8 MIN READ·AUGUST 30, 2025

Macro Update: The Labor Surprise Nobody Is Talking About

This Friday’s jobs report might be the most pivotal data release of the year, and not just because every labor print feels like “the most important one ever.” This time, it actually might be. We're going to explore why we believe there's a hole in the labor na

MR

CONTRIBUTOR · MARKET RADAR

This Friday’s jobs report might be the most pivotal data release of the year, and not just because every labor print feels like “the most important one ever.” This time, it actually might be. We're going to explore why we believe there's a hole in the labor narrative and things may not be as they seem.

Before we get into it, this next labor print is the final print before the next FOMC meeting, but it also comes just after Jackson Hole, where Powell came out unexpectedly dovish, making it clear that any weakness in the labor market could change the tone of policy going forward.

Since then, the vibes around labor have shifted. The media, the Fed, and the street have all latched onto a narrative of increasing fragility. We've seen persistent chatter about the sustainability of labor strength, fueled in large part by the wave of negative payroll revisions over the last 30 days. It got so loud, the Administration even ousted the head of the Bureau of Labor Statistics.

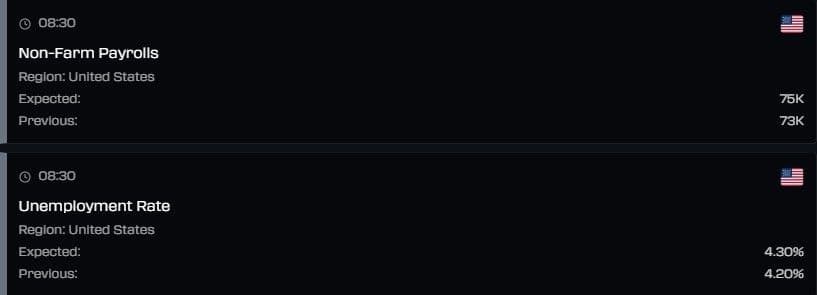

Here's what Wall Street is expecting next week:

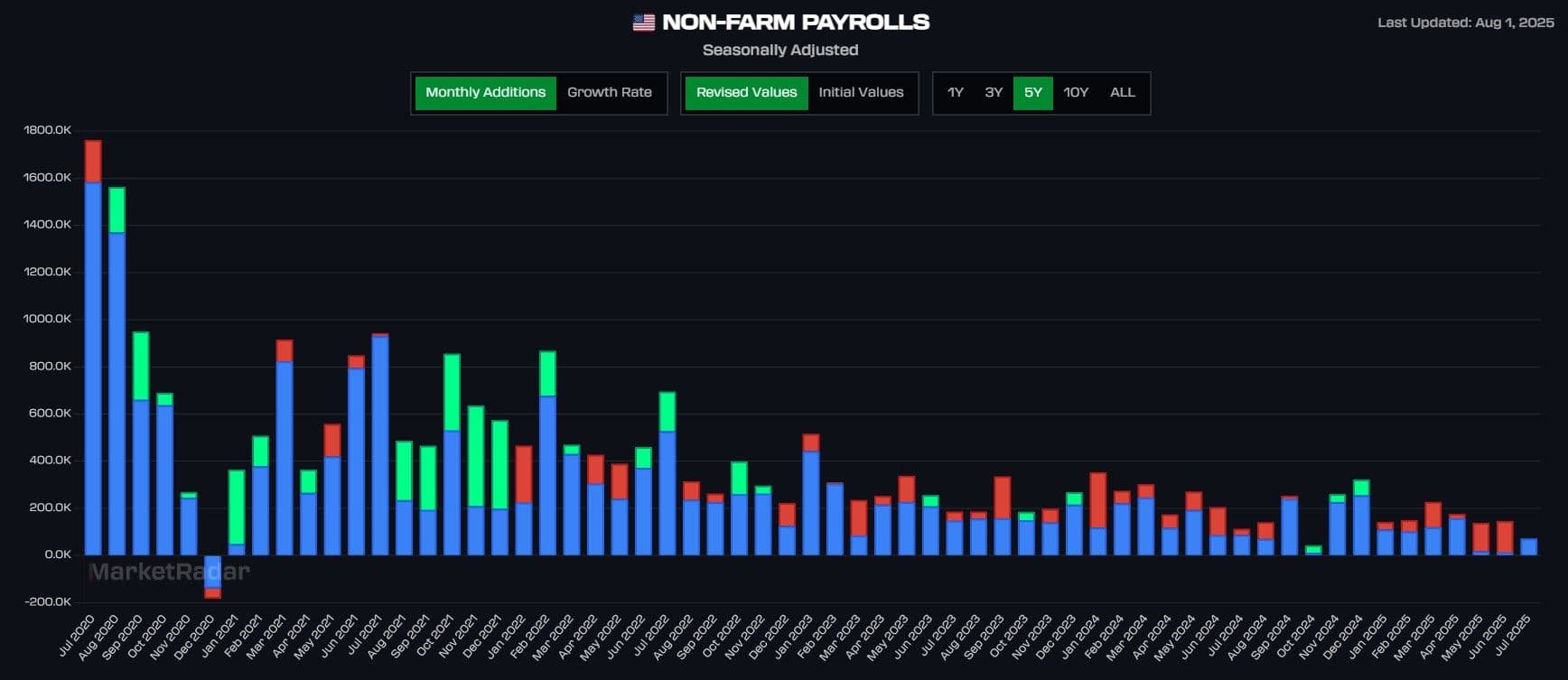

The consensus takeaway has been that payroll growth has stalled at fragile levels, labor has risks of cracking, and unemployment is likely next. I firmly believe this narrative has a hole in it. The market's fixation on monthly payroll prints is understandable; they’re flashy, easy to headline, and deliver a clean, binary number for traders to react to. But if you're actually trying to gauge labor market stress, payrolls won’t get you there. They only show inflows of how many new jobs are being added. The reason why understanding what payrolls represent is important is the exact dynamic we've been witnessing throughout this year. Payroll growth, measured by jobs added, has been declining and under additional pressure from heavy negative revisions.

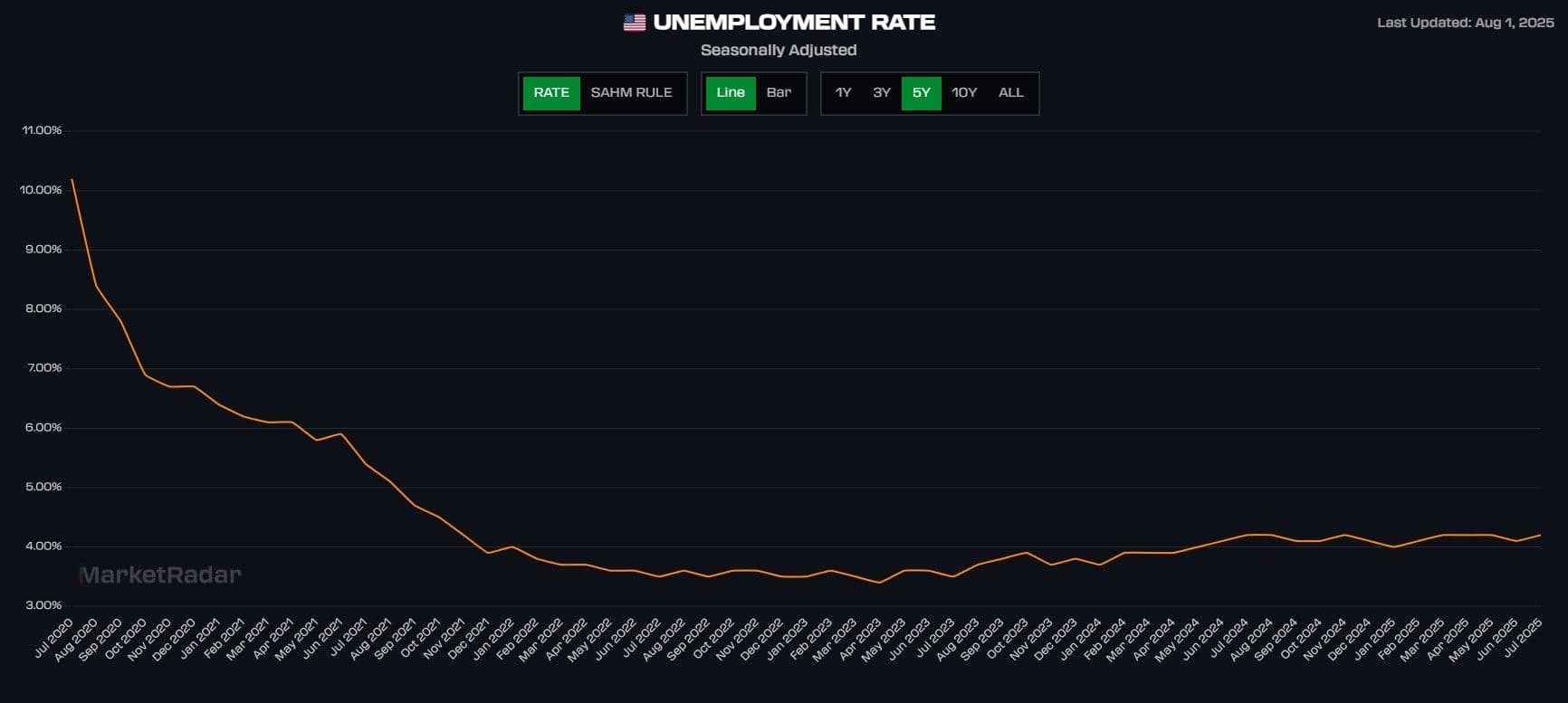

Yet the unemployment rate? Barely changed.

So it’s pretty clear that payrolls alone can’t explain shifts in the unemployment rate. We’ve seen massive negative revisions over the past few months, and yet the unemployment rate hasn’t budged. What’s causing that disconnect?

I won’t go too deep into the weeds here; this theory’s been passed around plenty, but the short version is: the labor market no longer needs the same level of new job creation to stay stable. Immigration dynamics, policy shifts, and broader demographic changes have effectively lowered the baseline of how many payroll gains are needed to keep things functioning.

If we run with that idea, then it implies something obvious but underappreciated: there’s a third variable in the labor equation that’s getting ignored. We always talk about payrolls (jobs added) and unemployment (people out of work), but rarely are we talking about what’s happening in between, specifically, the number of people being let go.

If payrolls are slowing but not lifting the unemployment rate, does it mean that fires are also slow/low, therefore not leading to a material rise in net employment? Actually, yeah, that seems to be the case. Similar to the unemployment rate, we're seeing a very consistent initial jobless claims number, indicating that the slowdown in payrolls is not translating to jobless claims.

At the most recent Jackson Hole speech, Powell did address this dynamic by noting that “While the labor market appears to be in balance, it is a curious kind of balance that results from a marked slowing in both the supply of and demand for workers.” So it's clear the Fed has some recognition of this dynamic as well, and this is where I think we need to dive deeper to truly understand the hole I mentioned earlier that exists in this labor narrative.

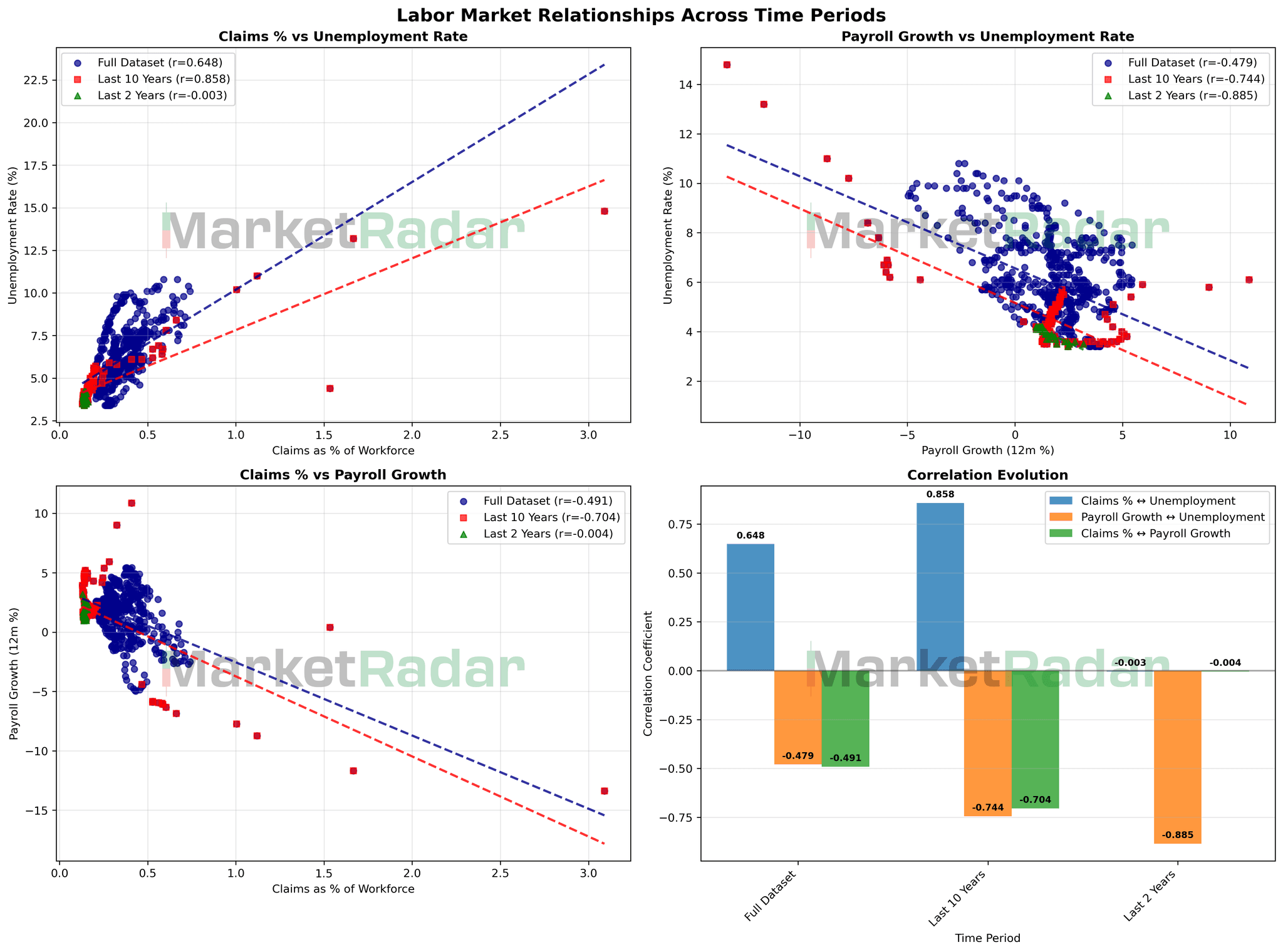

A less conventional way to analyze the labor market is by looking at jobless claims not just in absolute terms, but as a percentage of the total workforce. We will refer to this as the claims rate, noted as claims as a % of workforce in the graphics. This framing helps put weekly claims into context, showing the actual rate at which workers are exiting employment rather than just the raw headline numbers.

The measurement does require some care. Since payroll levels are subject to revisions, we use the prior month’s reported payroll base when comparing to the current month’s average weekly claims. While revisions can swing by several hundred thousand, they’re unlikely to meaningfully distort the ratio when the workforce base is roughly 150+ million. This approach keeps the measure consistent while still capturing the dynamics of the labor market. The reason we report the average weekly claims and not the total is to prevent bias fluctuations from 4 and 5-week months.

With that dataset in place, we can then run correlations between the claims rate and other labor market indicators. The goal is to see how strongly these proportions track with unemployment, payroll growth, and broader measures of labor market weakness. The chart below lays out those relationships across different time horizons. Note that the full dataset starts in 1967.

🚀 Join the Radar Community

Get free access to MacroBase and notifications about new posts and updates.

This analysis highlights a few key takeaways. First, there is a consistently strong relationship between unemployment, payroll growth, and claims rates. The most notable correlation is between the claims rate and the unemployment rate, particularly over the last 10 years. We also ran a 2-year test to isolate the post-pandemic labor environment. However, because claims and unemployment have both been relatively stagnant, the dataset lacks enough variation to produce meaningful correlations. The 2-year results are better seen as confirmation that there simply hasn’t been much movement, while a 5-year window would risk overweighting the pandemic’s distortions.

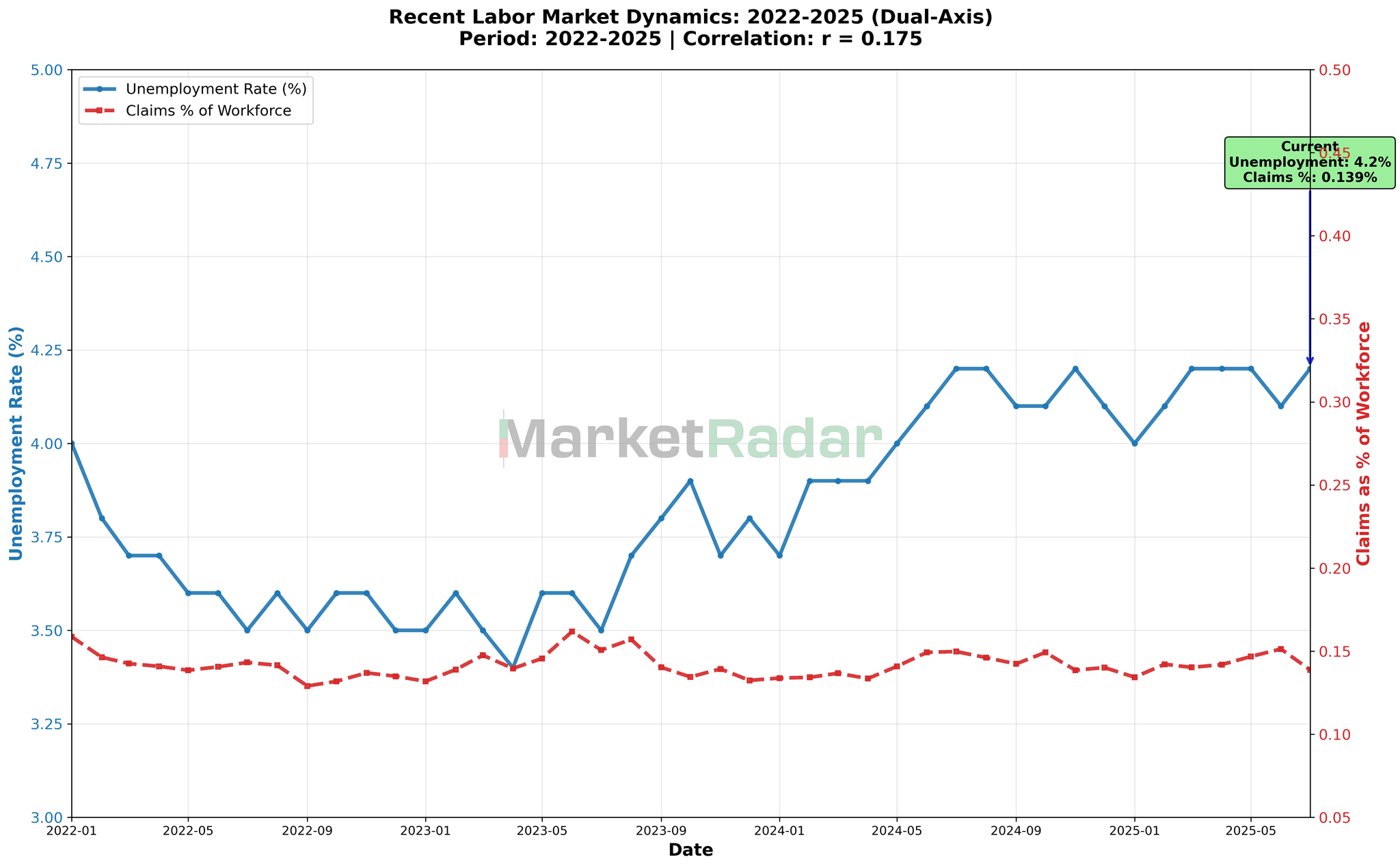

Since we established that the claims rate has statistical significance, we can go a step further by overlaying the claims rate and the unemployment rate to get a better visual of where we are today.

As mentioned earlier, the lack of variation in post-pandemic labor market data skews short-term correlations, which is why I place less weight on them. In a truly weak labor market, we’d expect the claims rate to climb meaningfully. Instead, while unemployment is sitting near the upper end of its recent range, the claims rate remains well anchored and far from stress levels. That suggests unemployment is more constrained than fragile; the rate may drift higher at the margin, but with the claims rate this stable, a sharp deterioration looks unlikely, at least for August. Think of unemployment as strapped with a weighted vest: it can move, but it’s not going very far unless the claims rate starts to break out.

This circles back to the broader narrative of labor market “fragility.” Payroll growth has clearly slowed, with hefty downward revisions, yet unemployment has barely budged from where it was last summer. That disconnect points to the likelihood of a lower breakeven payroll rate—the economy can sustain smaller monthly job gains without translating into higher unemployment.

In fact, as long as the claims rate remains range-bound, there’s a risk we’re repeating last summer’s pattern: a patch of weakness that looked concerning in real time but ultimately gave way to re-acceleration later in the year and long-end rates up as the Fed essentially eased into a rebound. The risk ultimately is the Fed easing policy into an environment that really just warrants a lower breakeven equilibrium.

Will the Fed actually cut into this weakness? Probably. But that’s where the risk lies. By trying to preempt a downturn, the Fed could find itself easing into a labor market soft spot that quickly reverses. In practice, the Fed can’t afford to be too early. If unemployment truly breaks higher, that’s harder to control, but cutting preemptively on the assumption of a much lower neutral rate risks overshooting if this weakness proves temporary.

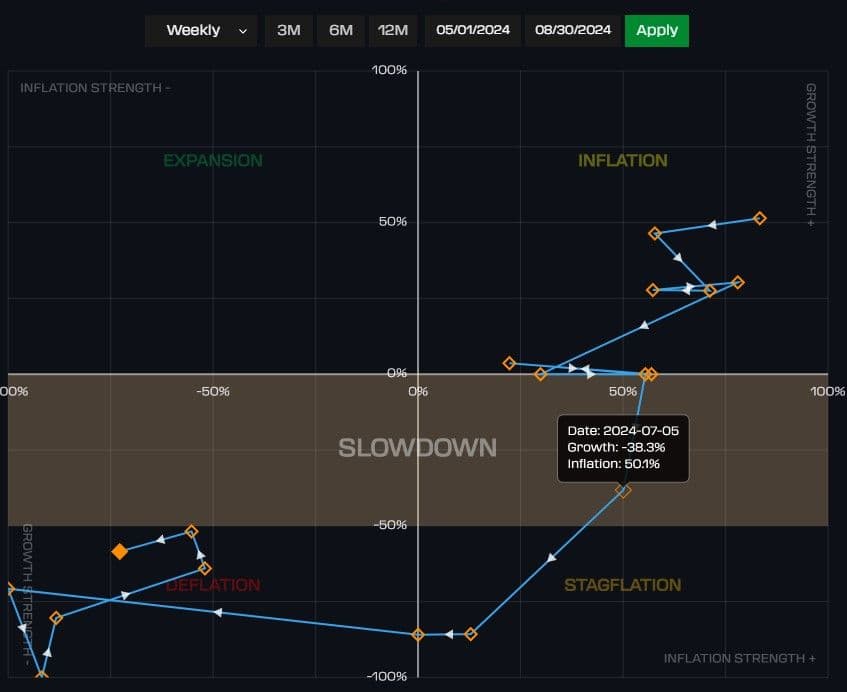

My view here is that the Fed needs to be cautious in triggering a policy mistake, and more dovishness is likely warranted once we can see the claims rate climb more towards its local highs. Labor probably doesn't have the fragility risks being portrayed, and there is a much higher probability than consensus believes that we can see a re-acceleration over the next few months. At the same time, our macro regime system is signaling strong growth and inflation impulses. You can see here that growth and inflation impulses are both above their momentum levels, signaling strong signals in each category.

Interestingly, the more pronounced labor market slowdown we saw last summer, when the Sahm Rule triggered, ultimately proved to be a head fake. Our System had already shifted to Risk-Off by mid-summer, ahead of the major equity drawdown, allowing us to pivot before consensus caught on.

All things considered, we see the labor market carrying higher odds of reacceleration than of sustained weakness, and our regime model backs that view, for now. With the Fed highly likely to respond to these labor signals, the greater risk is a policy mistake: easing too quickly and unintentionally loosening conditions more than the economy requires.

At Market Radar, our focus is on stripping away the noise. The macro regime system drives our positioning, and as long as it keeps us in Risk-On, we stay there, and only the data will shake us out. If our labor market thesis is correct, a more hawkish Fed wouldn’t be a negative; it could even be bullish, since it implies the economy is holding up better than expected. Conversely, if the Fed turns dovish into a reacceleration, that could fuel devaluation trades and lift risk assets as markets reprice policy that’s too loose for the backdrop.

Put simply: the market expects the Fed to ease. That expectation itself is an admission that the Fed is signaling it will prioritize avoiding job losses, even if it means tolerating more inflation. Not only is the market expecting the Fed to cut into this, but it's also dropping the cycle terminal rate, implying that more cuts are being added to the cycle in the process. I'll leave this off with a simple question: Do you think we should cut rates into this?

If you’re reading the free version and want deeper access to our work, you can sign up below for access to our interactive dashboard featuring our models that update daily in real-time!

MOST POPULAR

Unlock Premium Content

The remainder of this content is available to Radar members only. Subscribe to gain instant access.

$65/month

Billed annually at $780 (Save $120)

Access Models which boast 40%+ average yearly returns

Automated Portfolio Signals (RQF Strategy)

Live Calls with experienced traders

QuantBase Dashboard with macro regime models

DDAP TradingView Indicator

Real-time portfolio updates

Private Discord Channels

Lifetime Price Lock|Instant Access