Soft Landing Rate Cuts - 9.01.2024

OVERVIEW In a financial landscape marked by volatility and shifting probabilities, understanding the nuances of market regimes is more critical than ever. As we approach the quarter mark of the current Risk-Off regime, signs of easing risk probabilities flicke

OVERVIEW

In a financial landscape marked by volatility and shifting probabilities, understanding the nuances of market regimes is more critical than ever. As we approach the quarter mark of the current Risk-Off regime, signs of easing risk probabilities flicker on the horizon—but is this the calm before another storm or the onset of a meaningful shift? In this article, we delve deep into the System's latest readings, dissect the implications of the Federal Reserve's unexpected 50 basis point rate cut, and explore the intricate dance between bonds, equities, and commodities. We'll also spotlight key indicators like labor market trends and commodities prices that could signal whether we're headed for a soft landing or a steeper downturn.

THE SYSTEM

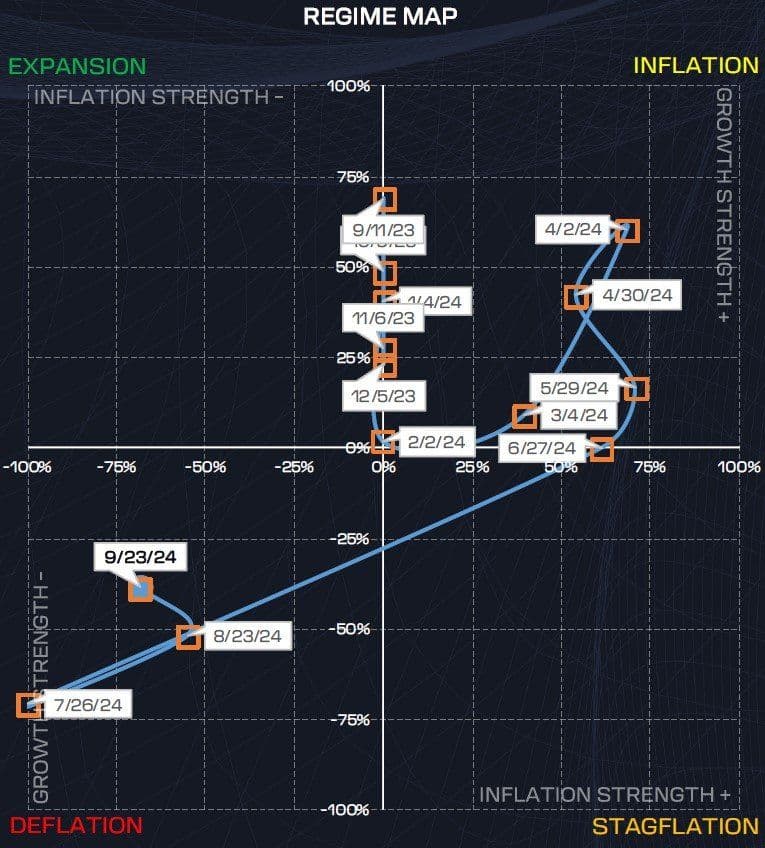

We’re nearing the quarter mark in the current Risk-Off regime, and at Market Radar, we gauge its strength by tracking the growth component in the System. Below is the latest Regime Map, and as you can see, over the past month, there’s been some easing in Risk-Off probabilities. However, it’s important to note that this relief is not yet material. Right now, it appears to be a cyclical chop rather than a decisive shift.

For those unfamiliar, risk probabilities are never static—they're always in flux. What truly matters is where these probabilities settle and how long they stay there. We could be in the midst of a typical countertrend risk move, where Risk-Off probabilities are catching their breath before potentially rebounding to stronger levels. This ebb and flow is reflected in the market’s response—bonds are pulling back slightly, while equities show some signs of life. That said, the chop in equities remains fairly visible, and despite the pullback in bonds, they've still provided solid alpha.

Since our last note, the odds of a regime shift toward Risk-On have improved slightly, but there’s still significant ground to cover. I wouldn’t be surprised if Risk-Off reasserts itself fully. Our models, which rely on System readings, indicate that for now, the System remains firmly entrenched in both the Risk-Off and Deflation regimes.

OUTLOOK

The FOMC meeting is behind us, and the unexpected 50 basis point rate cut has sparked debate. Some see it as a "mistake," others as a "must." We’re in the latter camp, and for good reason, which we’ll dive into below.

In our last note, we pointed out that we’re in a Risk-Off regime, even though equities haven't shown a full-blown bull market, they’d have the potential for gradual gains with bonds being the play. Since then, bonds have delivered solid alpha, outperforming equities, commodities, and bitcoin. Consistent asset signals continue to confirm the System’s Risk-Off stance.

Throughout this cycle, our base case has been a slowdown, with the potential for a recession only becoming clear as signals firm up. Right now, the outlook remains murky—though that’s often the case. Recessions are notoriously hard to spot in real-time; by the time they’re obvious, the market has usually "priced in" the damage. This uncertainty creates what we see as an asymmetrical upside in our positioning. If the slowdown persists, we expect yields to drift lower, especially if the Fed continues to ease more than anticipated. But if the deceleration accelerates beyond expectations, pushing the economy into recession territory, rates could plummet, driving bonds significantly higher.

Right now, markets aren't pricing in a recession—rather, they’re reflecting expectations for moderating growth and inflation. The Systems Deflationary regime outputs support this, with both growth and inflation strength scores both trending negative.

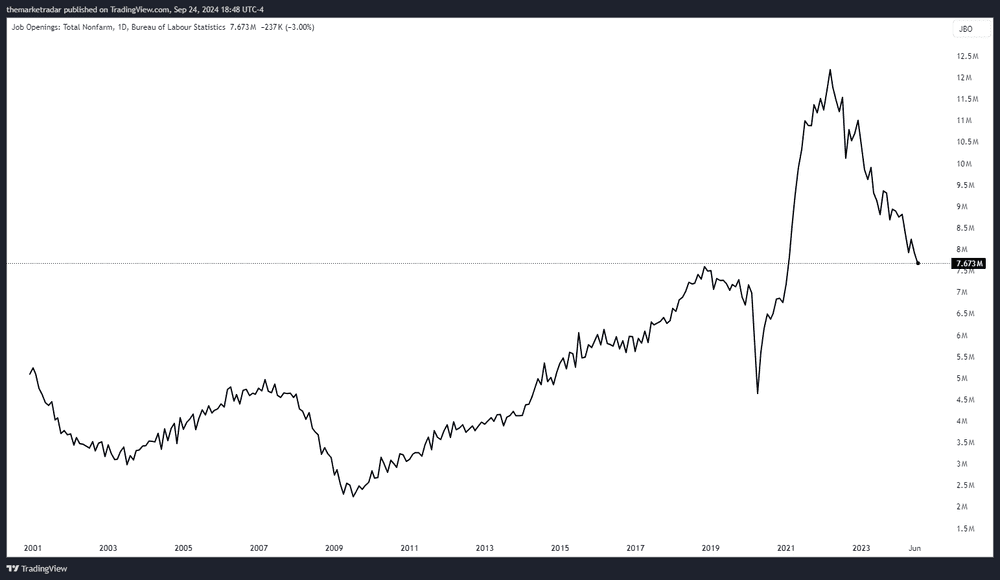

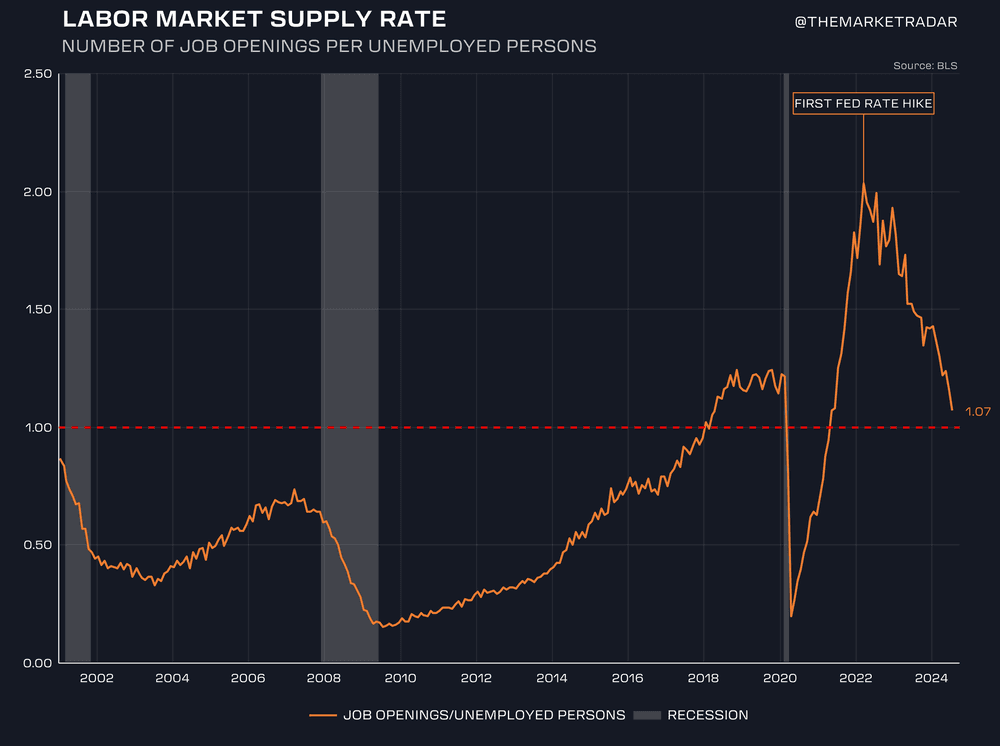

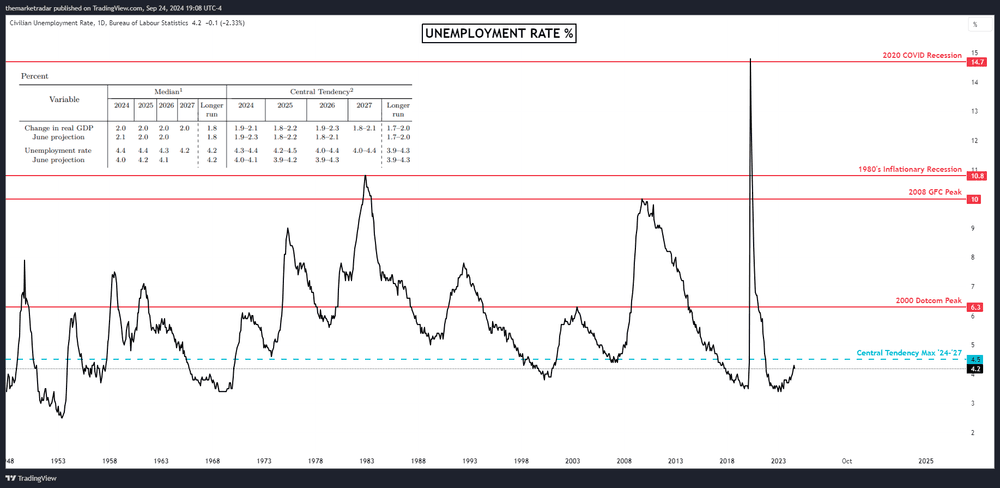

Since the Fed kicked off its rate-hiking cycle in 2022, we’ve seen job openings steadily decline while unemployment has been creeping upward. This dynamic, often framed through the Beveridge Curve, has been a key focus of our analysis and discussions. In our view, the unusually high number of job openings heading into the rate-cutting phase has delayed a sharper rise in unemployment. With so many open positions, companies have generally opted to halt new hiring rather than cut their current workforce.

With job openings returning to levels seen in the year running up into the pandemic and the labor market supply rate, which is the ratio of job openings per unemployed person, back in pre-pandemic territory, it’s clear that the cushion we’ve experienced with a lot of the pressure being taken out on job openings now falls more directly on unemployment.

🚀 Join the Radar Community

Get free access to MacroBase and notifications about new posts and updates.

If current labor trends persist, we expect to see more noticeable pressure on the unemployment rate. Interestingly, the Fed’s central tendency projections cap unemployment at 4.5% through 2027, which is a bold stance considering we’re already at 4.2%. This places the economy right at the upper edge of their forecast, leaving very little margin for error. Even a modest rise in unemployment could put the Fed in a more difficult position than their outlook suggests, forcing them to reconsider their stance and potentially take more aggressive action than they anticipated.

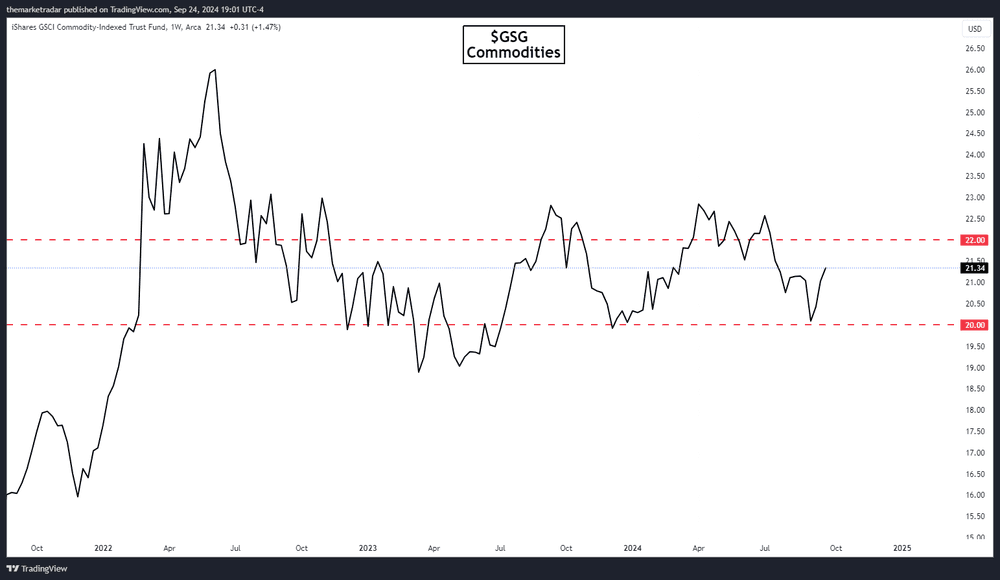

Commodities have also shown some recent weakness, although that has eased in the past few weeks as risk-on/off probabilities fluctuate. Commodities remain a key barometer of both demand and inflation. China’s recent economic stimulus has helped lift commodities off near 52-week lows, but we’re still range-bound. In our view, this range-bound behavior is essential for signaling a soft landing. If commodity prices break higher, it would raise the odds of inflation pressures re-anchoring upward, prompting more hawkish Fed action. On the flip side, if commodities break below their range, it could signal a deeper slowdown, perhaps a recession, and trigger even lower rates than expected. For now, though, the soft landing narrative holds.

The fact that 11 out of 12 FOMC participants voted for a 50bps rate cut to kick off the easing cycle signals a strong consensus: conditions have materially shifted enough in recent months to justify these "adjustment cuts." The majority of the committee seems to acknowledge they were behind the curve. Looking at real interest rates, real growth, unemployment, commodities, inflation, and inflation expectations, it’s clear the Fed remains deeply restrictive. Inflation, notably, has returned to 2018 levels and appears to be on track to hit the 2% target.

In our view, the Fed should have begun this cutting cycle months, if not quarters, ago. The prolonged restrictive stance, coupled with faster-than-expected data easing, made the 50bps cut a logical move. This likely opens the door for further adjustment cuts if current trends persist. However, without a significant weakening in labor—such as unemployment rising beyond the 4.5% threshold—any future cuts are more likely to be seen as soft landing measures. Since labor is typically a lagging economic indicator, its trajectory will be critical moving forward.

It’s important to remember that, by definition, a soft landing is a slowdown that doesn’t result in a recession. While slowdowns and recessions are distinct, both scenarios tend to be bullish for bonds. Bonds marginally outperform during slowdowns, but they significantly outperform in recessionary environments.

Our focus is squarely on jobless claims and unemployment, as labor market conditions now play a pivotal role in shaping the cycle. While equities may still grind higher under the current Risk-Off regime, the System remains firmly positioned, and we expect bonds to continue outperforming in this environment.

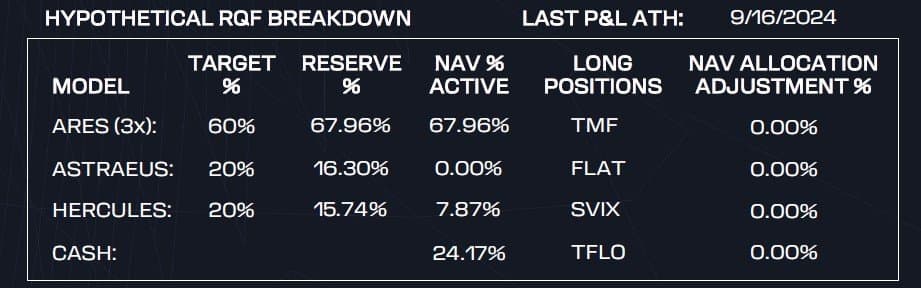

RADAR QUANT FUND (RQF)

Two of the three strategies within RQF are active: Ares, positioned long in U.S. Treasury Bonds, and Hercules, shorting U.S. equity volatility. The RQF is experiencing a normal run-of-the-mill pullback after printing new all-time highs just last week. This is along with us having nearly a quarter of NAV in cash. We expect bonds to continue outperforming equities as this Risk-Off regime progresses, aligning with Ares’ confident positioning. Hercules, on the other hand, is cautiously re-engaging in the short volatility trade. The strategy is more reliant on liquidity conditions, which remain positive but warrant close monitoring. Currently, Hercules is sized partially in response to the positive liquidity conditions but is still waiting for a Risk-On regime for the real size. As always, our moves are driven by the System’s signals, and these strategies will stay in place until the data justifies a change in course.

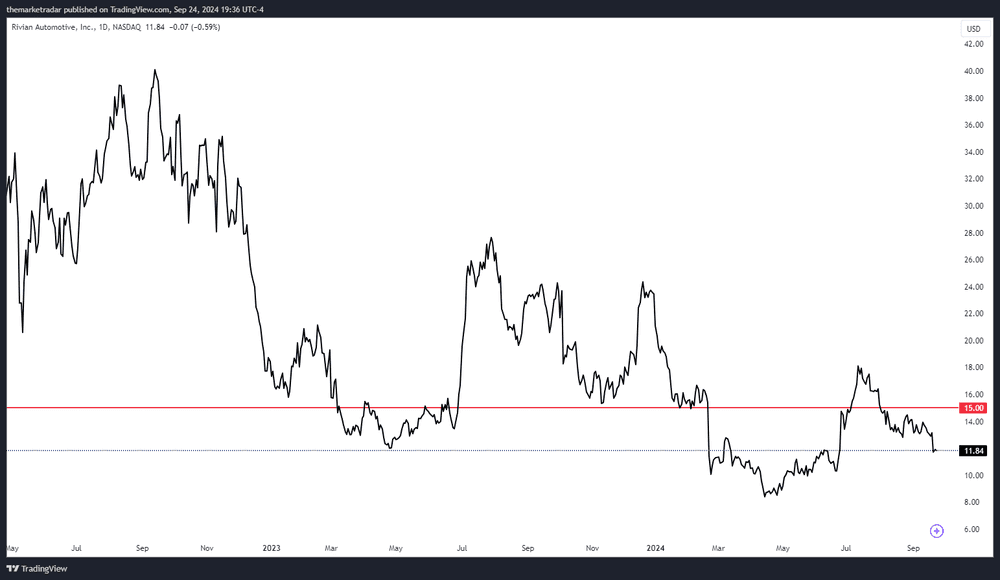

RIVIAN

We began covering Rivian in our podcasts around Q4 of 2023, when the stock was trading around $15 per share. Earlier this year, we formally outlined our investment thesis in a ledger note, which you can find HERE.

Since then, Rivian has been range-bound between $10 and $18 per share. As our long-term outlook on the company remains unchanged. Any further discounts may present an opportunity for us to increase our position size. That said, this remains a small and negligible position compared to our strategy allocations within RQF.