climate, the performance of equity indices, and the strategic decisions guiding the Radar Quant Fund. We'll also explore specific stock plays like Rivian, offering a detailed outlook on how to navigate these turbulent times.

THE SYSTEM

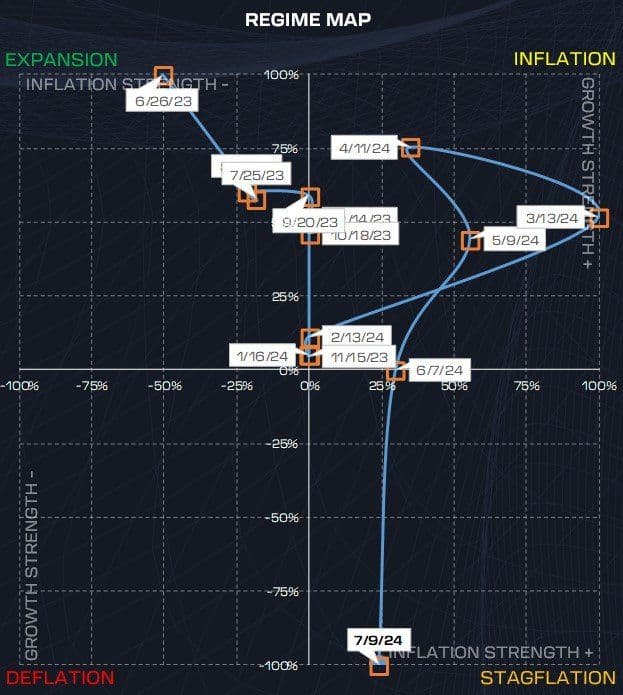

The System has officially switched to Risk-Off after entering the Stagflation regime. The regime is characterized by positive inflation and negative growth pressures. Typically, the term "Stagflation" brings to mind the extreme conditions of the 1980s. It's important to note that not all periods of Stagflation are as severe. Over the last 20 years, the System has displayed many Stagflation regimes that don't come with those severe conditions. We’re also at the junction where an acceleration in disinflation that lacks any acceleration in growth strength opens the door for the possibility of a Deflation regime. Although the System indicates we're in a Risk-Off environment, we’re seeing some nuances with this regime that we’ll go through in the OUTLOOK section below!

OUTLOOK

Risk-Off is here with some caveats. It might seem like we're giving off mixed signals in our public commentary. So let's explore what exactly is sticking out. Currently, the System is signaling a Risk-Off environment, but if we look below, the equity markets display something completely different. Coupling this with the economic data some exceptions start emerging.

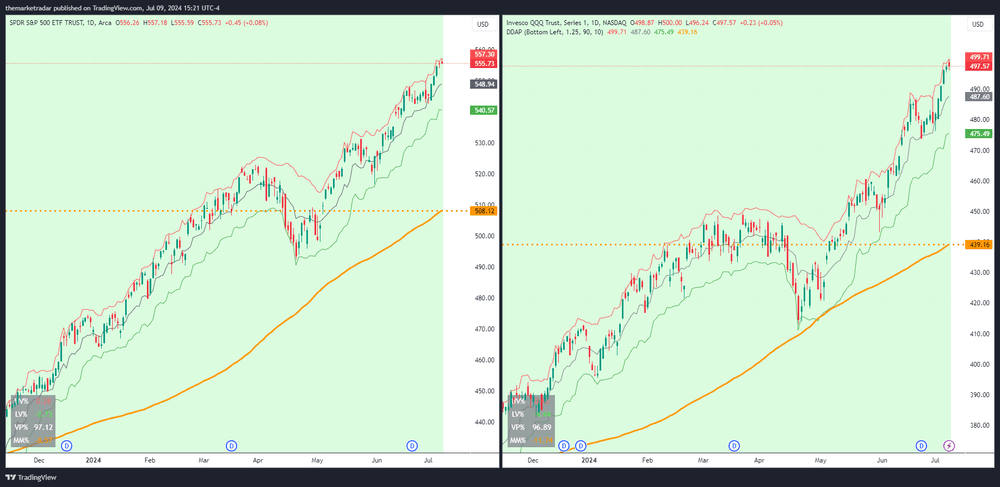

The equity indices are obviously in a bullish trend. If you couldn't tell already, there's nothing bearish about a bullish trend. Historically, we've seen the System pivot ahead of the market, so there is some sense in having caution despite the equity indices in a bullish trend. In a typical Risk-Off environment, we expect bonds to outperform equities. Most know these periods to be where equities and bonds have a negative correlation, with equities going down and bonds going up.

As of writing this both indices are quite extended and have over 10% downside to MOMO. There's a lot of damage that needs to be done here first before we even see bearish trends on both of these indices. There may be a good reason for this given the economic conditions we’re seeing at the moment.

The economy has been slowing for a short while now. However, there is a difference between slowing and declining. For instance, the labor market is weakening, but doing so from historically low levels. Similarly, real GDP has shifted from 3-to-4 percent to 1-to-2 percent. These new ranges are weaker than before but still acceptable. What stands out about all of this is how we're approaching the commencement of a rate-cutting cycle, but we're not in a recession yet. We believe the Fed should have begun its cutting cycle, but this is where we are now, and we're still not in a recession. This means there's still a slim chance that the slowdown ends in a slowdown and re-accelerates from there, coupled with rate cuts. It would look something like this:

🚀 Join the Radar Community

Get free access to MacroBase and notifications about new posts and updates.

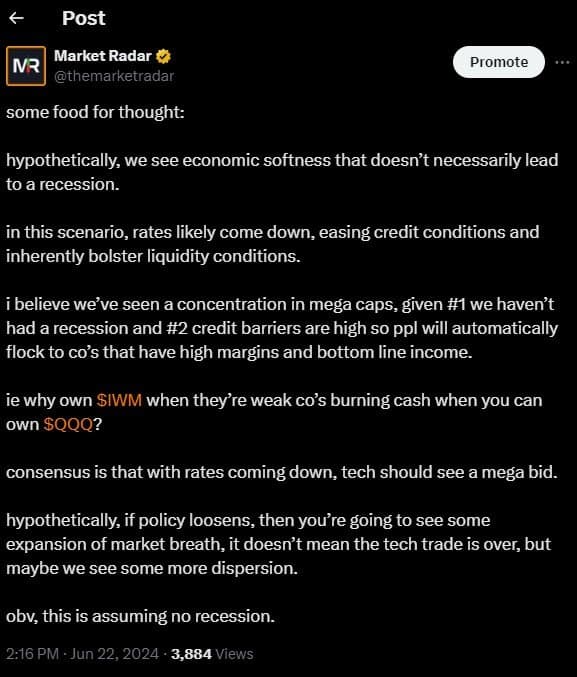

The problem with this? We need to see the Fed think ahead of the curve. Remember, their policy actions have lags that are essentially unquantifiable. If we see the signs of a slowdown now, it would be nearly impossible for the Fed to catch up unless cuts were already underway. The Fed doesn’t seem too concerned about the current slowdown as they're overly focused on not moving rates down too quickly reigniting inflation. Sounds complicated, right? That's because it is. This sort of “no recession resolution” could happen, where the Fed reduces policy allowing the economy to re-accelerate and our System flipping back into a Risk-On environment. We remain on watch for any indications of these possibilities becoming a reality.

With our System recently coming from a Risk-On regime we’ve spent nearly the entire year in equities, Bitcoin, and short volatility. Some may be reading this thinking, "Why not just hold both bonds and equities if things seem to be on the right track?" After all, equity indices are still trending bullishly. Our answer lies within what we’ve experienced as the path of least resistance and greatest outcomes. Ares, which makes up 60% of the RQF, was designed to execute a repeatable process, not one that is opaque and may work phenomenally under rare conditions. The System has historically provided great warning signs of what is ahead, the easiest path is to go with the regime and leave the complication at the door. We hope the current situation resolves itself smoothly, hopefully avoiding a recession. We’d rather be wrong on the Risk-Off call and have to buy back into equities than see a recession materialize. We are long-term equity and Bitcoin bulls anyway, and we hope to be back on those wagons soon!

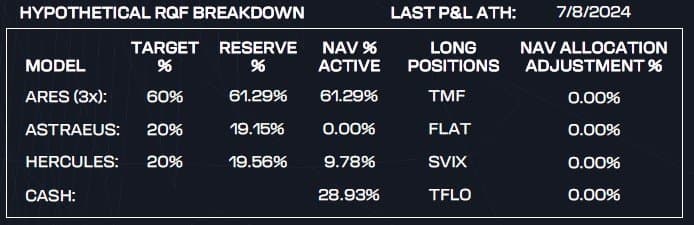

RADAR QUANT FUND (RQF)

The RQF is currently positioned heavily long in US Treasury bonds and partially short on U.S. equity volatility. We’ve also flattened our Bitcoin position after successfully riding the wave from $43k to $63k in 2024. It always saddens us to let go of Risk-On assets, but that’s the nature of the game—we must respect the conditions at hand.

The RQF made new all-time highs earlier this week and currently holds nearly a quarter of its NAV in cash. We expect bonds to outperform equities throughout this Risk-Off regime with times when bonds may seem undesirable with equities near all-time highs. Although we’re in a Risk-Off environment, Hercules continues to take advantage of the volatility landscape in equities. Likely, Hercules would end up closing the rest of the short volatility position if liquidity conditions in the United States were to show signs of decaying further.

The RQF operates on a 100% systematic basis. Despite our views on market conditions, we stick strictly to our investment strategy. Missing small moves in the short term is generally outweighed by the gains of longer-term trends. We remain committed to navigating these cycles, capitalizing on opportunities, and riding the waves as they come.

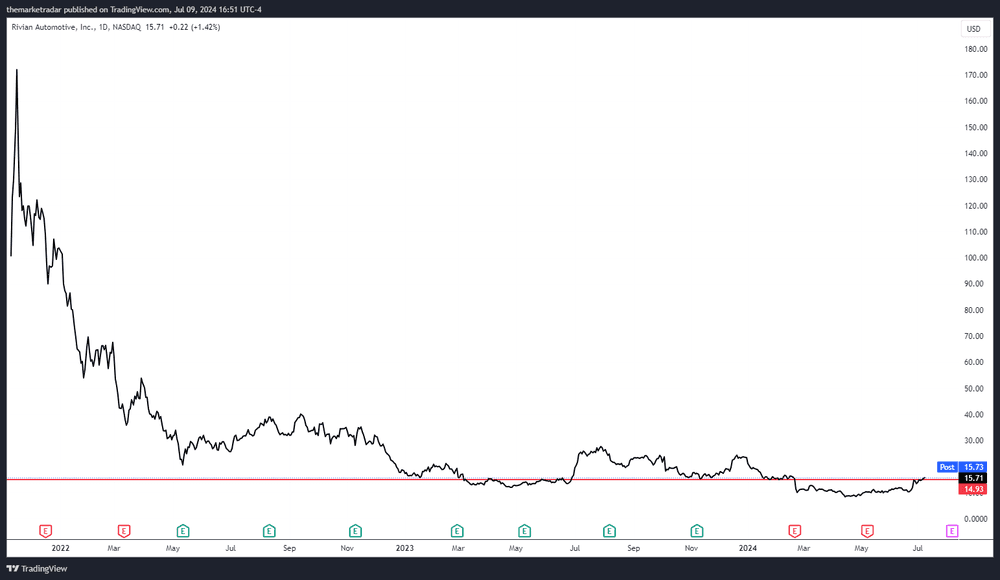

RIVIAN

We started covering Rivian in Q4 of 2023, around $15/share and we formally laid out our thesis in the prior ledger note which can be foundHERE.

Since the prior ledger note, Rivian is up roughly 55%+ from the $10/share market to nearly $16/share. We own Rivian around $15/share and we’ve seen the price recover nicely since Q1 of this year. This has been a fundamental play for us from the beginning, exempting it from some of the economic and momentum conditions we’ve explained throughout this post. We’re aware that if we tip into a recession, Rivian’s stock price likely will not bode too well, but we’re buying it today under a long-term vision as a real EV alternate to the behemoth Tesla. If we were to experience a recession, and Rivian were to display improved liquidity and fundamental conditions at that time, we’d likely be open to adding to our position.

Recently, it was also announced they would be conducting a joint venture with Volkswagen, and this is great news for the company as it comes with some fresh capital. While all the capital is not directly accessible, this update essentially acts as an equity offering with perks that investors don’t necessarily look that negatively at. Our thesis around this company remains mostly unchanged. The additional capital is welcomed alongside management reaffirming their positive Q4 gross margins target, which should drastically reduce cash burn. We believe the lower the odds Rivian needs to issue sizeable debt to make it to the R2 production ramp-up, the more favorable the company will trade. We do however think it’s still possible they issue debt as they through the R2 lines production, but from what the market has been telling us, the biggest fear has been the company making it to the point where they produce the R2 vehicles and fulfill orders, which seems to become clearer in a positive way.