The Labor Market Fake-out

The August Jobs Report May Be the Fed’s Biggest Test Yet Markets just got the weakest Nonfarm Payrolls (NFP) print of the year: only 22,000 jobs added versus expectations of 75,000. Yet the unemployment rate held steady at 4.3% as per forecasted. At first glan

The August Jobs Report May Be the Fed’s Biggest Test Yet

Markets just got the weakest Nonfarm Payrolls (NFP) print of the year: only 22,000 jobs added versus expectations of 75,000. Yet the unemployment rate held steady at 4.3% as per forecasted. At first glance, this looks like a simple slowdown in hiring. But the market’s reaction tells a far more complicated story, one that could define how policy, inflation, and asset prices evolve in the coming months.

Why Risk Assets Rallied on Bad Jobs Data

Normally, disappointing labor data sparks concern about growth. But this time, equities and credit moved higher: the Russell 2000 (IWM) rose 44bps, the Nasdaq 100 (QQQ) gained 14bps, and high-yield bonds (JNK) ticked up 9bps. This mirrors nothing like the August 2024 reaction, when the Sahm rule triggered and risk assets fell on real recession fears. Instead, today’s rally signals that markets expect the Fed to ease at the first signs of weakness, even if doing so risks stoking inflation.

The Inflation Risk Lurking Beneath the Surface

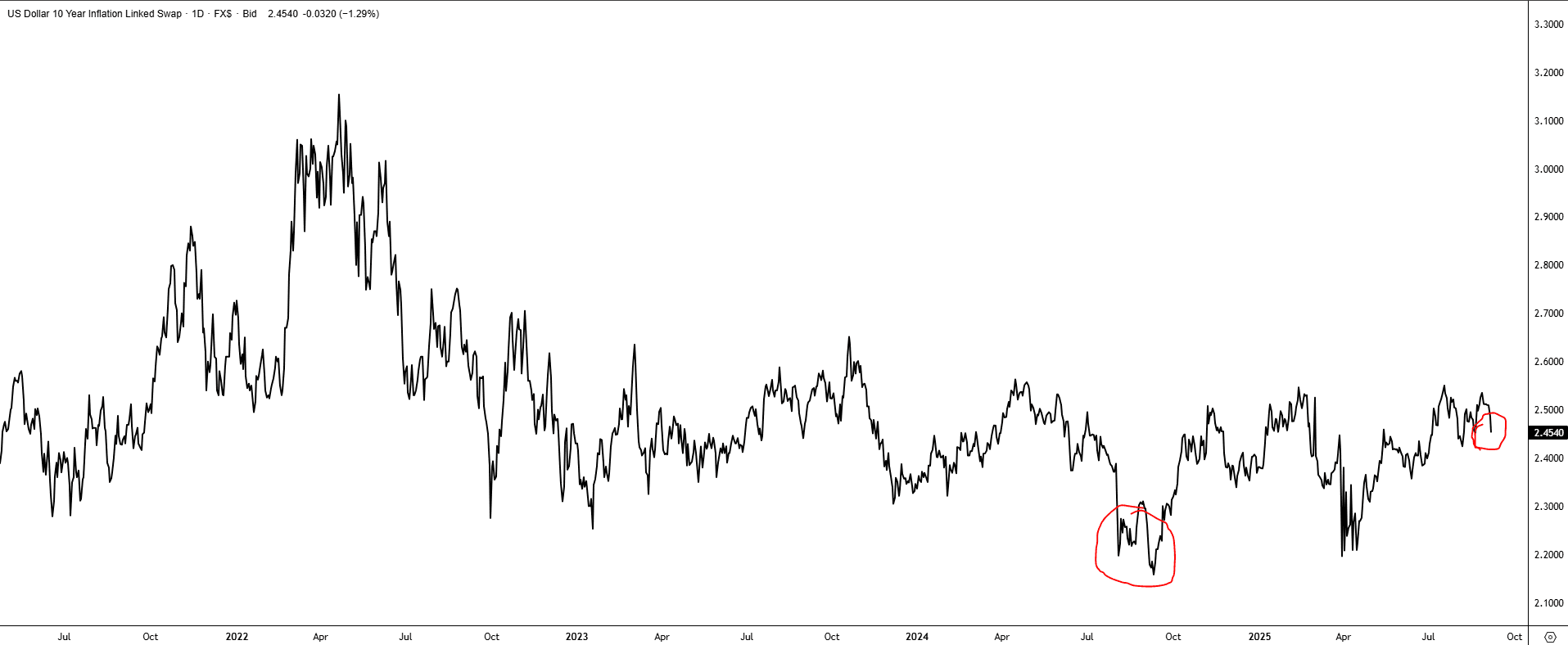

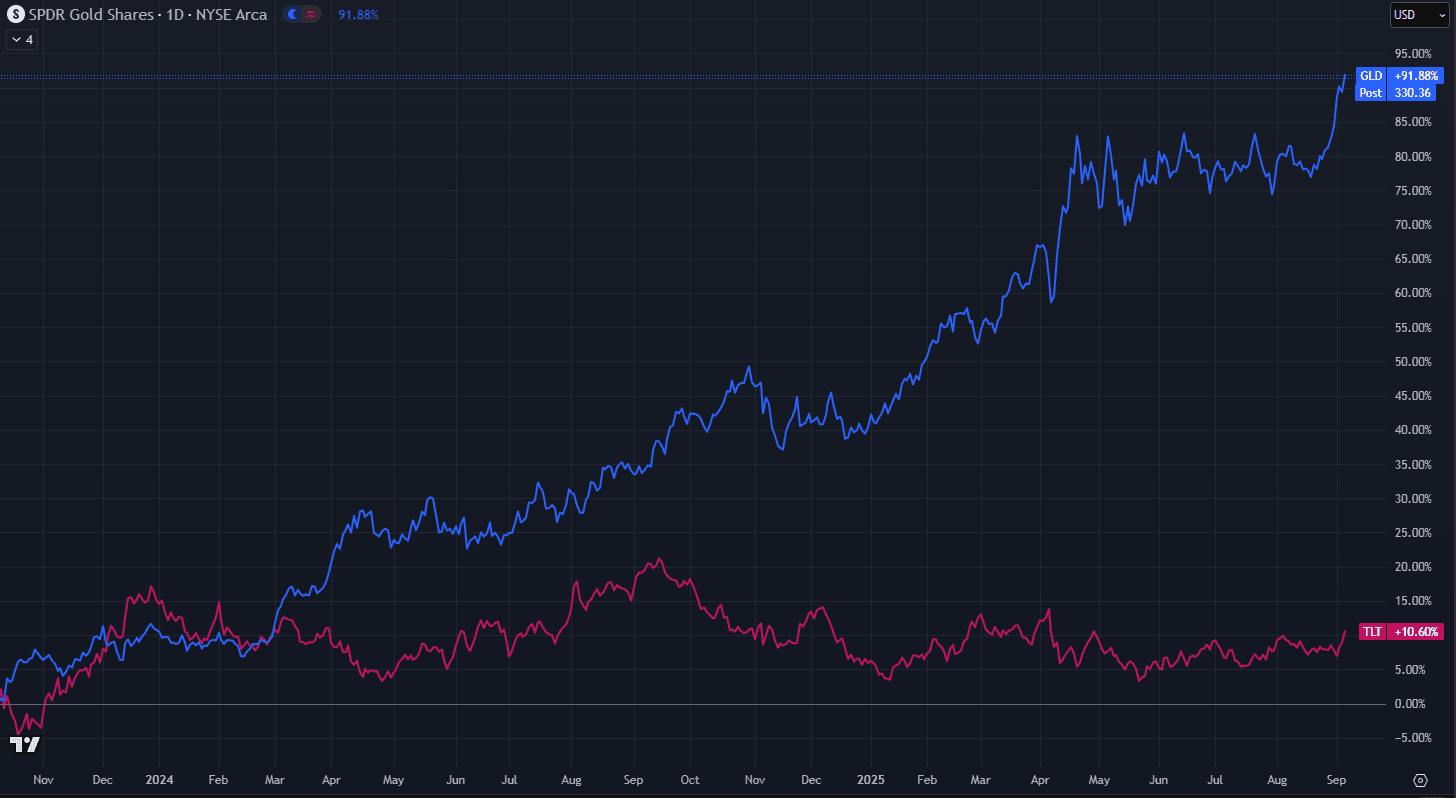

The Fed has already shown its willingness to protect the labor market at all cost including at the expense of inflation control. With inflation expectations higher today than in September 2024, as reflected in the 10-year Treasury yield, rate cuts now would not stabilize growth but rather accelerate it. Combined with ongoing fiscal support, the likely outcome is stronger demand, higher asset prices, and renewed pressure on inflation. Gold, equities, and credit markets stand to benefit in the near term, even if long-term inflation risks build.

🚀 Join the Radar Community

Get free access to MacroBase and notifications about new posts and updates.

Typically negative labor market shocks are deflationary in nature. Given the fact that long term inflation expectations are not at or below the levels we saw last summer when unemployment started accelerating gives the indication that the market likely isn't too concerned about a recession and inflationary impulses are still alive and well, signaling a lack of true underlying deflationary labor market weakness. The rise of central bank dovishness into this dynamic of persistent inflation and short term labor shocks is what we see reflected in golds significant disconnect from treasuries over the last few years.

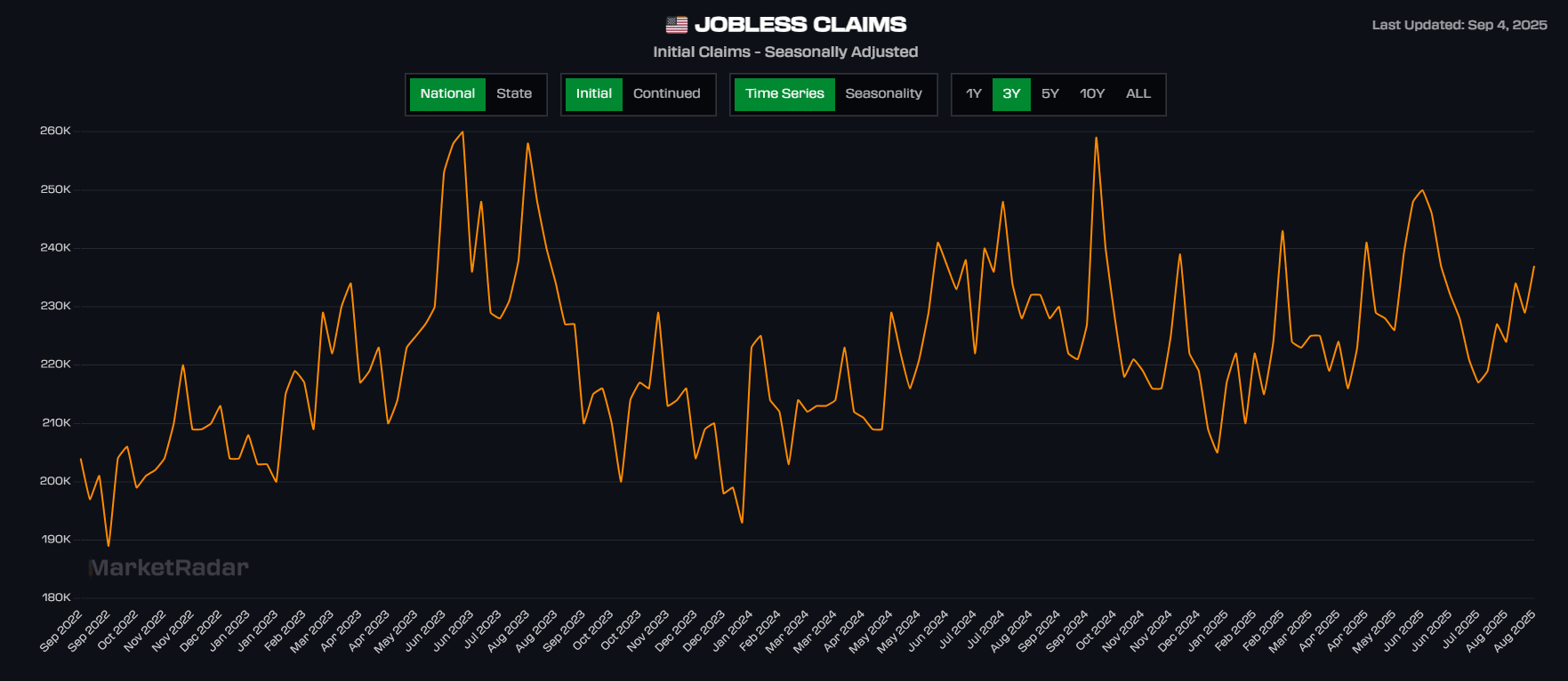

Jobless Claims Add Critical Context

The broader labor data complicates the picture. Jobless claims have remained in a narrow range since 2022, showing no material rise in layoffs. Payroll growth has slowed, yes, but this hasn’t translated into rising unemployment or an elevated firing rate. The signal is clear: the labor market is cooling, not collapsing. That makes this NFP print less about an economy on the brink and more about how the Fed responds. If policymakers cut too quickly, they could supercharge growth and inflation rather than smooth the cycle. A deeper analysis on the labor market dynamic shifts is outlined in The Labor Surprise Nobody is Talking About.