4 MIN READ·JULY 29, 2025

The Great Bull Market

Stocks are booming, the market is at all-time highs, and Bitcoin has broken a multi-month consolidation pattern. Topics like tariffs and the Fed have dominated headlines in the last few months, yet the market has ignored the noise and continues to climb the wa

MR

CONTRIBUTOR · MARKET RADAR

Stocks are booming, the market is at all-time highs, and Bitcoin has broken a multi-month consolidation pattern. Topics like tariffs and the Fed have dominated headlines in the last few months, yet the market has ignored the noise and continues to climb the wall of worry. The predictions made in the last ledger note for the remainder of 2025 are playing out as expected. Consistent all-time highs, falling volatility, it's clear a bull market is upon us, and Risk-On is in play.

Even through all the headline noise, our proprietary system says growth is alive and it’s accelerating. Our systematic trading model, Radar Quant Fund (RQF), is known to go through periods of consolidation and then literally rip your face off as it puts in ridiculous returns in strong bull legs. We’re seeing that now, as it has been positioned max long risk assets since July 10th. We're on the precipice of hitting new all-time portfolio highs, and based on our models, it looks like the serious up-leg is only starting to get underway.

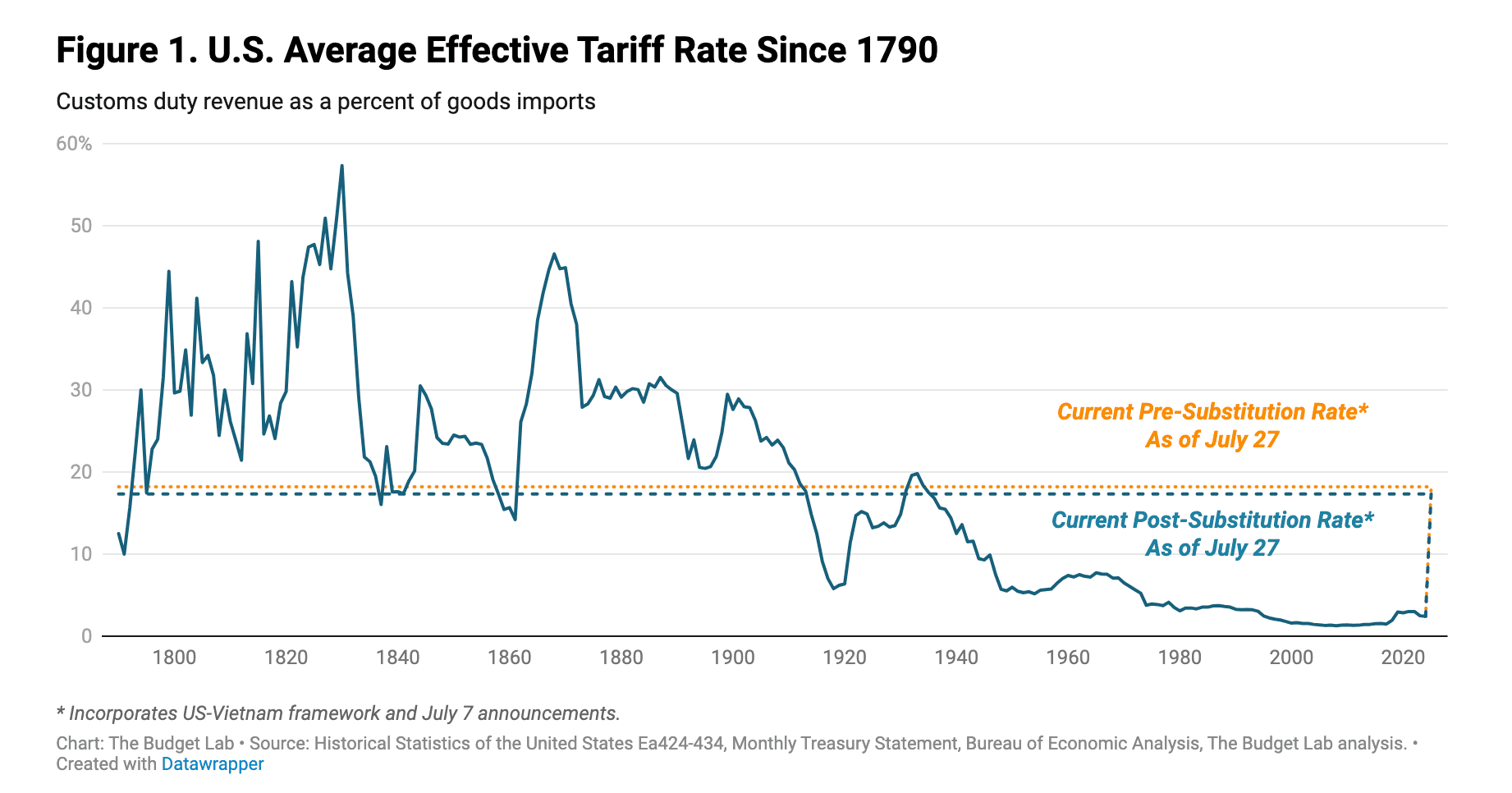

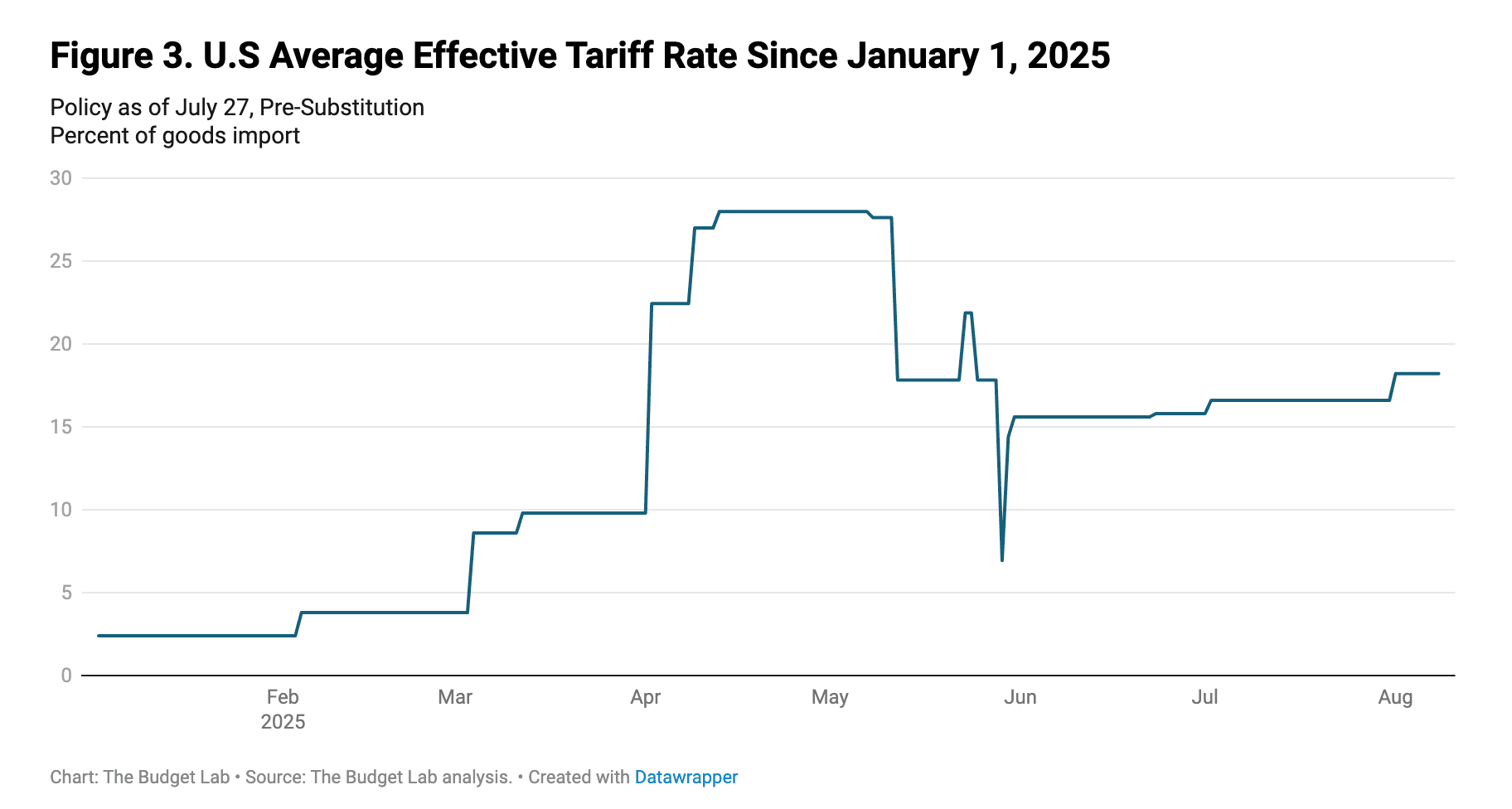

I can tell you that our models are risk hungry right now, but if you pay attention to headlines you may be feeling a large level of “uncertainty’ and confusion. Here’s the deal, tariffs are cooked, you can always find a reason to be bearish, but they certainly shouldn’t be one of them at this point. Despite the noise, the average effective U.S. tariff rate is still hovering near multi-year highs, up nearly 9x from its 2024 closing levels. And while some "breakthrough" trade deals have made headlines, the deadlines keep slipping, and the actual rollback in duties has been minimal. In other words, tariffs haven’t really come down, they’ve just stopped getting worse.

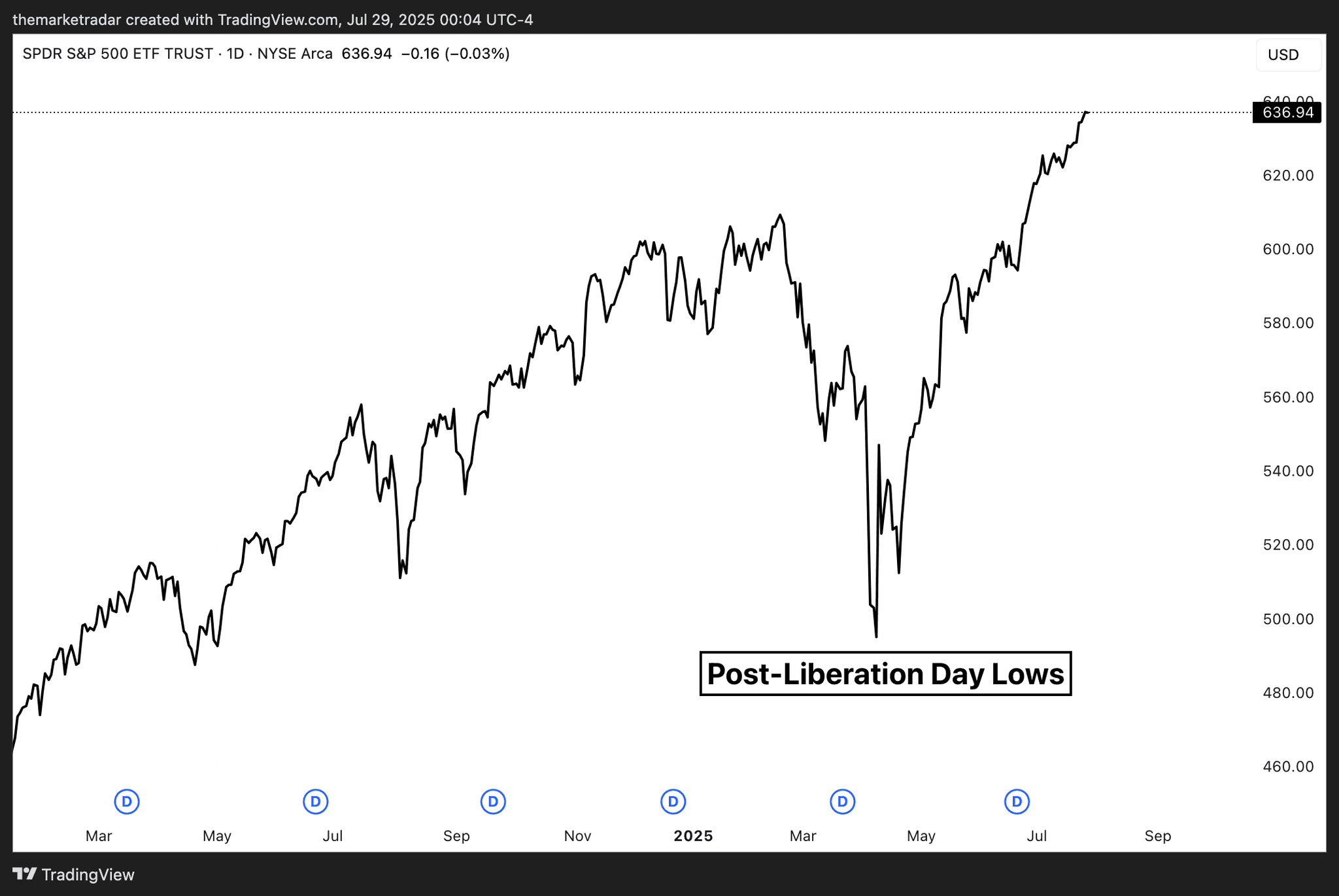

Markets, however, don’t care. The S&P is up over 40% from the lows set after the so-called 'Tariff Liberation Day' panic, which temporarily shook confidence. That rebound tells you everything you need to know: tariffs aren’t in the driver’s seat anymore.

The real force lifting markets? A resurgence in growth expectations, preloaded stimulus, and the forward expectations of fiscal flows, especially those potentially unlocked by the Big Beautiful Bill. Our System sees this pricing mechanism and is going to take advantage of it until it fizzles out.

🚀 Join the Radar Community

Get free access to MacroBase and notifications about new posts and updates.

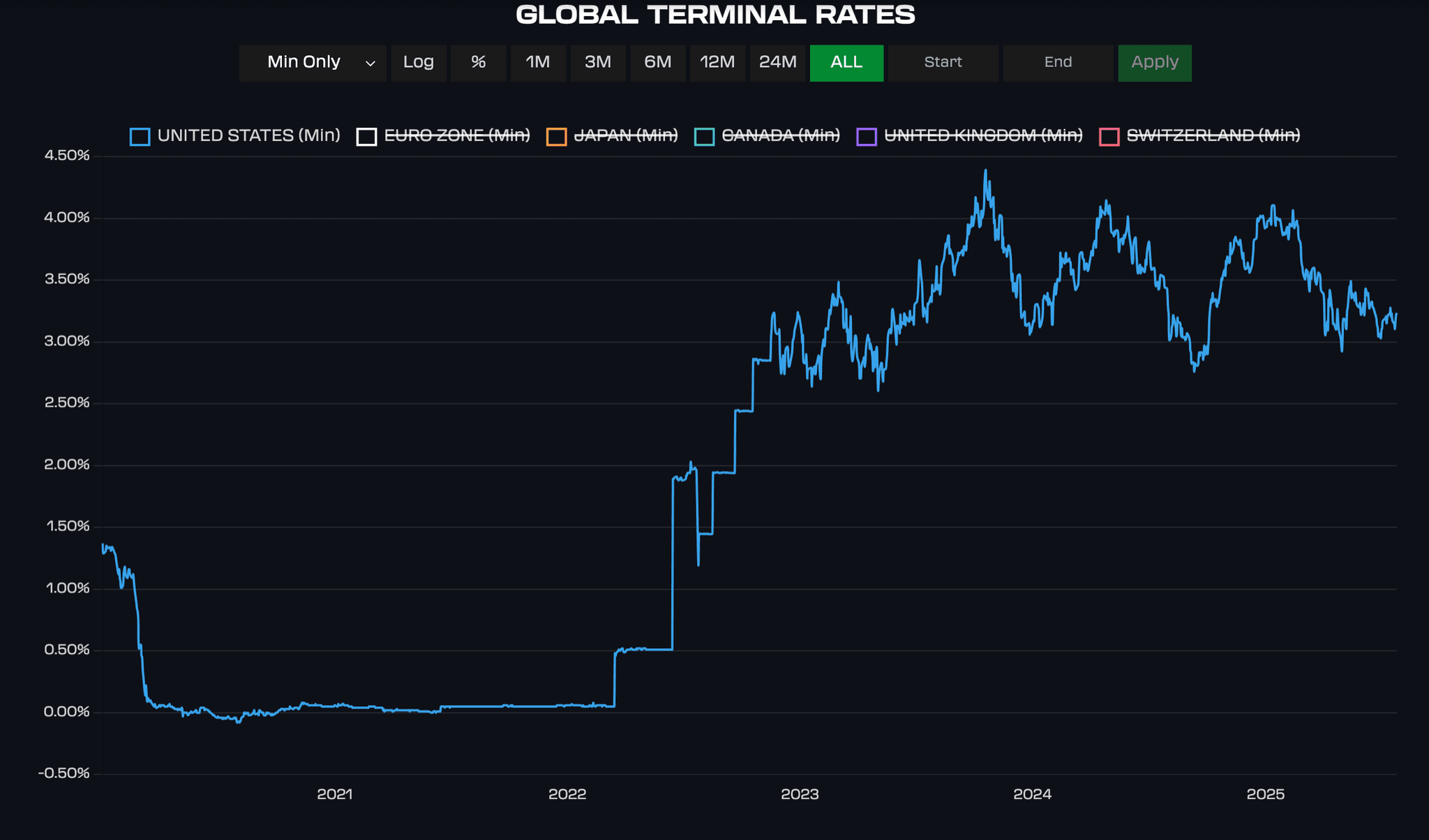

Disregarding tariffs and solid growth expectations, FOMC still has some runway here where rates can be reduced gradually. However, we’re not going to see anywhere near what the Trump administration is calling for. The level of policy reduction the White House is calling for is what you would see in a crisis. We’re currently in no crisis, and the Fed is still trying to understand the transitory flows of tariff impacts on inflation.

Market-based inflation swaps are showing us that there is “some” concern of there being a rise in inflation expectations; however, this move is still insignificant and can be chalked up to price action and transitory offsets. These are figures that are not bad enough where they concern some Fed members, and others may simply disregard them. But, they do raise some concerns as to their level given the Fed still holds policy over 4% signaling that they have limited room in forward guidance before their policy feeds back into inflation expectations.

The Fed has kept markets steady on their forward guidance with their lowest project policy point, terminal rate, over the next 3 years is still higher than the 2024 lows. The reason for this can be attributed to large fiscal deficits and the need to maintain a higher neutral rate to offset deficit effects and keep inflation contained.

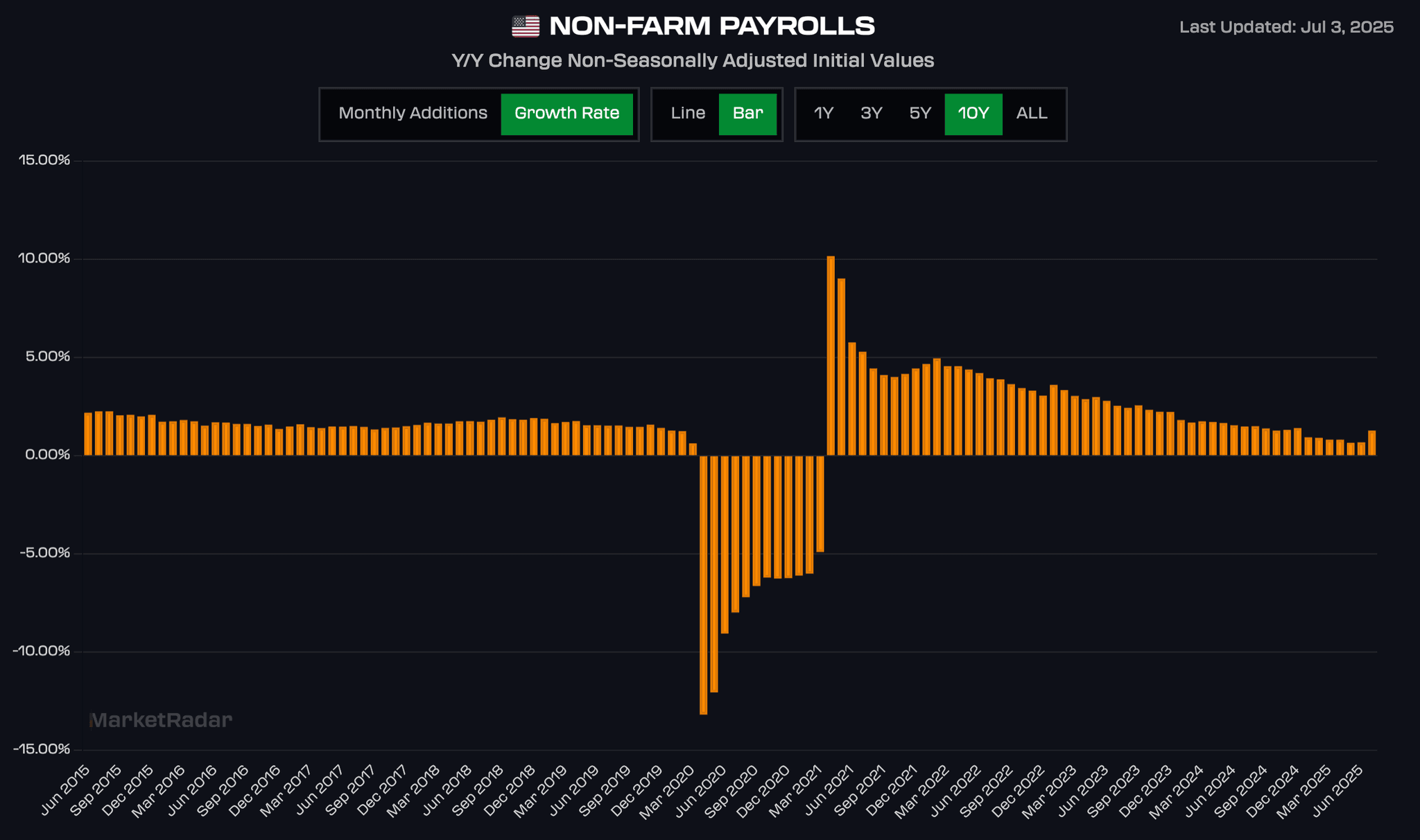

The headwinds in payroll growth rates do raise some concerns that the Fed could legitimately act on their forward guidance of gradual policy reduction over the next year. However, we’re still holding a decent growth rate for now, if this is around the 1% figure, we likely aren’t facing a recession or any real labor market stress.

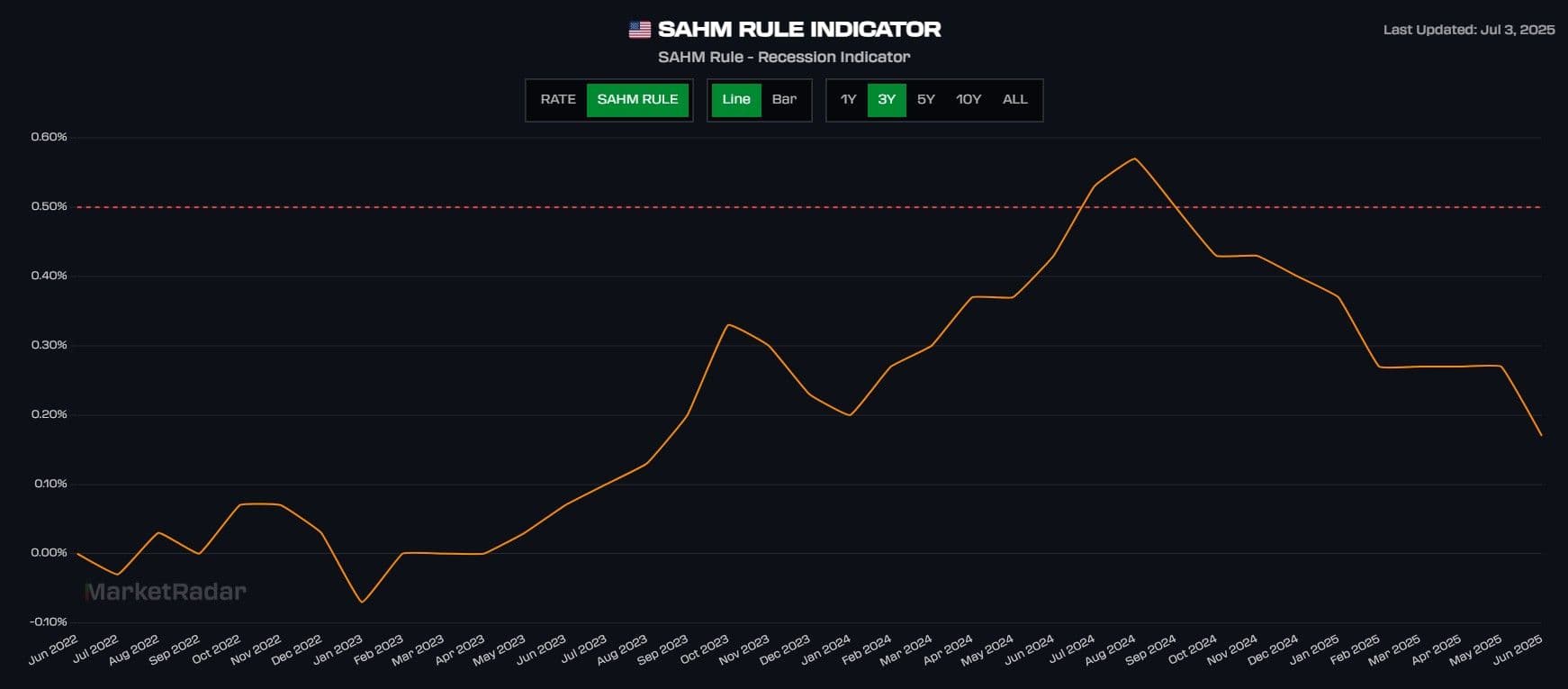

The unemployment rate has also shown a significant reduction in momentum from around this time last year. The Sahm rule, which measures momentum in the labor market, has crumbled over the last 12 months, after briefly triggering a false signal last summer. This is yet another sign that labor market conditions are going the opposite direction they should be if you're hoping for super doves at the FOMC. The Fed is in a position here where they can ease into the forward guidance which is already priced into the market, but they don't have much room further unless disinflation forces start rapidly coming back to life.

Navigating an environment like this, with constantly contradicting headlines and breaking news daily is especially hard for discretionary traders trying to quantify the headlines themselves on a daily basis. Our systematic approach allows us to think less, bet more, and try and ride as much of the cyclical wave as possible. With the market just experiencing the tariff panic lows a little over 3 months ago, a majority of individuals may have been simply caught off guard on risk given the sheer whipsaw in price action. Without a recession coming to fruition, which our System would almost certainly see coming, lots of hands are going to continue to be forced back onto the table as the tariff fears slowly get priced out and fiscal stimulus in an economy that probably doesn't need this level of stimulus regains control of the driver's seat. Dips are to be expected; they're buyable on our watch until further notice.

MOST POPULAR

Unlock Premium Content

The remainder of this content is available to Radar members only. Subscribe to gain instant access.

$65/month

Billed annually at $780 (Save $120)

Access Models which boast 40%+ average yearly returns

Automated Portfolio Signals (RQF Strategy)

Live Calls with experienced traders

QuantBase Dashboard with macro regime models

DDAP TradingView Indicator

Real-time portfolio updates

Private Discord Channels

Lifetime Price Lock|Instant Access