Respect the Lag - 08.10.23

OVERVIEW: With the stock market well off the 52-week lows, many market participants are raising concerns that the Fed isn't nearly restrictive enough for the current economic environment. There is also some discussion going around about there being fewer lags

OVERVIEW:

With the stock market well off the 52-week lows, many market participants are raising concerns that the Fed isn't nearly restrictive enough for the current economic environment. There is also some discussion going around about there being fewer lags in monetary policy than those historically observed. In my humble opinion, this is macro monkey bullshit. Before we dive into today's current macro situation, let's understand what the Fed has already done.

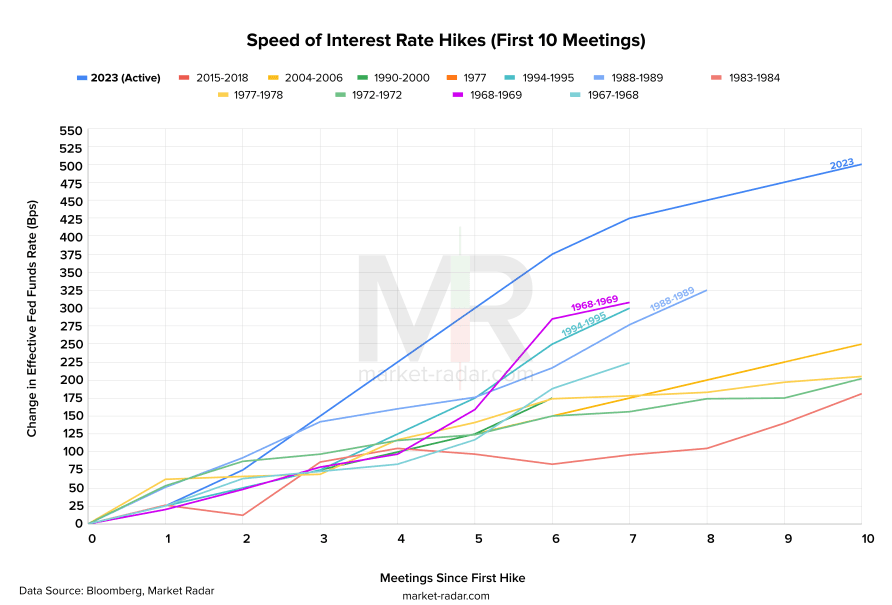

The current hiking cycle (2023) is the fastest in terms of percentage points added to the Federal Funds rate in the prior 50 years. It's commonly understood that the Fed was late to lift policy in 2022 and could have done so well into 2021. Nonetheless, it’s clear as day that once they lifted...they lifted firmly without messing around.

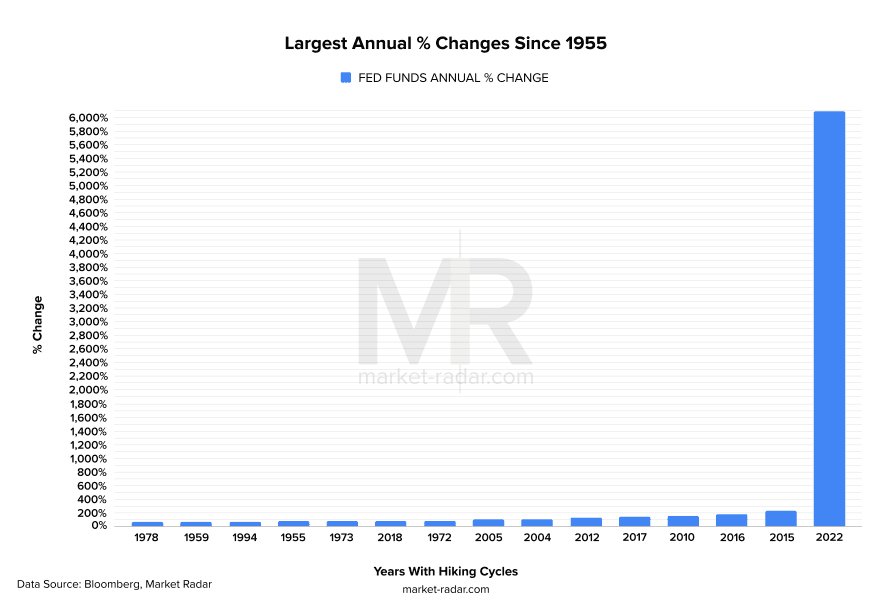

Not only is this hiking cycle titled the "fastest", but it's also titled the most "explosive" in the prior 50 years. On an annual rate of change basis, the Fed Funds Rate was lifted over 6,000% in 2022. The second on the list is not even close at 233% YoY in 2015!

CURRENT CONDITIONS:

Fed Conditions

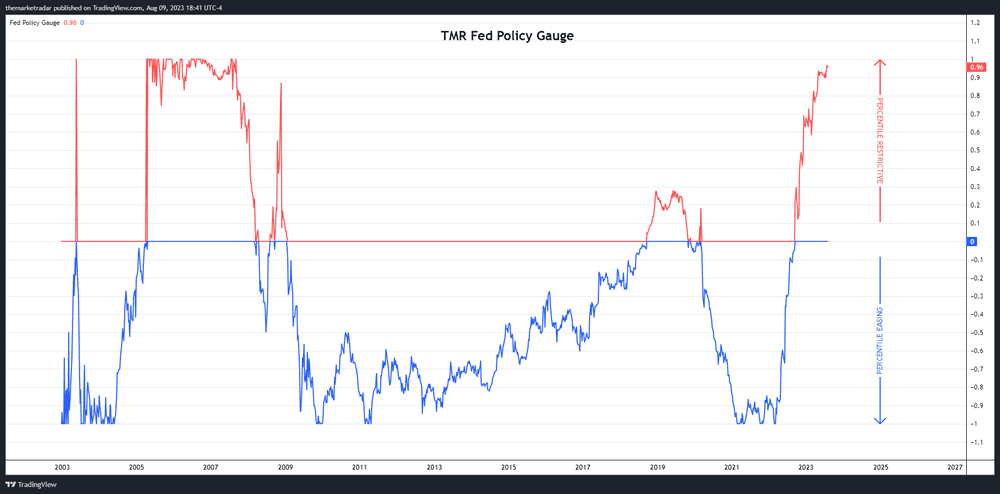

Our Fed Policy Gauge is in the 96th percentile of restrictiveness going back to 2003. Despite claims of easing conditions, the Fed is very restrictive in regard to forward inflation expectations. With the Fed merely holding rates here and inflation expectations becoming more controlled, the real policy at the Fed will continue to expand...adding further restrictiveness to the economy.

TOO LOOSE?:

Out of all the data points making their rounds on the internet, it seems that GDP and Unemployment are two of the main drivers behind the narrative that the Fed isn't restrictive enough...and this economy warrants way more rate hikes.

GDP

As you can see, the Atlanta Fed GDPNow model has GDP estimates for the quarter well above consensus. This is basically alluding to an ACCELERATION in the economy. The argument here is that GDP accelerating will only put upward pressure on inflation...meaning the Fed isn't restrictive enough.

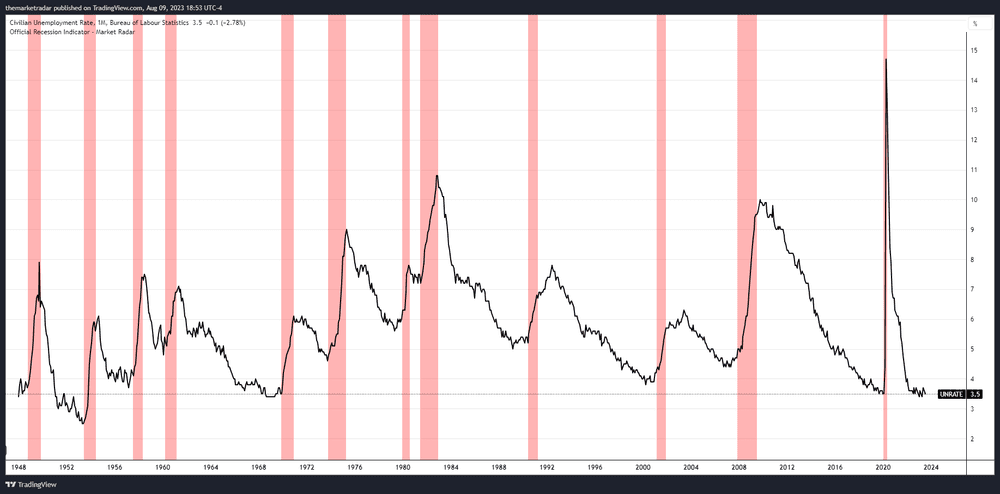

Unemployment

🚀 Join the Radar Community

Get free access to MacroBase and notifications about new posts and updates.

The Unemployment Rate has gone absolutely nowhere since the Fed lifted off in Q1 of 2022. This is a primary driver in FOMC headlines and market participant narratives on the Fed not being restrictive enough. Again, the argument being made here for further hikes is lower unemployment will continue to fuel demand in the labor market for higher prices of goods (further inflation).

POLICY LAGS:

So we've gone over what the Fed has done, how the market sees the Fed's current policy, and what the economy continues to do despite all of this. The main question being raised here is the validity of policy lags and if they even apply anymore. We've even heard Powell claim that policy actions move much quicker in modern times with instant news distribution and advanced derivatives that pickup and price forward expectations almost instantly.

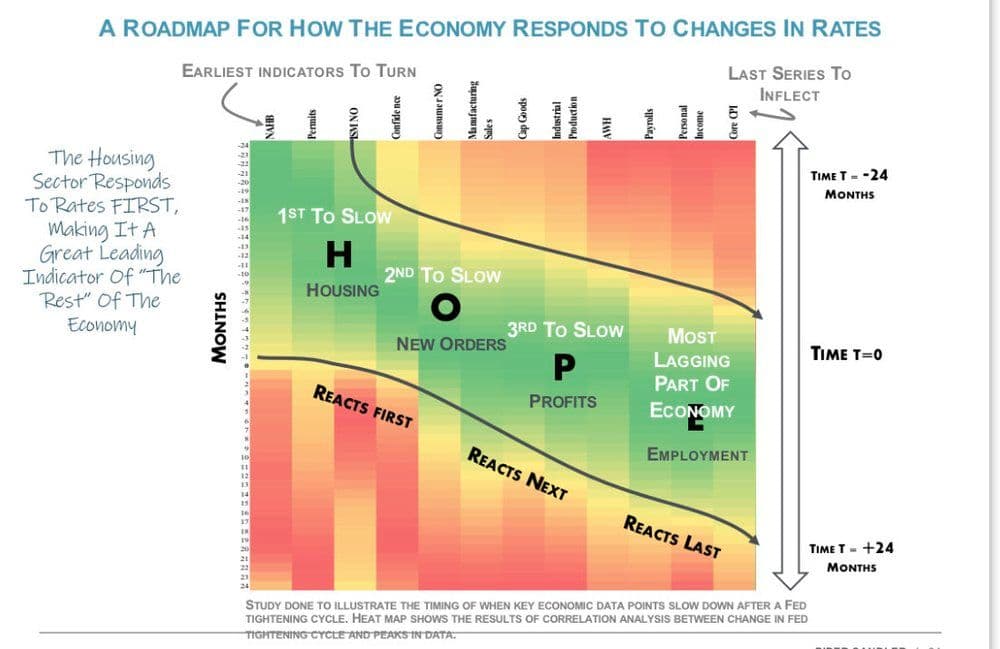

There has been a ton of research conducted on the policy lags of the Federal Reserve and typically a range between 18 to 24 months is seen as a referenced figure for the expected lag in tightening cycles. Michael Kantro, CIO at Piper Sandler, has a great framework for visualizing the shocks of a tightening cycle through different sectors of the economy.

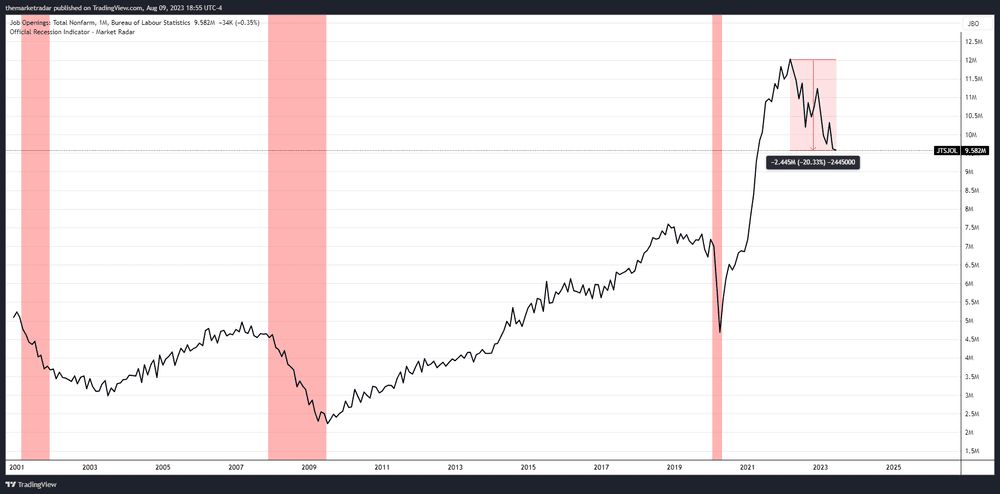

Employment tends to come up as one of the most lagging parts of the economy. Meaning, it's the last to be affected. However, Job Openings are down over 20% from their post-pandemic highs...signaling that something is afoot and things are certainly slowing. Typically, for unemployment to accelerate, you have to clear out excess job openings. This is more evidence that while the unemployment rate hasn't budged, things are shaking up beneath the surface.

Now that you have a basic understanding of policy lags. Let's expand on why they matter, and what is likely going to happen next.

THE PLAY:

It's clear that people are really focused on the unemployment rate as a key factor in causing a recession. The Federal Reserve (the Fed) is puzzled by the fact that unemployment hasn't changed, and they're talking about achieving a "soft landing" that seems unlikely. Let me explain why we think this "soft landing" might not work.

If you look back at the beginning of this message, you'll notice that the Fed has been making some extraordinary changes to its policies during this period of raising interest rates. Basically, they're increasing rates faster and more dramatically than ever before in recent history. The question is, considering this rapid and strong increase in rates, how long will it take for the effects to show up in the economy?

About a year ago, the Fed Funds Rate was around 2.30%, and now it's at 5.25%, a 128% increase. A sensible assumption would be that when rates are tightened so much, it will take a while before the changes affect things like employment. Here's where the problem arises: the Fed's main tool isn't the rates themselves, but how long they keep the rates at a certain level. Because of the unique nature of this rate increase cycle, it's quite reasonable to think that there might be a significant delay before the most important aspects of the economy, like employment, start to feel the impact.

The challenge is that the Fed could continue to have a strong impact on the economy just by keeping rates where they are right now. However, because the Fed isn't really sure about the exact timing of these effects, they will likely end up restricting the economy too much by holding rates too high for too long. This is because even they refer to their policy as having "long and variable" lags, which basically means they're uncertain about how long it takes for their actions to take full effect. Given the Fed holds a lot of weight in data that is the most delayed, it’s probable that they overstay their welcome.

Now, the reason why the idea of a "soft landing" has a good chance of working is that, even though they've been tightening things up quite aggressively, most people are still expecting the usual delays before the impacts are felt. This has created a situation where people are split into two groups. On one side, there are those who believe a recession is imminent because they're not considering the possibility of positive outcomes like higher stock prices. On the other side, there are those who think a smooth economic transition is possible and that we can avoid a recession altogether. They're not worried about economic risks or stock market declines.

Here's where it gets interesting. Because of these extended delays in the effects of the Fed's actions, it's not impossible for a positive market trend to happen before the full effects of the rate increases are felt. This could lead people to lose faith in the idea of a sharp economic decline and make those who believe in a smooth landing more relaxed.

In simpler terms, even though the Fed is being aggressive in raising rates, it might take a while for the effects to kick in. This uncertainty is causing different groups of people to have different expectations about the economy, and this uncertainty could lead to positive market trends continuing before the negative impacts are fully realized. The current Risk-Off environment is extremely boring, it can certainly hold through the storm…or it can shift if the storm isn’t close enough to affect us and we can surf some more waves in the interim before Fed policy completely cycles through the economy.