Liquidity vs Collateral - The Money Market Crisis 06.14.23

With the financial industry abuzz over the upcoming supply shock resulting from the treasuries issuance wave to replenish the TGA (Treasury General Account), it is crucial to gain a comprehensive understanding of the mechanics behind the short-term funding mar

With the financial industry abuzz over the upcoming supply shock resulting from the treasuries issuance wave to replenish the TGA (Treasury General Account), it is crucial to gain a comprehensive understanding of the mechanics behind the short-term funding market, specifically focusing on money market funds (MMFs) and their impact on the forthcoming issuance.

As of June 2022, MMFs accounted for approximately 30% of all outstanding bills, making them one of the key players in the treasury bill market, excluding the Federal Reserve. You may wonder why MMFs are inclined towards investing in bills. The answer lies in the duration restrictions imposed on MMFs. These restrictions require that 10% of their assets be in highly liquid assets that can be readily converted to cash (such as cash itself and repurchase agreements), 30% be in assets that are liquid on a weekly basis (such as treasury bills and government agency debt), and the weighted average maturity of the fund be 60 days or less.

Consequently, MMFs find themselves compelled to focus on the front end of the treasury yield curve, which represents the shorter-term maturities. However, this does not imply that MMFs are limited to one asset allocation. Typically, unless they have specific mandates, MMFs operate in various markets, including treasury bills, commercial paper, and repurchase agreements. This understanding is crucial in comprehending the current situation in the repo market. Before delving further into that, let's provide a high-level overview of the repo market.

What exactly is a repo transaction? In simple terms, it involves a collateralized swap, usually with government securities, that has an expiration date, typically one day. It is important to note the distinction between a repo transaction and a reverse repo, which is a facility provided by the Federal Reserve. The repo market is quite sizable, with banks engaging in such transactions on a daily basis. To simplify the repo market:

Institution A: Has excess cash and seeks to generate a return on it.

Institution B: Has an excess of treasury securities compared to cash and requires cash to balance its operations.

In a repo transaction, at the end of the agreement, the securities or cash are returned to their original owners. Institution A reclaims its cash, and Institution B retrieves its securities, excluding the interest paid for borrowing the cash.

Repo transactions are routine within the banking ecosystem, and the average

interest rate at which these funds are borrowed is referred to as the Secured Overnight Financing Rate (SOFR). This rate is known as the market-priced "risk-free rate".

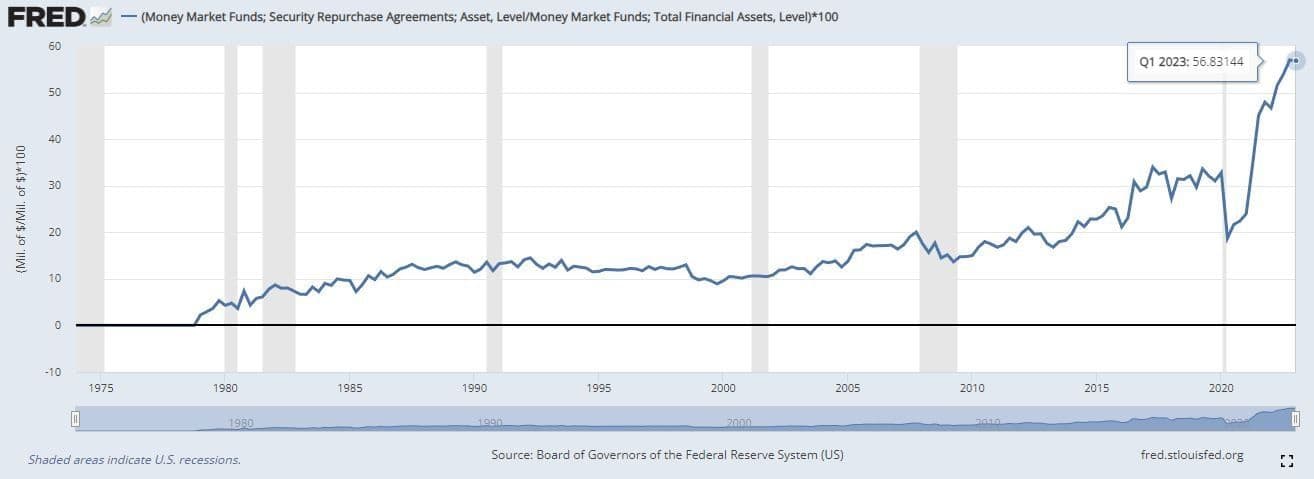

Understanding this is crucial because MMFs can act as Institution A, utilizing their excess cash to engage in repo operations. Historically, between 12-20% of all MMF assets were invested through the repo market. As of Q1 2023, this figure stands at 56%.

However, it's important to note that the repo market allocation of MMFs is not solely comprised of private transactions; it also includes cash held in the Federal Reserve's reverse repo facility. This facility is called "reverse repo" from the Federal Reserve's perspective. In the scenario outlined earlier, Institution A engages in a repo operation, and Institution B receives the opposite end of the transaction, making it a reverse repo.

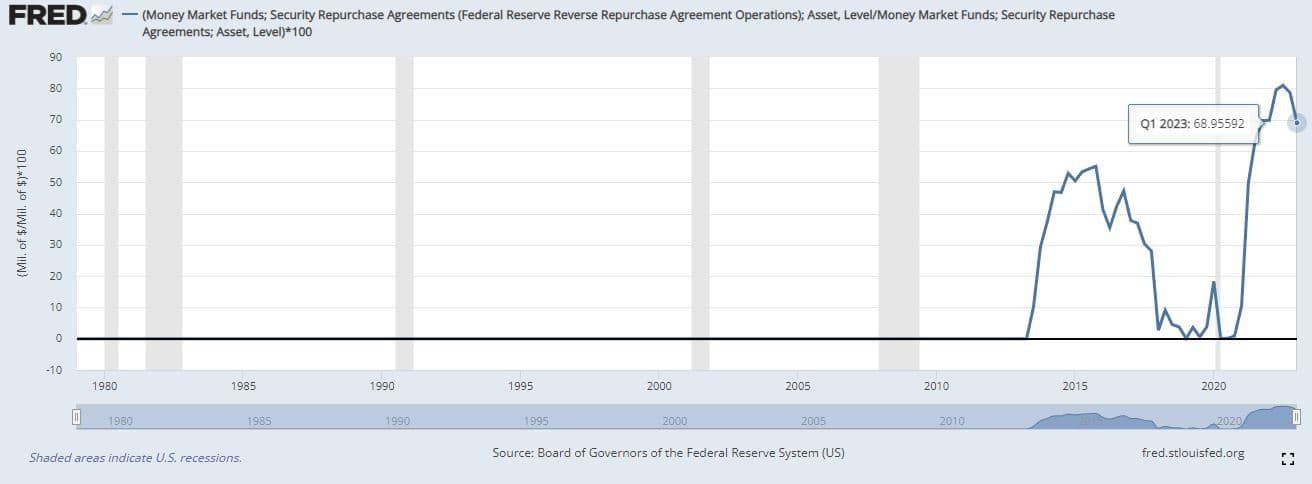

Historically, an average of 20-30% of MMF repo allocations involved the Federal Reserve. As of Q1 2023, this figure stands at around 70%. This interconnection ties everything together, and by understanding the aforementioned context, we can comprehend the following events.

🚀 Join the Radar Community

Get free access to MacroBase and notifications about new posts and updates.

To put it simply, MMFs are focused on pursuing higher yields. They will invest where they can attain the best possible return within their risk profile. There is generally no significant difference in risk between buying a treasury bill and participating in the Fed's reverse repo facility, as the MMF will most likely receive a treasury bill as collateral for its cash. (Remember, when MMFs engage in the Fed's reverse repo facility, they are Institution A, while the Fed is Institution B.) Consequently, MMFs will migrate to wherever the yield is most attractive.

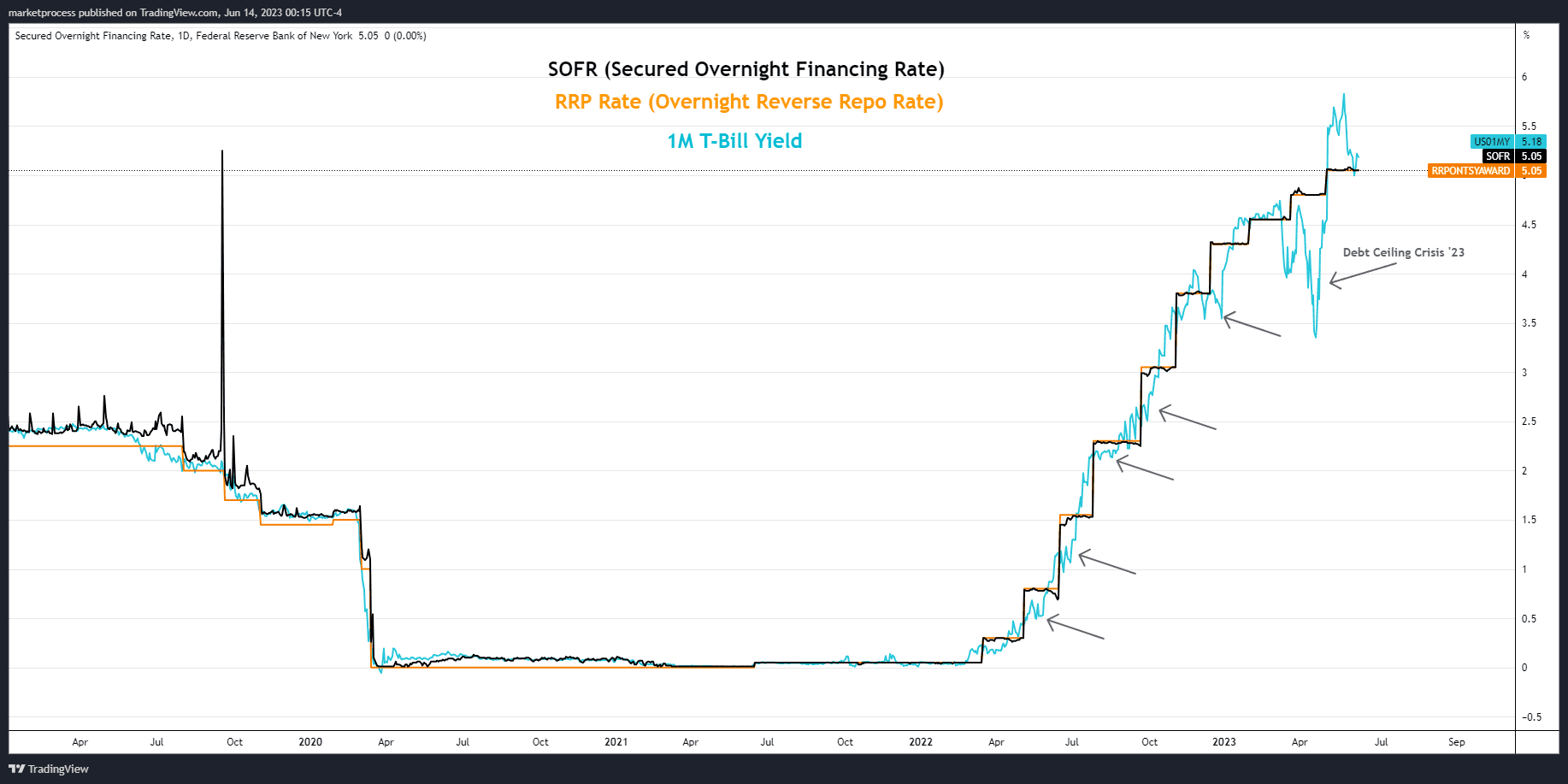

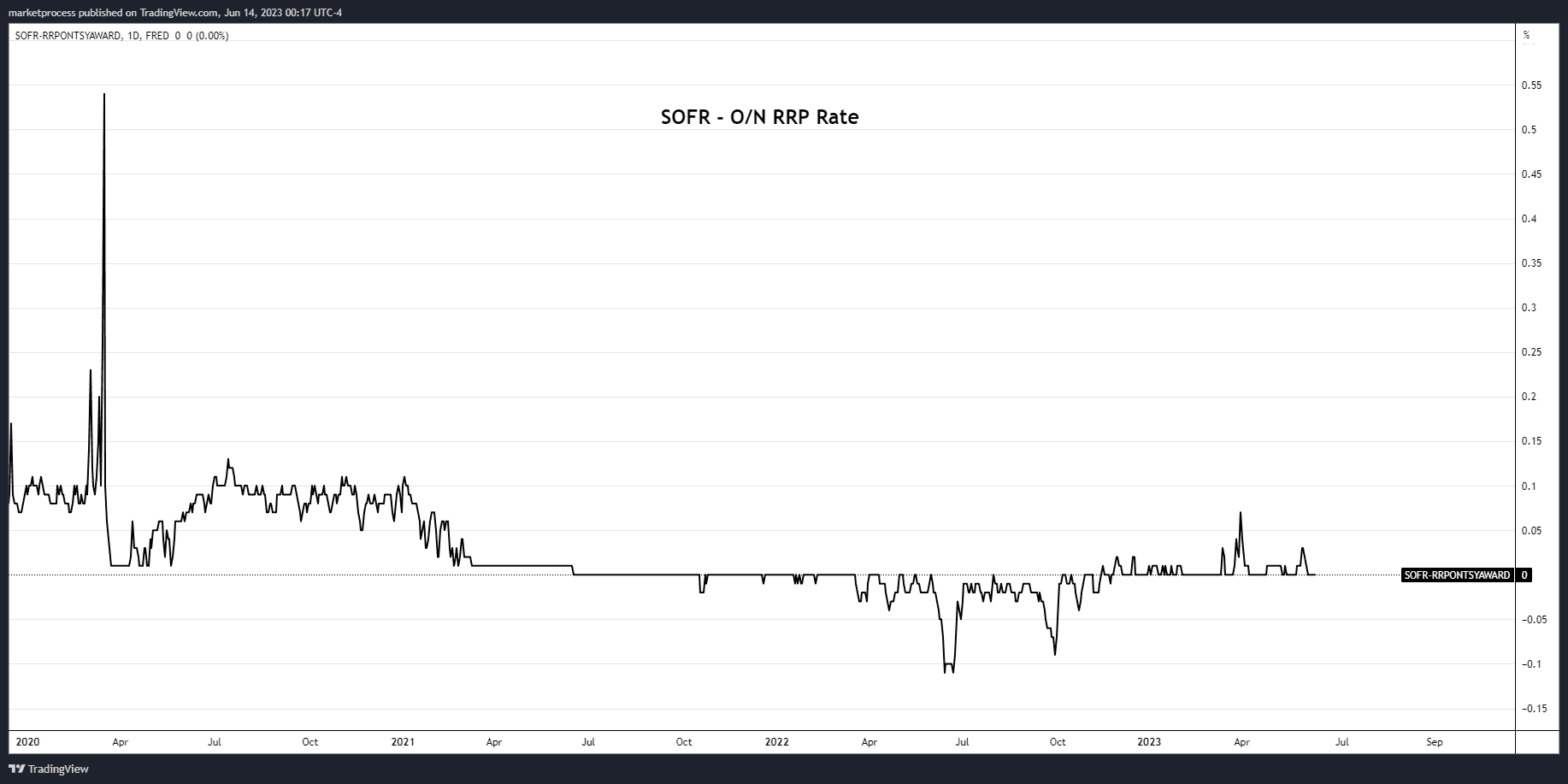

Now, let's examine three interest rates, two of which were mentioned earlier: the SOFR rate, the reverse repo rate (RRP), and the one-month treasury bill rate. An immediate observation is that the treasury bill rate exhibits significant fluctuations, often surpassing or falling below the SOFR rate. The most recent decline in the bill rate can be attributed to concerns surrounding the debt ceiling. Additionally, the SOFR rate struggles to surpass the fixed rate offered by the Fed's reverse repo facility.

This chart effectively illustrates that the short-term dollar funding market is saturated with excess cash, and there is an insufficient supply of collateral (treasuries) to meet the demands of the repo market, resulting in yields that are less competitive and or equally competitive than the fixed rate provided by the Fed throughout the rest of the market.

The SOFR rate can be considered the market-priced equivalent of the Fed's overnight reverse repo rate. By subtracting the overnight reverse repo rate from the SOFR rate, we can observe that for most of 2022, the spread was negative. This indicates that the private sector's ability to engage in repos and the supply of treasury bills were stretched to their limits in meeting the demands of the money market assets.

In recent days, Janet Yellen has made it clear that the Treasury will design treasury offerings to be highly appealing to market participants. Essentially, she is highlighting the substantial surplus of eager buyers at the front end of the yield curve with a dearth of supply. The Treasury aims to address this and fulfill the demand. Currently, there are over $5 trillion in money market funds. Remember, the average maturity of these funds must be 60 days or less. Therefore, over a few months, it is highly likely that MMFs will absorb any short-term bill issuances.

Since MMFs are yield-focused, as long as treasury bills yield more than the Fed's overnight reverse repo rate, money will flow out of reverse repos and into bill issuances.

Ultimately, the Treasury will not sustain this pace of issuances. This means that MMFs will not have an unlimited supply. The underlying issue lies in the excess cash within the system, which the Federal Reserve is undoubtedly aware of. As they continue Quantitative Tightening (QT), the Fed will withdraw money from the system and open up parts of the treasury curve for MMF buyers as they gradually unwind their treasury positions.

Let’s not forget that between 2020 and today M2 money supply has increased ~$5T or 30%, accounting for the recent decline off the peak. That’s still 5T dollars in less than 3 years. It’s likely some of this is cash jamming the system for now and will continue to do so for some time. The benefit though, is it seems most of it is off the street and that has demand implications on consumers which should help keep inflation on trajectory.

In conclusion, considering that the treasury issuances are not duration-related (which MMFs cannot purchase), it is unlikely that we will see negative effects on risk assets or long-term bond yields. Long-term bonds and stocks move off of duration risks (inflation, growth, etc). Any move in bonds will be due to larger economic implications with liquidity for the front end of the curve not coming from long bond or stock sales. MMFs already have a line of buyers eager to invest their sidelined cash at the front end of the yield curve.

I'd like to summarize the above a little further to add some more clarification. The Fed's Reverse Repo facility is the repo of last resort. Meaning, they set the floor in the market for returns on excess cash. What you're basically seeing is an unconventional repo crisis, where instead of participants not having enough "funds", there isn't enough "collateral". MMF would not allocate dollars to the reverse repo if there were alternates out there paying a higher yield. Typically the Fed's RRP Facility acts as the FLOOR and the rest of the market trades higher. The fact the rest of the market CAN'T trade higher is telling you that we've got bids slammed across the arena and that is only possible when cash is ample and collateral for those cash swaps is not. So in a way...the upcoming treasury issuance of bills is very much needed.