Is The Bull Run Over - 05.08.24

OVERVIEW As we approach the midpoint of the year, with equity indices having pulled back off all-time highs and the ongoing tug-of-war between bulls and bears, it's crucial to assess the market from a data-driven perspective. Let's examine the current readings

OVERVIEW

As we approach the midpoint of the year, with equity indices having pulled back off all-time highs and the ongoing tug-of-war between bulls and bears, it's crucial to assess the market from a data-driven perspective. Let's examine the current readings from our System, identify any discrepancies, highlight areas that are performing well, and discuss our expectations for the upcoming quarters. We will also review the performance of the RQF, pinpointing potential weaknesses and strengths that may emerge. To conclude, we will provide a formal recap of Rivian, a company we've touched upon in our podcasts but have yet to introduce thoroughly.

THE SYSTEM

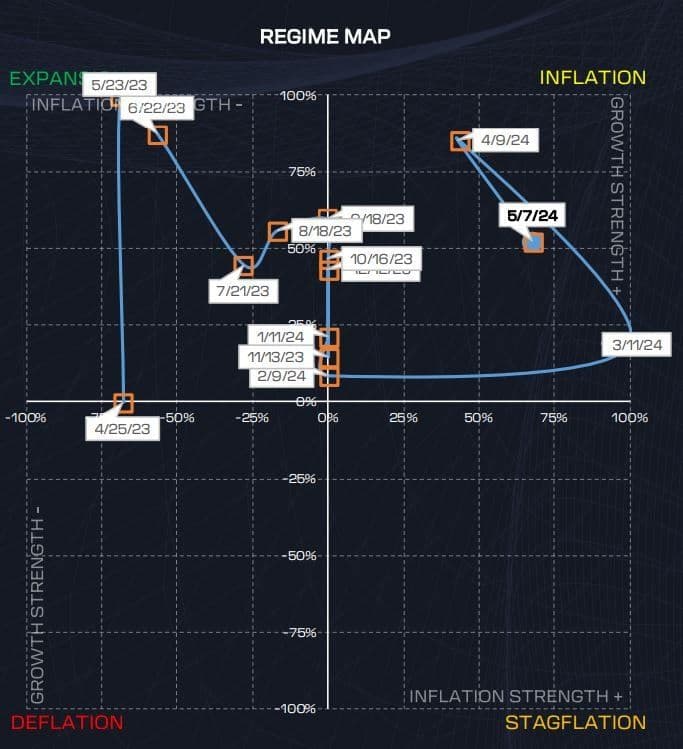

As you're aware, our system entered the year in a Risk-On regime, signaling strong momentum throughout. We're currently navigating the INFLATION regime, characterized by persistently moderate yet sticky inflation, alongside robust economic growth. While we've experienced some shifts between stronger and weaker INFLATION regime dynamics, I'm beginning to sense a possible transition toward the EXPANSION regime soon.

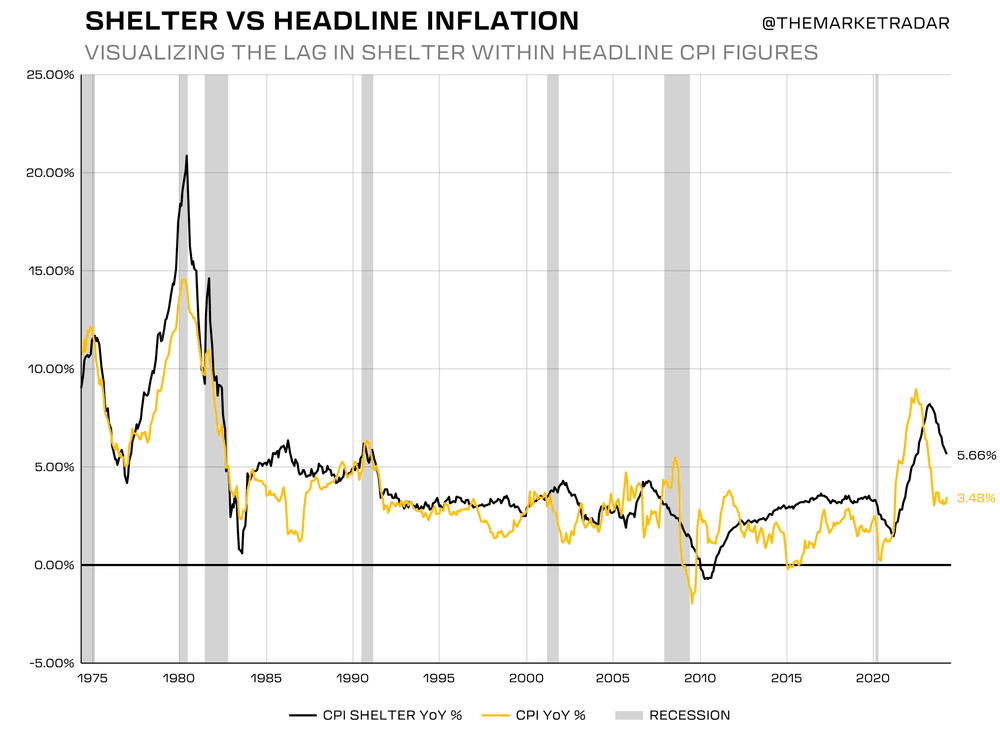

As we know, base effects in commodities start working against the higher inflation narrative into the second half of this year, coupled with the continued decline in shelter, I have a feeling disinflation is going to kick back into action. We know that the official shelter figures lag actual shelter costs indicated by more real-time indicators by at least 6 months. This emergence of disinflation could act as a driver for additional policy dovishness. At Market Radar, however, we don't preemptively act on predictions; we wait for clear signals to guide our strategies.

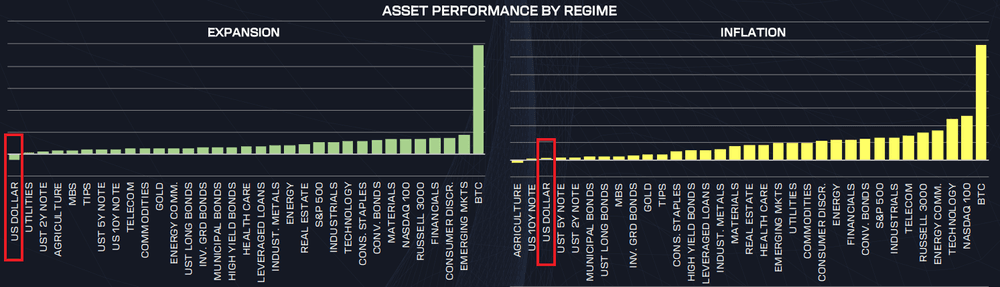

This year, most of our time has been spent in the INFLATION regime, occasionally teetering on the edge of EXPANSION. Both scenarios favor risk assets. Typically, the INFLATION regime boosts risk assets, but this year has proved atypical, especially for small caps. Contrary to usual trends, small caps haven't benefited from the usual tailwinds within this regime, primarily due to many small cap companies either stagnating or facing negative earnings growth in a high-interest rate environment. This has led to continued bullish trends and higher prices in larger cap indices, driven not just by standout performers like Nvidia.

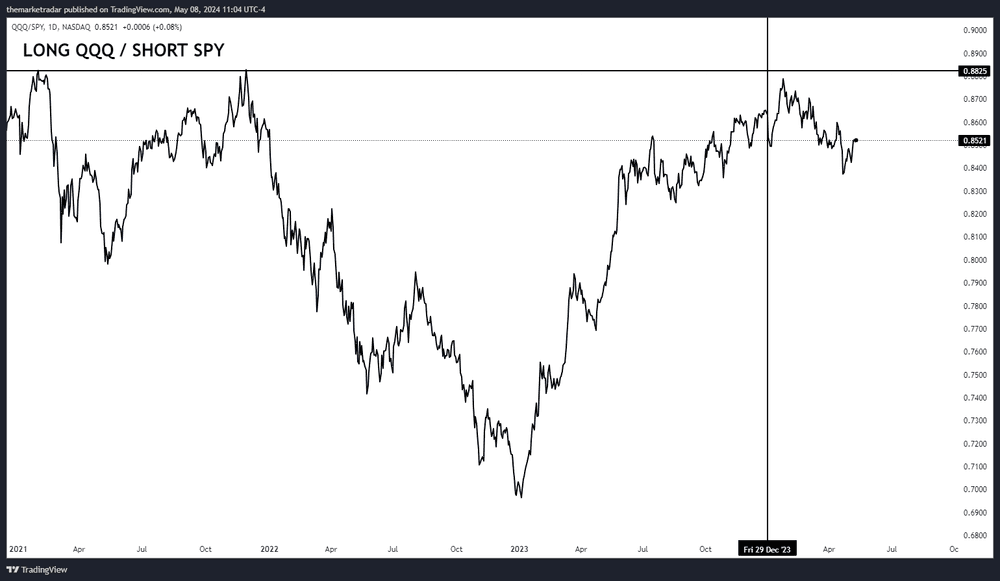

Interestingly, since the beginning of the year, there has been notable underperformance in the Nasdaq-100 and technology sector compared to the S&P 500—unusual for a Risk-On regime. If this regime maintains its course with continued growth and moderating inflation, I anticipate a correction in this trend, potentially leading to new highs for the Nasdaq-100 relative to the S&P 500.

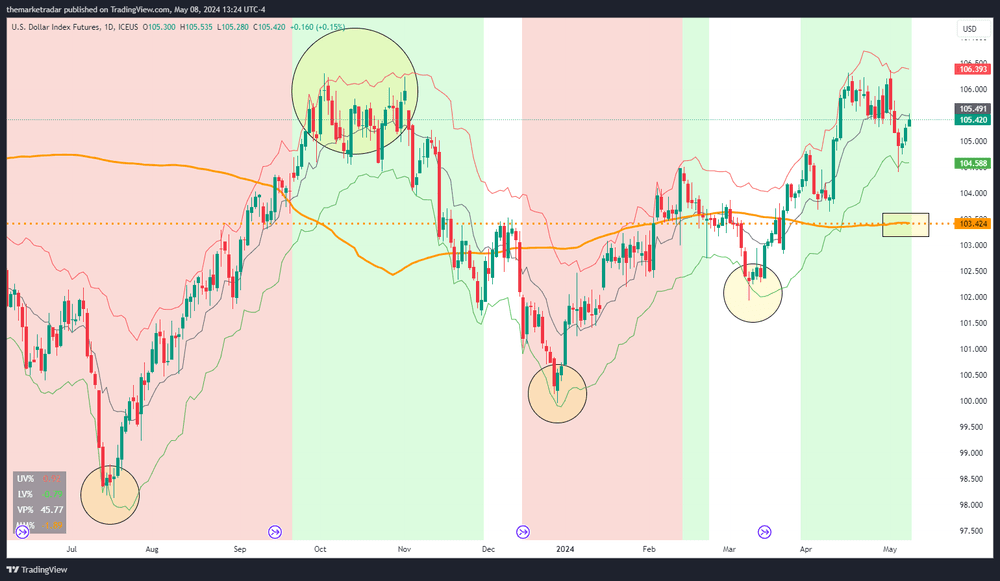

Lately, the resilience of the US dollar has been noteworthy. This strength likely stems from the expanding real rate differential between the United States and other countries, coupled with the weakening Japanese Yen due to the Bank of Japan's dovish stance. Generally, a stronger dollar is not seen as a favorable indicator in Risk-On environments, and it is typically expected to underperform in such market regimes.

The dollar has shown strength throughout the year, maintaining either a bullish or neutral trend. Currently, it is trading below the mid-VAMP level, but the outlook remains positive unless it falls below the momo indicator, which could signal further challenges for equities.

🚀 Join the Radar Community

Get free access to MacroBase and notifications about new posts and updates.

Despite the robust trend, there's a possibility that the dollar could weaken, potentially influenced by more dovish expectations for future monetary policy. Presently, Fed Funds futures are pricing in a 100% probability of one rate cut and a 75% chance of a second cut in 2024. The latest Federal Reserve dot plots suggest three rate cuts this year, though this forecast could shift at the next FOMC meeting.

Additional hawkish pressures are apparent in the market, exceeding the one-cut discrepancy between the dot plots and Fed Funds futures expectations. The market remains tight through 2025, likely reflecting anticipation of the Federal Reserve's initial rate cut. Once the Fed begins to reduce rates, we could see a relaxation in market conditions, signaling a shift towards easier monetary policy. This shift is expected to reduce demand for the dollar, as the real rate differentials between shorter and medium-term durations diminish.

RQF (Radar Quant Fund)

So far this year, our performance has been modest. Although the RQF has outperformed the S&P 500 by over 200 basis points year-to-date, this margin isn't our primary goal. Much of this performance stems from the underwhelming results in the technology sector this year. The RQF is heavily invested in TQQQ, which is a triple-leveraged ETF of the QQQ. If the current risk environment persists, there is potential for technology stocks to regain their leadership position and recover some of their losses relative to the S&P 500 this year.

Additionally, our strategy has been affected by poor returns in the short volatility trade. The RQF also invests in SVIX, an inverse volatility ETF. The volatility landscape in the first quarter showed an unusual pattern where higher volatility on market up days erased much of the gains typically expected from being short volatility. This situation adversely impacted our profits. However, recent market corrections and a rise in the VIX to 20 may help to stabilize this as the market dynamics recalibrate and realized volatility adjusts.

Bitcoin has performed well this year. We entered our RQF position during the pullback that followed the ETF approvals early in 2024 at around $40,000 per coin. It has been a favorable investment thus far, supported by a risk-on market environment. We anticipate continued bullish trends as long as they align with our systematic trading regime.

Ultimately, the RQF operates on a 100% systematic basis. Regardless of our personal views on market conditions, we adhere strictly to our investment strategy. Short-term adjustments are generally outweighed by long-term trends. We remain committed to navigating these cycles and capitalizing on opportunities and ride the waves as they roll in.

RIVIAN

We initiated coverage of Rivian (RIVN) in Q4 2023 when the stock was trading around $17 per share. Since then, the price has fluctuated, reaching as high as $24 and dropping to a low of $8, and is now approximately $10. My average purchase price is around $15. This investment differs significantly from the strategies outlined in the RQF and is not typically included in our regular reporting. We've sized this position so that if Rivian becomes a major player, it will provide a notable boost to our net asset value (NAV); however, if it fails to progress, the impact will be minimal.

The investment thesis for Rivian remains largely unchanged, despite some adjustments in company guidance and a rise in long-term rates since we started discussing the company. Among EV manufacturers, Rivian has a strong potential to capture market share, even from Tesla. Currently, the EV market is undervalued, impacted by high interest rates, the high cost of EVs compared to internal combustion engine vehicles, and reduced gas prices. Despite producing impressive revenue figures compared to its peers, Rivian is still unprofitable. In the current high-rate environment, cash-burning companies are generally not valued highly in the market.

Rivian aims to continue to produce over 50,000 vehicles annually and expects to become gross margin positive by the end of 2024. With new mass-market models like the R2 on the horizon, Rivian could establish itself as a profitable EV manufacturer if it navigates the scale-up phase successfully. Currently trading close to book value, this metric is less relevant since the company is unprofitable and will likely see a decline in book value until it achieves profitability, there isn’t much premium in the name. Rivian has over $7 billion in cash and access to up to $9 billion in total liquidity, spending about $1.5 billion per quarter. There's a chance it might issue new stock or convertible preferred equity to fund operations until it reaches its production ramp-up for the R2, scheduled for 2026. Achieving positive gross margins by the end of 2024 could significantly reduce its burn rate, extending its financial runway and potentially diminishing the need for a substantial capital raise.

SUMMARY

As we progress through 2024, Market Radar has observed a fluctuating investment climate, primarily within the INFLATION regime, with occasional shifts towards EXPANSION. This environment has uniquely affected asset classes, notably underperforming small caps and a strong, albeit atypically behaving, US dollar. Our Radar Quant Fund (RQF) has modestly outperformed the S&P 500, driven by diverse strategies including heavy investments in technology through TQQQ, handling market volatility with SVIX, and promising performance from Bitcoin. Our small strategic investment in Rivian reflects a cautious yet optimistic outlook on the EV market, positioning us to leverage potential market shifts while managing risks conservatively. As always, we remain committed and most focused on our systematic investment approach, ready to adapt to market signals and trends.