Inflation, Credit, and Rates A Turning Point

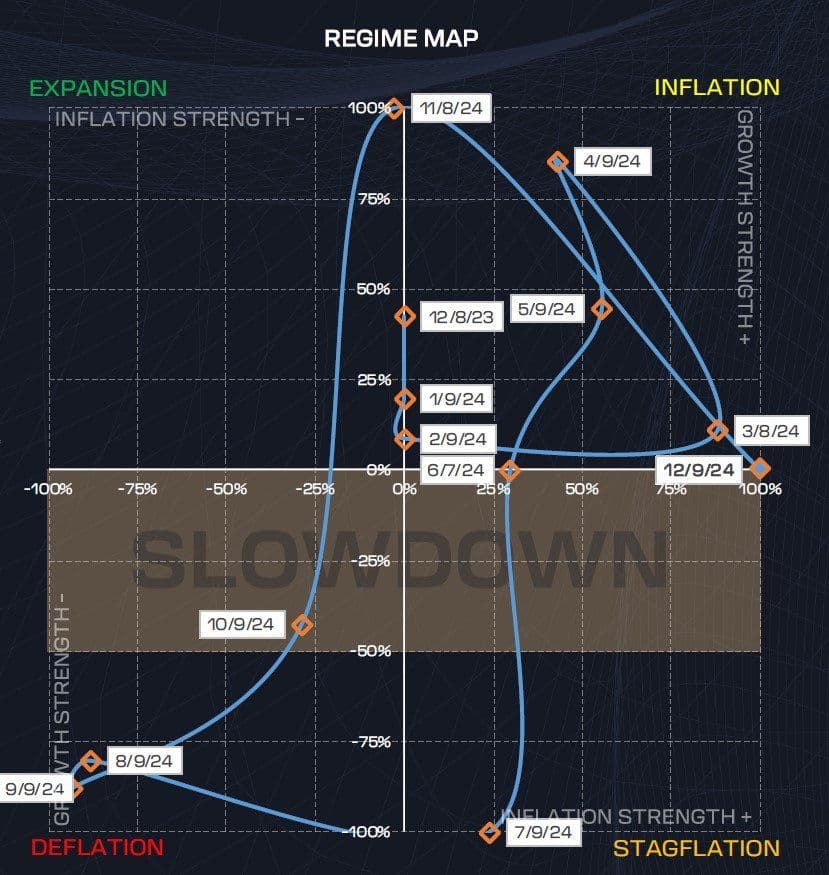

THE SYSTEM We’re observing a noticeable acceleration in inflationary pressures across the System. Over recent weeks, growth strength has churned at persistently low levels, while inflation strength has gained momentum. The market remains sensitive to inflation

THE SYSTEM

We’re observing a noticeable acceleration in inflationary pressures across the System. Over recent weeks, growth strength has churned at persistently low levels, while inflation strength has gained momentum. The market remains sensitive to inflation narratives, likely due to residual apprehension from the post-COVID inflationary surge. Early indicators suggest an increasing likelihood of transitioning entirely to an Inflation regime (positive growth, positive inflation strength) or a Stagflation regime (negative growth, positive inflation strength).

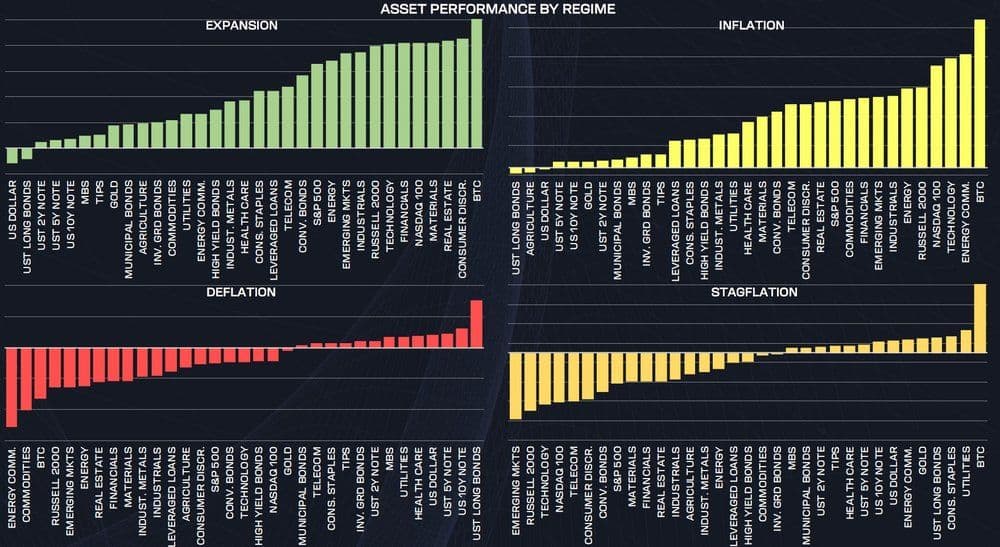

To clarify: the term “Inflation regime” often carries an alarmist undertone, but history shows these regimes aren’t necessarily synonymous with runaway inflation. For example, we’ve seen Inflation regimes in the past decade with CPI levels comfortably under 3%. The System could simply be identifying a slowdown in disinflationary momentum—less “inflation ripping,” and more of a pause in downward pricing pressures. However, a more compelling shift in disinflationary forces would require stronger signals, such as $GSG entering a bullish trend. Remember, an Inflation regime is very bullish for risk assets. However, a Stagflation regime is quite the opposite.

Looking ahead, the data suggests an evolving risk landscape. Growth strength is flatlining, while inflation strength builds. While our approach remains systematic—acting purely on the signals—the System has historically hinted at subtle shifts before they’re fully reflected in the print. One emerging risk is a potential transition to a Slowdown regime style. It’s important to emphasize that slowdowns are distinct from recessions. Practically, we might experience a consolidation in growth expectations before any re-acceleration.

Here’s the breakdown of regime style thresholds:

- Growth strength above 0%: Risk-On (Expansion / Inflation Regimes)

- Between 0% and -50%: Slowdown (Stagflation / Deflation Regimes)

- Below -50%: Risk-Off (Stagflation / Deflation Regimes)

Note: A Slowdown regime style shares characteristics from Risk-On and Risk-Off. We find defensive positioning tends to work best in that environment.

The current growth score hovering around 0% suggests the potential for a Slowdown. Prolonged stagnation here after declining from higher Risk-On levels increases the likelihood of defensive repositioning. For those in crypto: allocations to Bitcoin are unlikely to shift significantly unless we see growth strength plunge below -50% for an extended period.

For added macro context, the Atlanta Fed’s GDPNow forecast stands at 3.3% for Q4—a strong print. However, our focus remains forward-looking. If real GDP estimates for Q1 2025 taper to ~2.0%, while still healthy, it could signal further deceleration risks for growth. The System’s strength lies in identifying these shifts ahead of the broader market. As always, our positioning will adapt precisely and without bias as the data unfolds.

MACRO

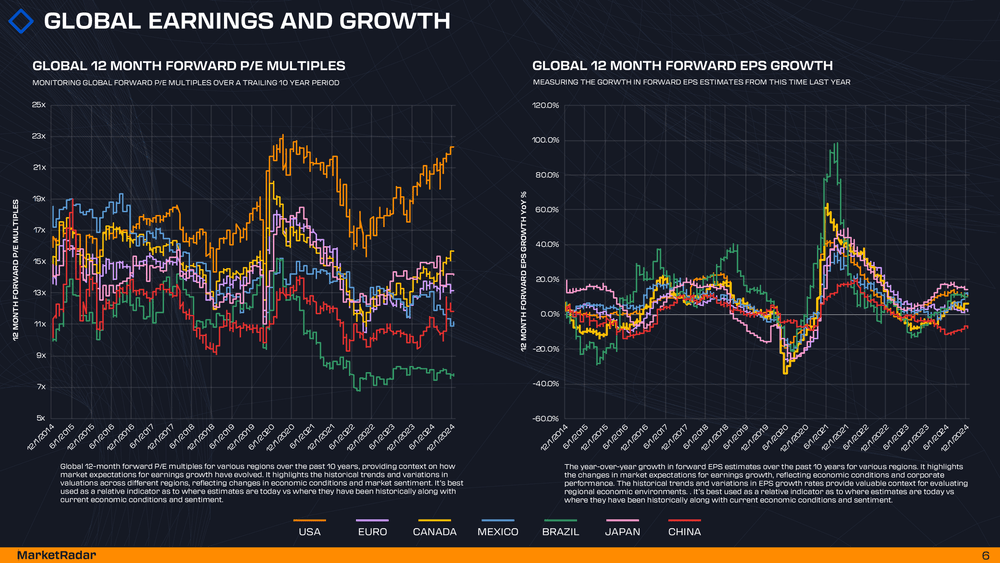

Price-to-Earnings

Let’s begin with an analysis of global forward price-to-earnings (P/E) estimates. As we head into the end of the year, in the United States, forward P/E estimates are currently at or near the peak levels we saw in 2021—a period characterized by a ZIRP (zero interest rate policy) environment. While I wouldn’t outright dismiss these multiples as expensive, the current setup leaves us with three potential paths forward:

Multiples continue to expand, making valuations even richer.

🚀 Join the Radar Community

Get free access to MacroBase and notifications about new posts and updates.

Prices fall relative to earnings, bringing multiples down.

Earnings accelerate beyond expectations, helping normalize multiples without a price contraction.

Ultimately, either P (price) or E (earnings) expectations need to adjust to restore balance.

At first glance, it’s easy to label the U.S. market as overvalued compared to the rest of the world, given its higher multiples. And that’s 100% accurate. But in my opinion, this isn’t inherently a red flag. Higher valuations are justified when considering the strength of the U.S. economy and the technological innovation it fosters—after all, quality comes at a premium.

That said, a deeper look at implied earnings growth—the “E” in P/E—offers an interesting perspective. Current market forecasts suggest much lower earnings growth rates than we saw in 2021. The silver lining here is that there’s room for these growth estimates to rise, which could offset price increases and ease P/E multiples without necessitating a sharp price contraction. Interestingly, forward earnings growth rates today are also below the levels seen in the pre-COVID 2018 period.

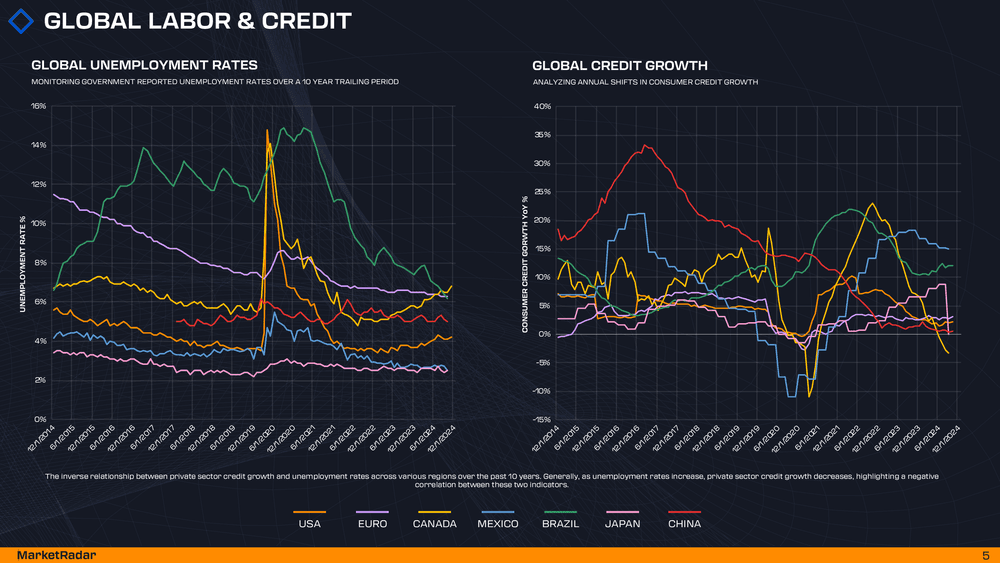

Credit Growth

As noted earlier, disinflationary trends are facing resistance, as highlighted by our System. One key factor I’m closely monitoring is credit growth. Currently, U.S. credit growth is trending below 2018 levels and significantly lower than the post-COVID environment. For inflation to meaningfully break away from its disinflationary trajectory, I believe we’d need to see a substantial acceleration in credit growth, particularly in the United States. Without that, what we’re observing may simply reflect a transitory pause in the broader disinflation trend.

Globally, the landscape varies. The United States appears relatively balanced, while Brazil and Japan continue on hawkish monetary paths as credit growth remains elevated. Meanwhile, Canada is experiencing outright credit contractions and persistent dovish monetary policy.

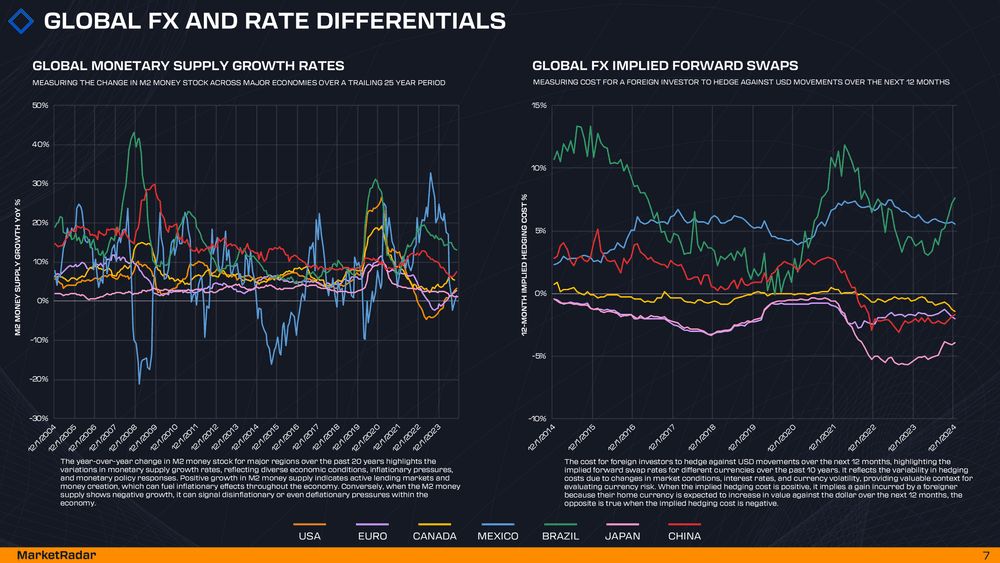

Rate Differentials

Over recent months, we’ve seen rate differentials narrow between CAD and EUR implied forward swaps relative to the USD. The Canadian dollar, in particular, seems to be drifting further into “carry currency” territory. With the Fed’s forward guidance likely to take center stage soon—next week’s FOMC meeting and the release of the dot plot alongside the SEP could add clarity—rate expectations in the U.S. could shift more hawkishly than in other countries.

The implications for carry trades are significant. A strong rate differential in favor of the U.S., coupled with robust dollar fiscal policies on the horizon, reinforces the dollar’s dominance. Despite the noise around BRICS, the reality remains clear: the dollar is—and will remain—the global reserve king.

OUTLOOK

Our macro outlook remains a cornerstone of the System. Growth strength in our signals currently exhibits very low confidence, with persistent labor market weaknesses—evidenced by a rising unemployment rate—elevated P/E ratios, and muted growth estimates.

As it stands, our allocation remains Risk-On, but it’s critical to stay nimble. Any number of signals could tip us into a more defensive posture. While we would love to remain Risk-On, remember that emotions have no place in decision-making. Stick to the signals, stay prepared, and don’t hesitate to pull the next trigger when the data demands it.