The Next Leg - 07.17.23

With so many variables at large, let’s simplify the Market Radar message and lay out what we’re seeing as of right now. Soft Landing Let’s start with the current situation with the “Soft Landing”. Given where we are with inflation and employment, the soft land

With so many variables at large, let’s simplify the Market Radar message and lay out what we’re seeing as of right now.

Soft Landing

Let’s start with the current situation with the “Soft Landing”. Given where we are with inflation and employment, the soft landing narrative is firmly gaining confidence. We went over the Fed’s approach towards a soft landing HERE. I want to cover it a bit differently today, as it seems the consensus is rapidly catching on. For those that don’t know or are new, we’ve been harping about the nature of the soft landing since Q1 of 2023. We even coined our own saying that goes like this: “The soft landing will continue until all faith in the hard landing is lost”. Along with that, we’ve emphasized that the soft landing is impossible…but like everything in finance, you can get creative with the word “impossible”.

We have discussed the likelihood of the Fed overtightening due to the rapid deviation between lagging and real-time data. To sum up the potential "hard landing" (which doesn't necessarily need to result in a deep recession), it is highly unlikely that the Fed will be able to merely slow down the economy and magically offset a recession while also preventing inflation. However, as is often the case in the markets, some people believe that the Fed can precisely navigate this situation without considering the lags in Fed policy, and some even deny the existence of these lags.

I assume many of you reading this might be thinking, "Okay, great, gamma is warning us about an impending hard landing, and I agree." However, I want to stop you right there. Just because we may see a hard landing doesn't mean that it will happen immediately or be as severe as the Global Financial Crisis (GFC). In our podcasts, we have discussed that unless the market can outprice the expected "recession" in 2022, it will be challenging to significantly impact equities.

Regarding point #1 mentioned earlier, the soft landing could continue until everyone is fully committed to it. It seems that we haven't reached that point just yet. A good indication of a soft landing would be cuts up the FFF curve and a more relaxed stance from the Fed in their statements. The best indicator will be when the Fed claims they have achieved it, specifically Powell. However, currently, that's not the case, and thus, I believe the market hasn't fully priced in the certainty of a soft landing. This situation presents an opportunity for us, provided the System deems it appropriate. Now, let's move on to the next segment and discuss the role of the System in the soft landing.

The System

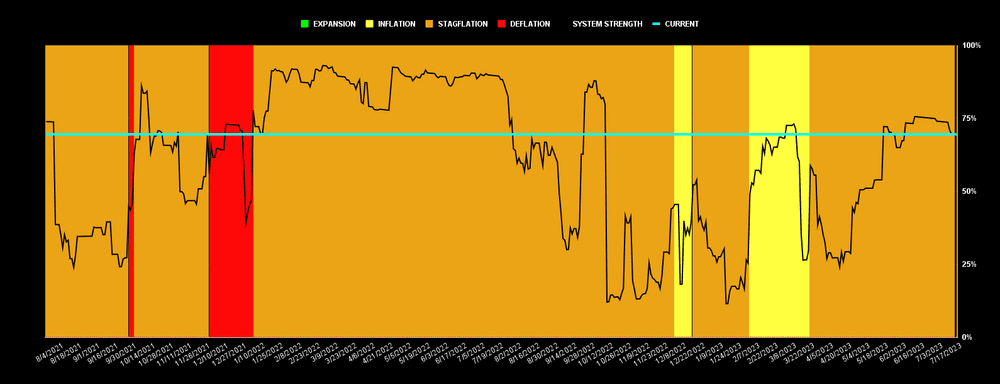

For the past 4 months, the System has been pretty boring, I know. It's worse than watching paint dry. I'm sure most of our new followers and listeners perceive the System as a senior citizen who doesn't know if they're coming or going while cruising at 40 mph on the highway—a highly annoying and dull experience. My simplest response to you is this: you're at the right place, but it's just not the right time. The System doesn't settle for 40 mph on the highway; it goes 120+ and makes sure to take pit stops to change tires and refuel/oil so it doesn't jeopardize your journey. Right now, we're in the pit, refreshing.

This period of "rest" has led many to believe that the System is gearing up to flip to Risk-Off and invest in TMF. To some degree, that's what I hope happens, and I would agree with you in thinking that Risk-Off "feels" more appropriate, especially after NQ performed exceptionally well during the first half of 2023. However, I'll tell you this: this is a game of playing high-probability scenarios. Unfortunately, the System didn't consider the long opportunity presented in early '23 as durable enough to hold onto. Does that upset me? Yes, I want to move aggressively, not sit in money market funds. The System has remained rather consistent in strength, as we observed it pick up during the current Risk-Off regime over the last 2 months.

This means exactly what it says. The System doesn't currently see an adequate level of risk-to-reward in either bonds/gold or equities. This is where things can get interesting, particularly in terms of what comes next. As I mentioned earlier, we're all more or less "assuming" that a full Risk-Off pivot is next. However, we need to be cautious about selling ourselves a narrative. The stock market is known for unexpected turns becoming reality quite often.

🚀 Join the Radar Community

Get free access to MacroBase and notifications about new posts and updates.

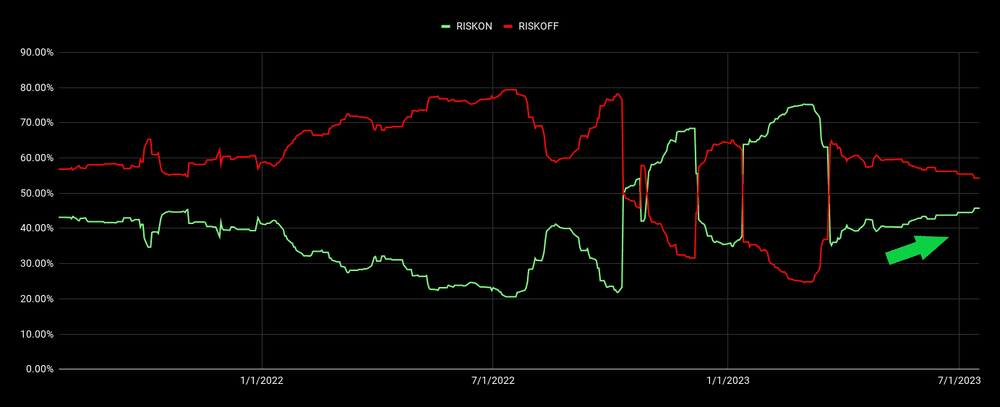

As you can observe, Risk-On has been slowly building in the past few months, despite Risk-Off dominating the scene. It's essential to pay attention to this, especially noting that the odds aren't that far off—we're basically at a coin-flip between Risk-Off and Risk-On!

The last thing I want to see is Ares ripping a long position in the Q's after such a significant year-to-date (YTD) increase. This is where Market Radar comes full circle. I've reiterated this point many times: base your narratives on the data, not the other way around. Many people can only envision one direction for equities: lower. However, as I explained earlier in the Soft Landing section, there's a possibility that the party can continue for some time.

Therefore, I must set aside my own "feelings" about what I think will happen and focus on Ares' perspective and predictions. Is it possible that we could actually go Risk-On? Only time will tell, but I refuse to become a lost soul fixated on pessimistic views perpetually. That is a job left for the Simps.

The Fed

After reviewing the previous points, it might appear as a good idea for the Fed to hike rates even more aggressively until something breaks. Some of you may have that mindset because you strongly believe in the possibility of a hard landing and wouldn't mind witnessing whatever measures it takes to achieve it, even if it leads to a deep recession, and so on. However, that's not a realistic approach. We must follow the data.

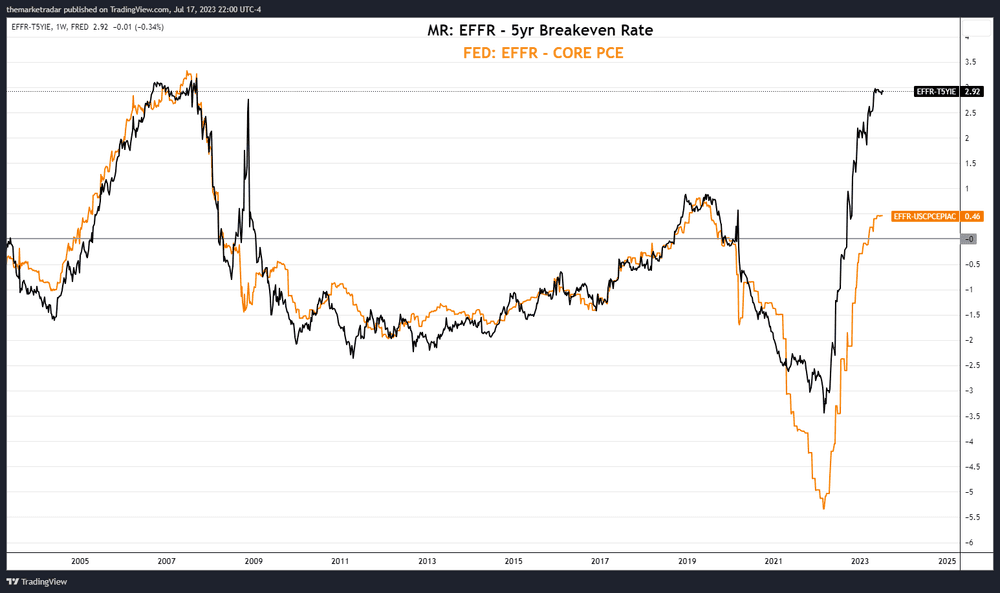

Regarding the Fed's fight against inflation, they have done a spectacular job, especially after letting it escalate between '21 and '22. As we explained earlier, the Fed is likely to overtighten either through nominal rates or relative rates, holding policy in a restrictive state for too long. You can find a better measure of "real Fed policy" than what the Fed provides HERE.

As you can see below, the Fed is currently in restrictive territory. This becomes highly significant when comparing it to their lagging indicator of "EFFR-CORE PCE," displayed in orange. This discrepancy makes it very challenging for the Fed to navigate the situation effectively. Typically, the Fed's measure follows the Market Radar measure, only recently showing a disconnection. The rapid fluctuations in inflation and disinflation will undoubtedly have consequences, particularly on lagging datasets.

So where do we go from here? I don't believe the Fed should, or even needs to, hike rates anymore, and the current policies can be maintained in a state of restrictiveness. In the past few weeks, I've made comments suggesting that it's more likely than what the market has priced in, that we have already seen the last rate hike, and that the Fed is just pausing from here. The odds, which have hovered around 90% for a rate hike over the past few weeks, despite employment and inflation data, make me think that the likelihood of a hike is becoming more of a reality than a mere head fake. While I have accurately predicted nearly every Fed move over the past 18 months, we all have to take L’s sometimes and if this is it for me, I’m ok with it.

Unfortunately, it's challenging to predict whether the Fed will ignore the data to make a statement for credibility. Regardless, the additional 1-2 hikes they have been signaling shouldn't cause significant damage, as the major impact of the rate moves has already taken place. Now, it's more a question of the duration of these rates rather than their specific level. This is where things get tricky for the soft landing because as the Fed plays catch-up with their lagging indicators, they will likely fail to implement the proper approach to softly land the economy.

As we discussed earlier, this doesn't mean the hard landing is imminent right now. We are in a unique situation where the data can lag for longer than expected, creating an environment that is unpredictable and even resented, defying everyone's expectations. Being prepared for the unexpected and approaching each day with a level head is essential. Don't focus too much on what happened yesterday or last month, but pay attention to what is happening right now.

Let's just say the hard landing has been postponed. At this point in time, considering the current state of the market, how many people do you think would absolutely REFUSE to go long here? Think about it; Ares might pull a rabbit out of a hat and even make me go against my own "feelings."