7 MIN READ·AUGUST 15, 2025

Time for Rate Cuts?

It seems like the Fed has been in focus lately, specifically the current administration’s adamant calls for significantly lower rates. The market is expecting rate cuts, just nowhere near what the President is calling for. The administration is calling for any

MR

CONTRIBUTOR · MARKET RADAR

It seems like the Fed has been in focus lately, specifically the current administration’s adamant calls for significantly lower rates. The market is expecting rate cuts, just nowhere near what the President is calling for. The administration is calling for anywhere between 2-and-3 percentage points of policy reduction from the Fed, which comes out to 8-12 rate cuts. They want this immediately, too. The market, on the other hand, is much more restrictive; it forecasts that at most we’ll see 6 rate cuts over the next THREE years.

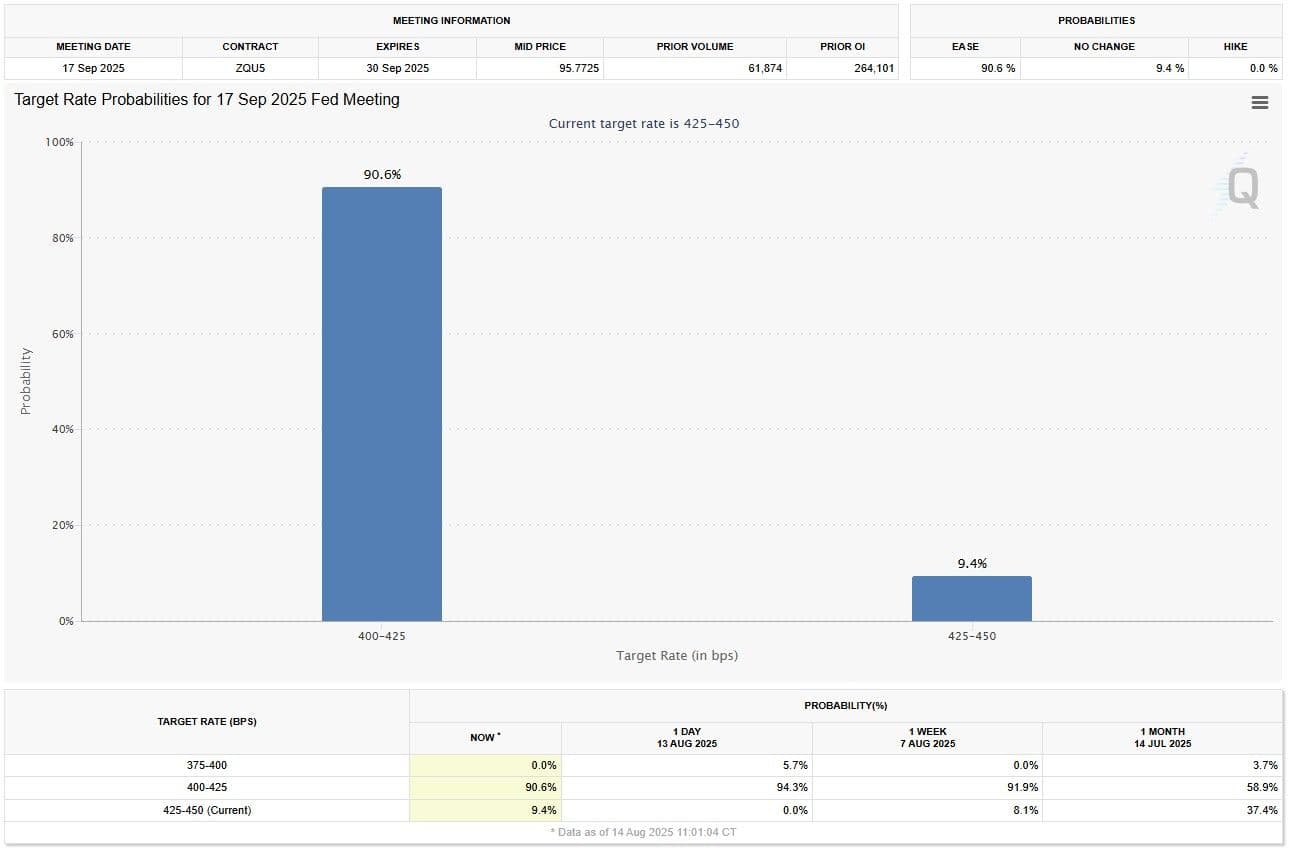

In theory, the Fed is independent. Their policy decisions should come with little-to-no political influence, and they should solely react to incoming data, not the opinions of our political leaders. Despite the administration’s calls for 8 rate cuts immediately, we’re seeing the market price that the Fed will cut rates at the September (next) meeting by 25 basis points, or 1 cut, with a 90% probability.

Before we cover exactly what is driving these rate cuts, we need to understand that the Fed, by nature, has a dual policy mandate. They aim to achieve maximum employment with price stability. In other words, they aim to keep the labor market growing with low inflation. In recent FOMC press conferences, Powell has made it clear that the Fed’s mandate has shifted into a better balance. Over the past few years, we have had a very strong labor market, with high inflation, so wrangling inflation took priority. Now Powell is saying that the two are more balanced and there are more risks to a weakening labor market that could get the Fed to react, as the inflation rate has fallen quite a bit over the past 2 years.

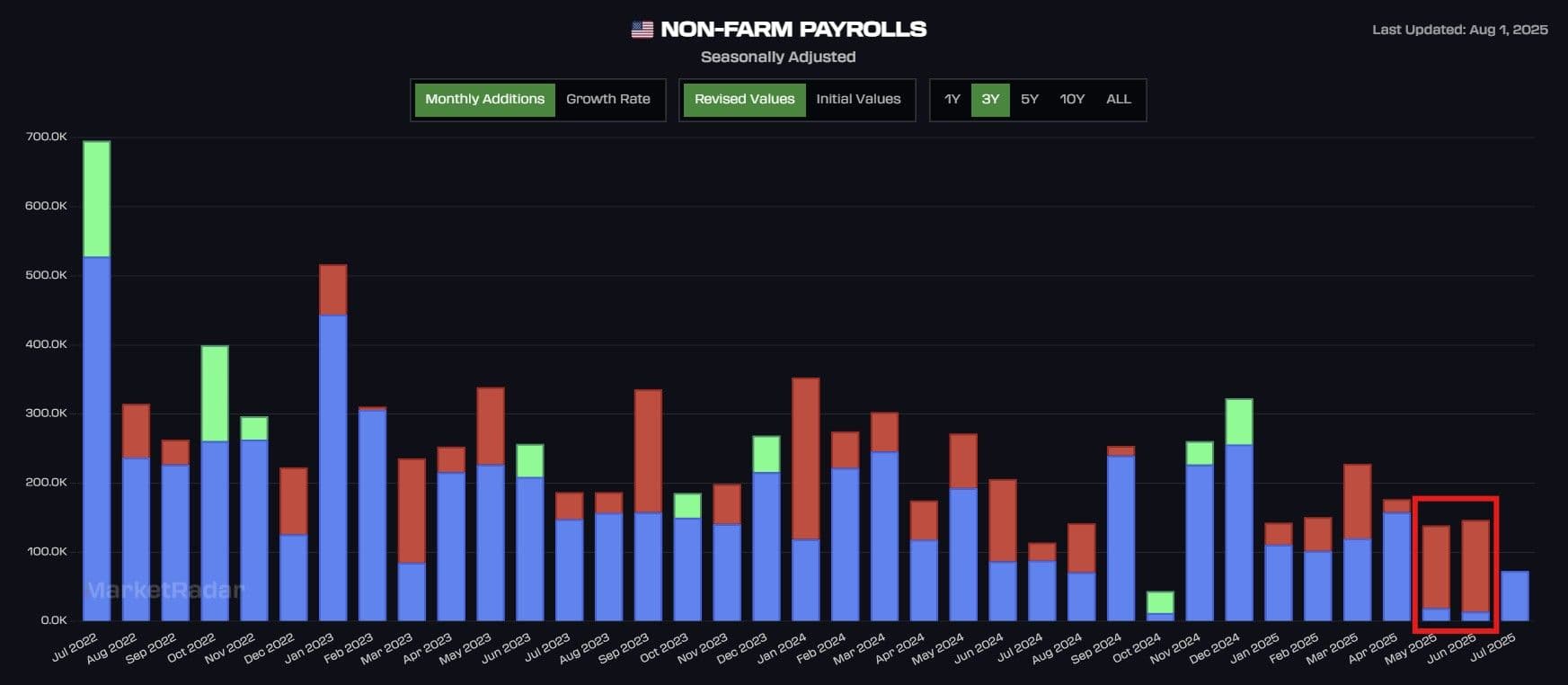

This rebalancing in their mandate is exactly what is fueling the shift in rate cut probabilities. In the past 15 days, we went from a sub 40% probability of a September rate cut to a near 100% probability. The cause? The weak Non-Farm Payroll (NFP) report we received at the beginning of the month. Remember, the Fed is more equally weighing the performance of the labor market and inflation now. The big breaker on the NFP report was the huge negative revisions that came with it for the prior 2 months (May and June). Both figures were revised 90% from their original reported values and were barely positive. Typically, when negative revisions accelerate like this, we’re used to seeing a recession as labor deterioration is a pivotal point in the economic cycle.

Initially, the market dumped on this news; it closed sharply that day, but has since reversed all those losses. There’s a signal there that I think requires some attention. While both the market dropped and September odds climbed from 40% to near 100% probability, the market has since rebounded, BUT the odds have not fallen out of the 90% range for a cut.

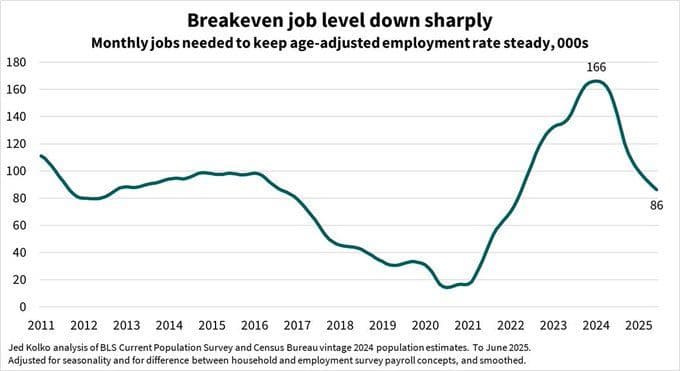

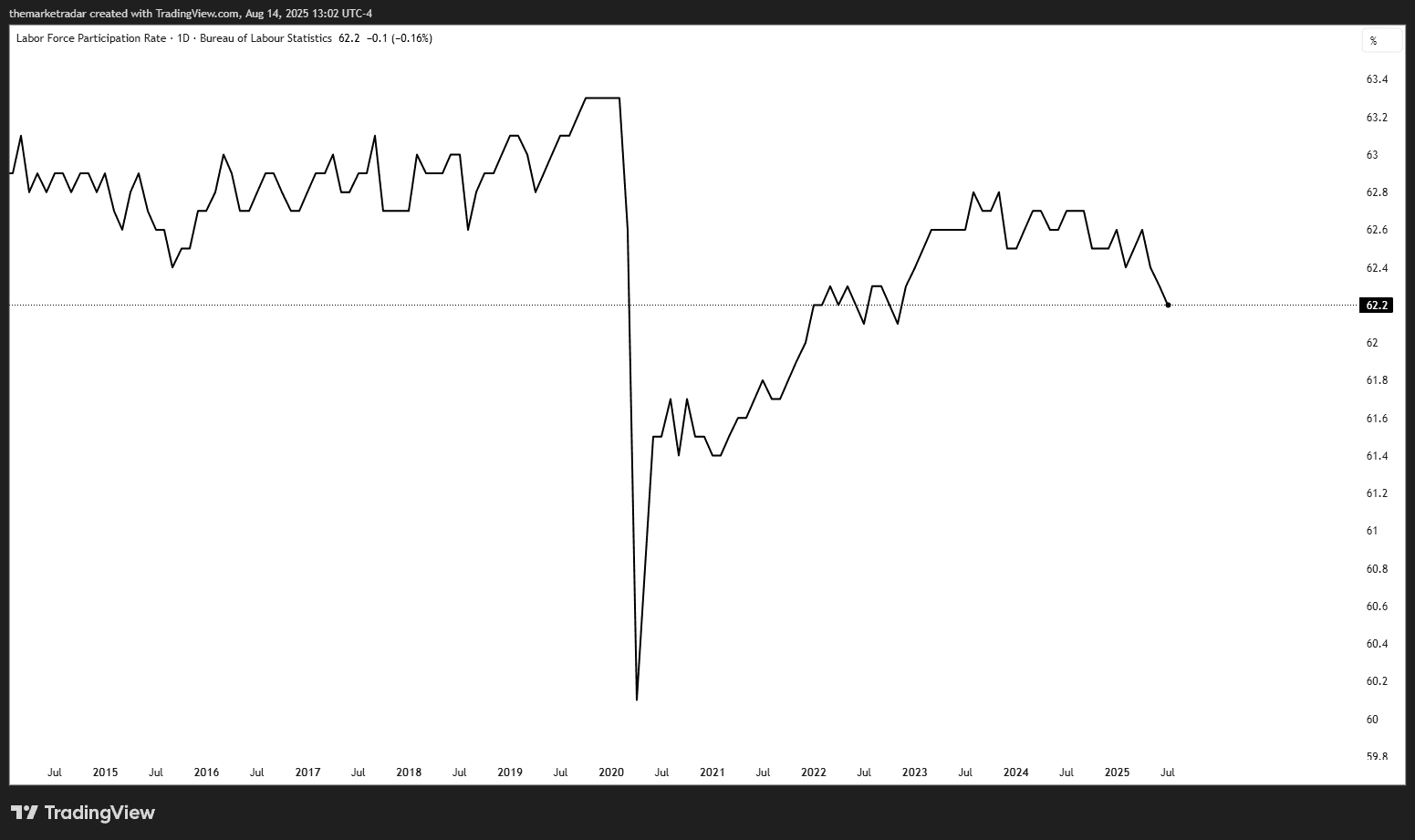

We believe the signal to be the fact the lower NFP prints are a side effect of immigration policy, rather than a truly weakening economy. There’s a lot of commentary around this, but the effect immigration is having on the economy is a reduction of supply in the workforce, therefore leading to a lower level of competition and ultimately, a lower number of required “new jobs” to keep the labor market growing. This can be explained visually through the estimated “breakeven job level” below:

What backs up this theory is the coinciding decline in the labor force participation rate. This also feeds back into the unemployment rate, where it essentially is weighed down as supply constricts and there is fewer people looking for jobs in the workforce, leading to a seemingly unchanged unemployment rate.

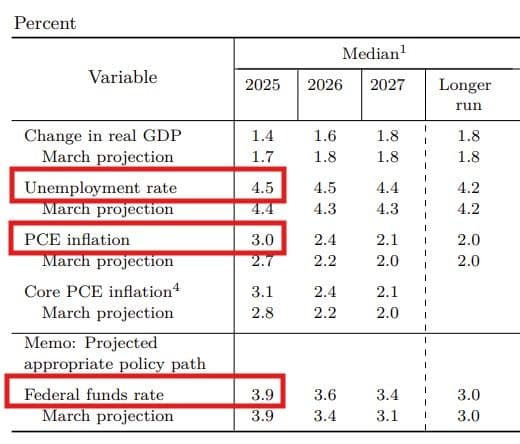

Now that we have covered the basics, we can go back to the Fed and how the changes across these data points feed back into their decision-making. Every quarter, the Fed releases what is called a Summary of Economic Projections (SEP), and it encompasses multiple data points across the economy. The most important being datapoints around their mandate, PCE (inflation), and the Unemployment Rate (labor). Based on the following median forecasts for the rest of 2025, the Fed is seeing a median Fed Funds rate of 3.9% in 2025; we're currently at 4.3%, leaving roughly 2 rate cuts for the rest of the year. Does the data seem to have shifted enough since the last SEP to warrant the Fed cutting rates out of caution? Let's explore.

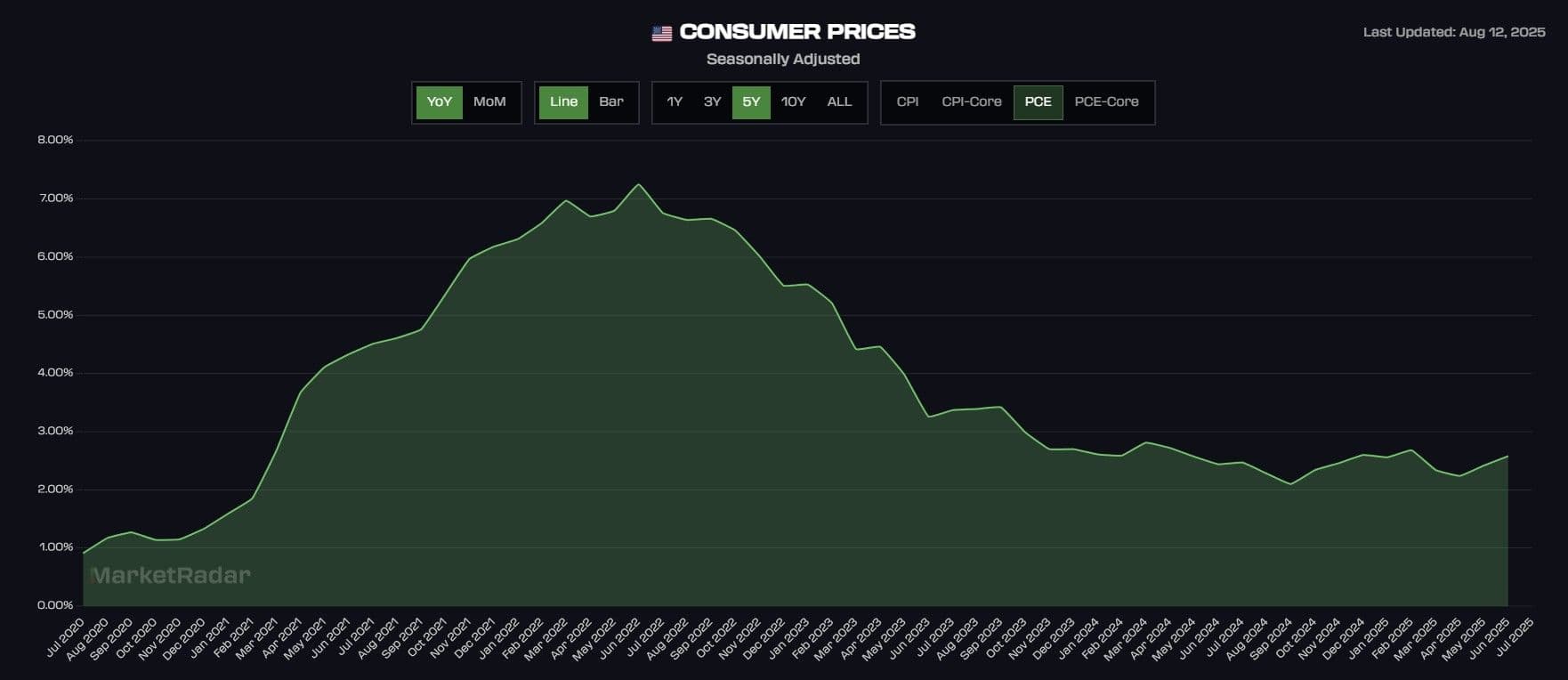

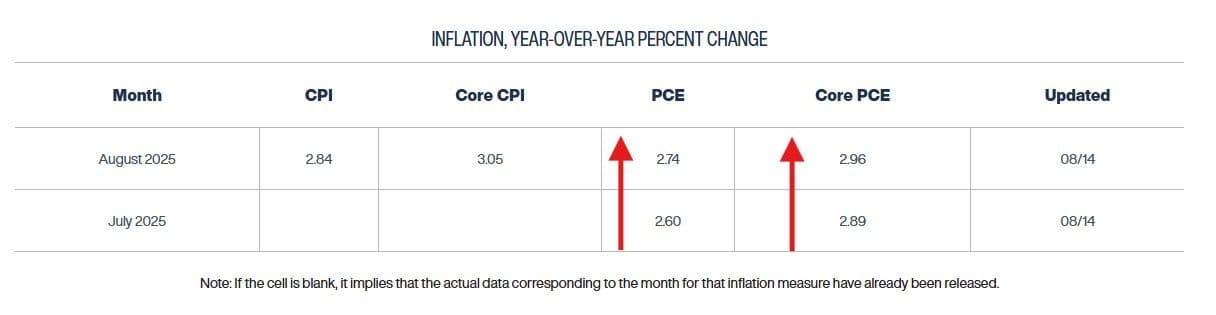

This is where things begin to get interesting. Let’s start with PCE. The Fed is forecasting a median PCE rate for 2025 to be 3%; the last print was 2.6%. The Fed is already forecasting noticeably higher inflation as of June (the last SEP report) through the rest of the year. The last time PCE was 3% was in 2023, so if that is their median as of June for the rest of 2025, they are seeing upside risks in inflation through the rest of the year. That risk seems to be coming true as disinflation seems to have stalled and reinflation is under way with the inflation rate on the upswing.

🚀 Join the Radar Community

Get free access to MacroBase and notifications about new posts and updates.

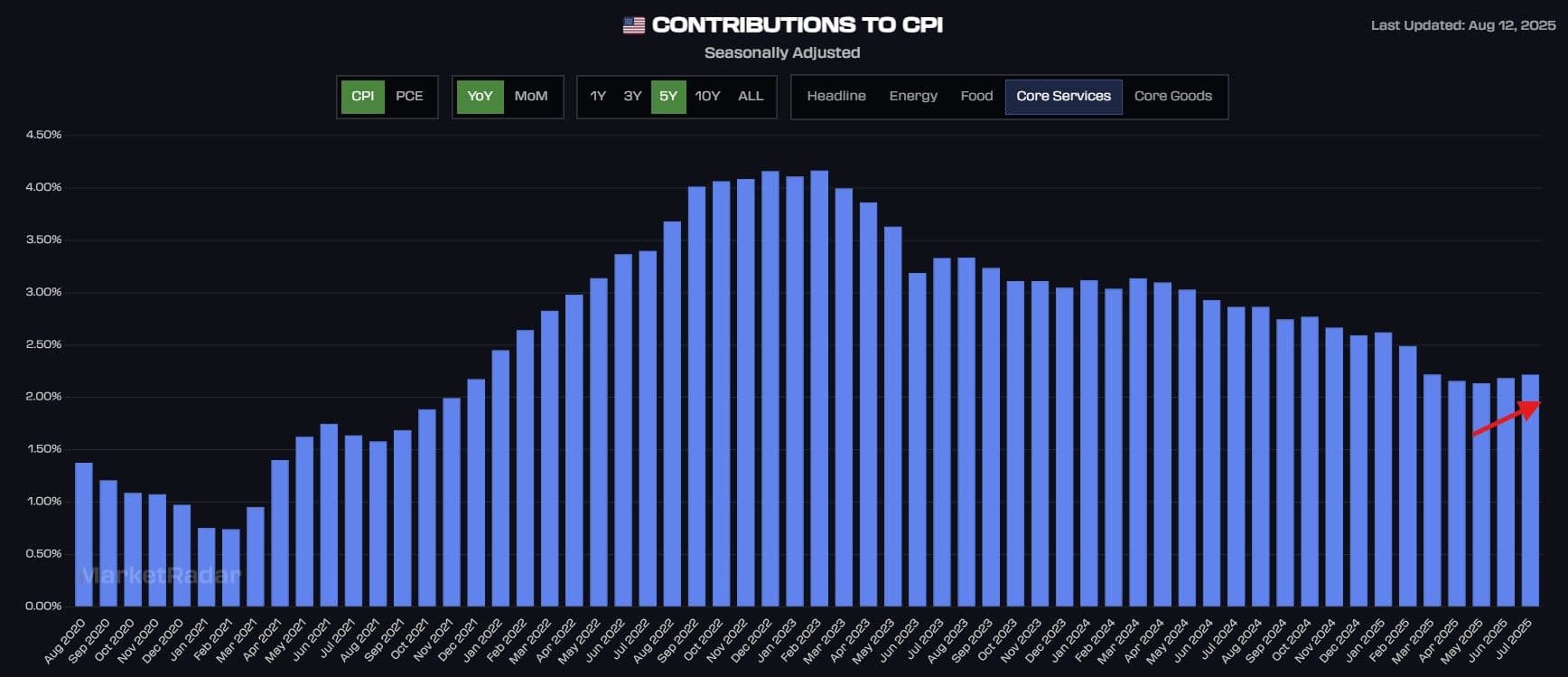

Now, the first and easiest culprit to point at would be tariff impacts as a TRANSITORY (temporary) inflation driver, which should pass through. By default, the Fed SHOULD account for this; however, based on what we’re seeing, it’s likely more than just tariff impacts driving inflation, as you’re seeing things like core services, which have little tariff impacts, bottom out and grind higher. This was one of the main sectors of inflation holding up the basket, and it seems like progress here has stalled. If we’re seeing this, the Fed is too.

Both PCE and Core PCE, based on the Cleveland Fed, for August, are showing continued signs of rising. There's a good chance that if this pace continues, we'll see both 3% headline and core PCE prints by the fall. This is just another signal that inflation risks aren't dead just yet, therefore leaving us with uncertainty around its trajectory, something the Fed does not want to see when reducing policy.

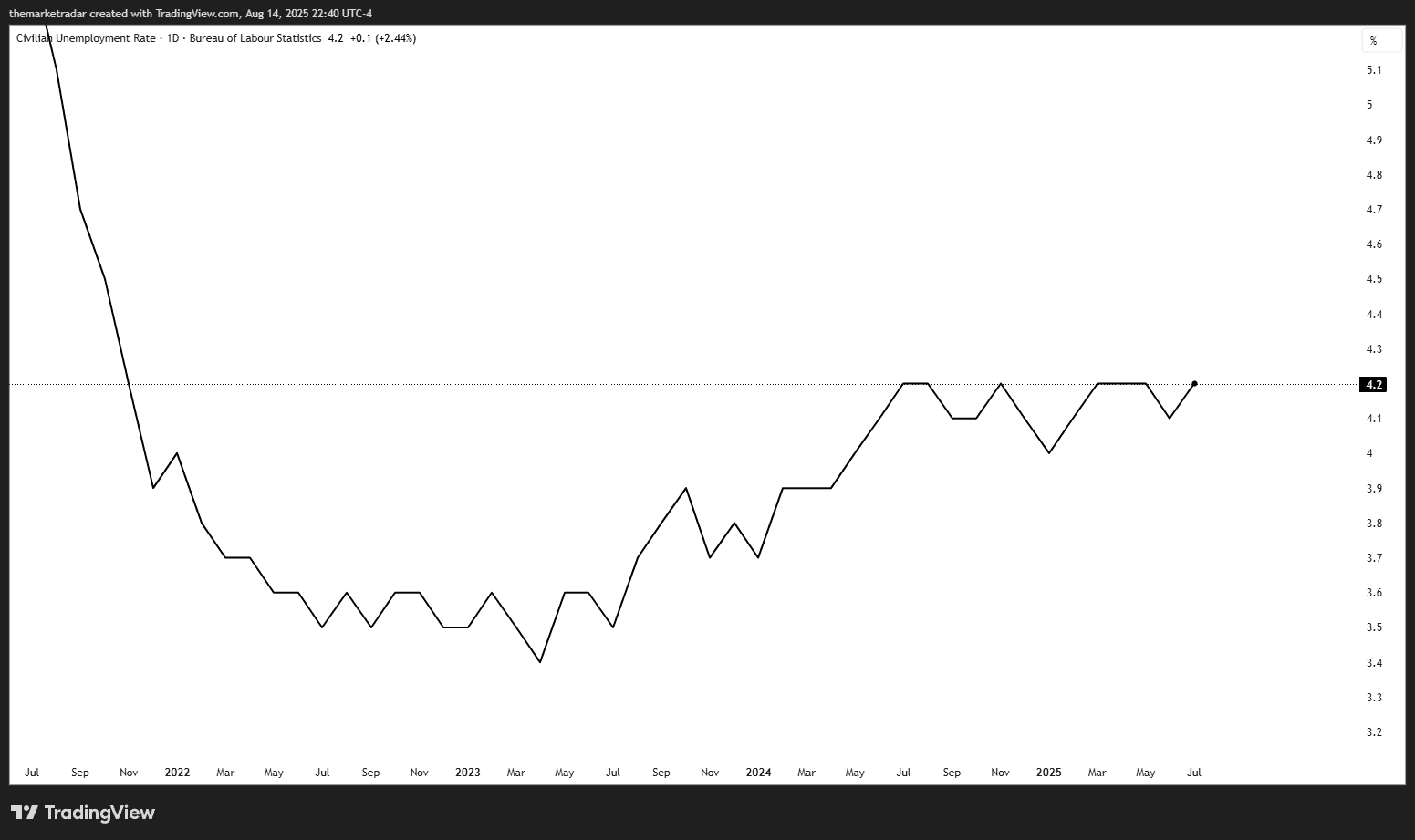

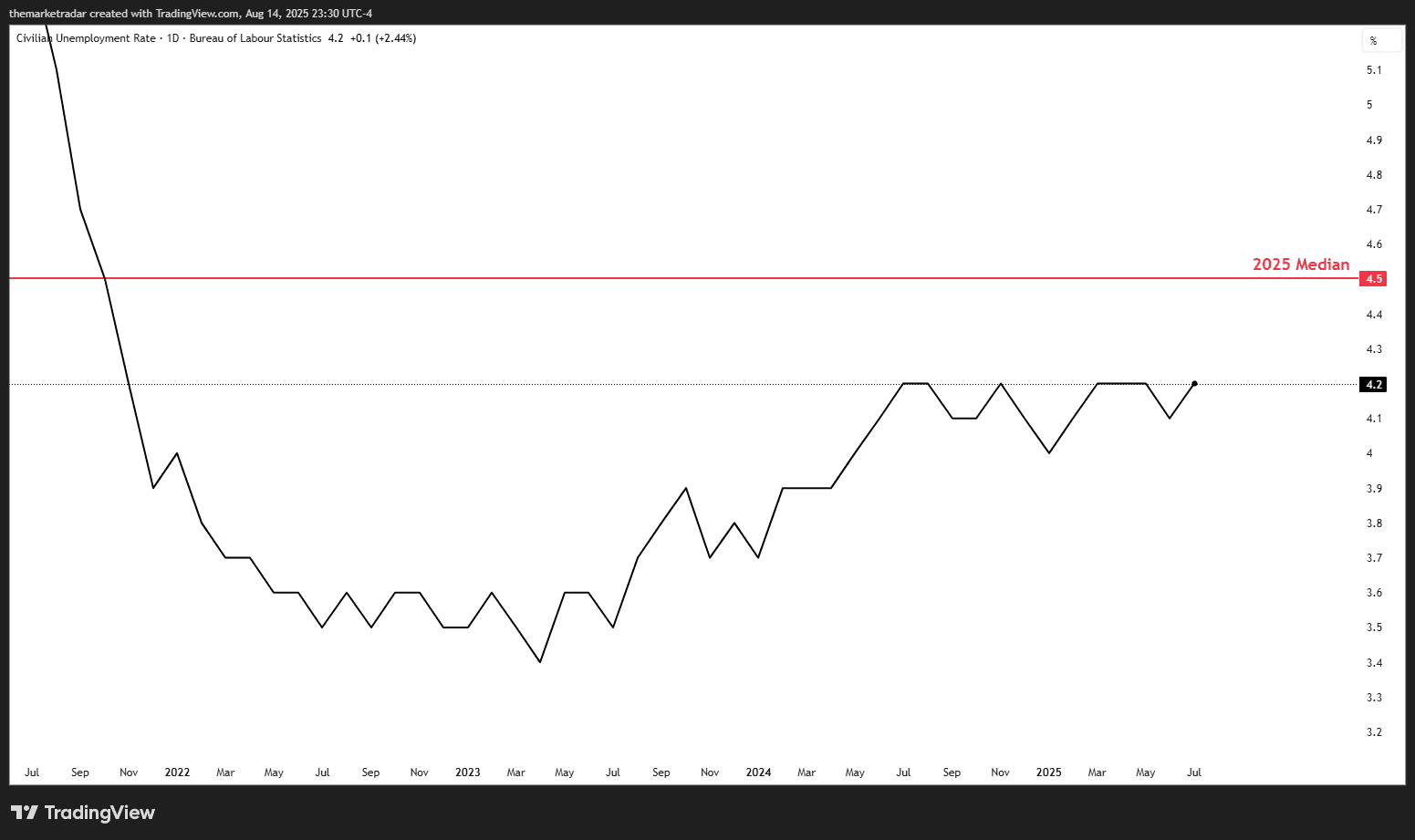

This leads us to the next part of their mandate, labor. Their latest forecast for the median unemployment rate was 4.5%; like PCE, unemployment is still lower than their median for the year, coming in at 4.2%. The last time the unemployment rate was at 4.5% was in 2021, for context. As we mentioned earlier, the most likely culprit anchoring down the unemployment rate is immigration policy. The Fed was expecting much weaker unemployment throught the rest of the year in their last SEP that justified cuts. On this surface, the lower NFP prints seem like a labor market risk, which the Fed may let influence policy, but if the NFP prints are falling because of a lower equilibrium, it’s not as bearish as initially expected. If the unemployment rate remains as anchored as it is, it’s hard to see the Fed become so eager to cut rates, especially with inflation moving the wrong way.

This opens the door to a policy mistake. After taking all this information above in, it would be safe to assume that a Fed, which has been so concerned about moving policy lower too quickly, with inflation that is still not yet at target, and unemployment that is still on the “hotter” side of their estimates, should probably continue in holding rates unchanged.

The market isn’t pricing this, though. The market is expecting the Fed to cut with near certainty at the next meeting, which, while we believe to be a policy mistake, will not be something that breaks the market.

Here’s why.

The market doesn’t care about the semantics of exactly what upcoming meeting has the rate cuts; it is more sensitive to the entire cutting cycle itself. We measure this through the cycle low terminal rate, or “floor”. As you can see here, while we went from 40% probabilities of a rate cut to near 100% over the last few weeks, the cycle terminal rate is little changed, meaning no “new” cuts have come onto the table. It’s when the market fears a recession that the floor begins to rapidly fall, and “new” cuts get priced into the market as the market fears panic at the Fed. We’re not seeing that now, which is why we believe the timing of the next cut to be more semantics rather than “new market information”.

Now, finally, onto the policy mistake. We believe the policy mistake emerging here is easing policy into a labor market that is not actually weak but essentially recalibrating for the supply dynamic shifts from the administration’s immigration policies. The Fed likely has enough time here to continue sitting patiently and letting more data come through to clear up the picture as to whether the labor market is really under stress or simply recalibrating.

We’re over a month away from the next FOMC meeting, there is Jackson Hole next week, and we have another CPI and jobs report that will be released before the Fed meets again. There is so much room here for movement that a 90% chance of a rate cut seems a bit early and likely will continue to shift around as we get closer to the meeting.

There’s a trade to be had. Here’s how we’re trading it…

MOST POPULAR

Unlock Premium Content

The remainder of this content is available to Radar members only. Subscribe to gain instant access.

$65/month

Billed annually at $780 (Save $120)

Access Models which boast 40%+ average yearly returns

Automated Portfolio Signals (RQF Strategy)

Live Calls with experienced traders

QuantBase Dashboard with macro regime models

DDAP TradingView Indicator

Real-time portfolio updates

Private Discord Channels

Lifetime Price Lock|Instant Access