Recessionary Cracks - 8.01.2024

OVERVIEW As we navigate the shifting tides of the financial markets, it's clear we're in the midst of a significant transition. Over the past month, our system has accurately called the move from Stagflation to a Deflation regime, signaling that a cautious app

OVERVIEW

As we navigate the shifting tides of the financial markets, it's clear we're in the midst of a significant transition. Over the past month, our system has accurately called the move from Stagflation to a Deflation regime, signaling that a cautious approach is more important than ever. This shift, while not entirely surprising, highlights the challenges ahead, especially as we find ourselves firmly in a Risk-Off environment—a space where negative growth strength holds sway and the path to a more optimistic Risk-On scenario feels increasingly narrow. As we dig into our Compound Landing framework, we're at a pivotal moment. The economy has been adjusting to higher rates, but the big question on our minds is whether we can maintain this delicate balance or if we're on the brink of something more serious. In this piece, we'll explore what this means for bonds, equities, and our overall strategy, offering insights to help you navigate the complexities of the road ahead. Let's dive in together and make sense of these uncertain times.

THE SYSTEM

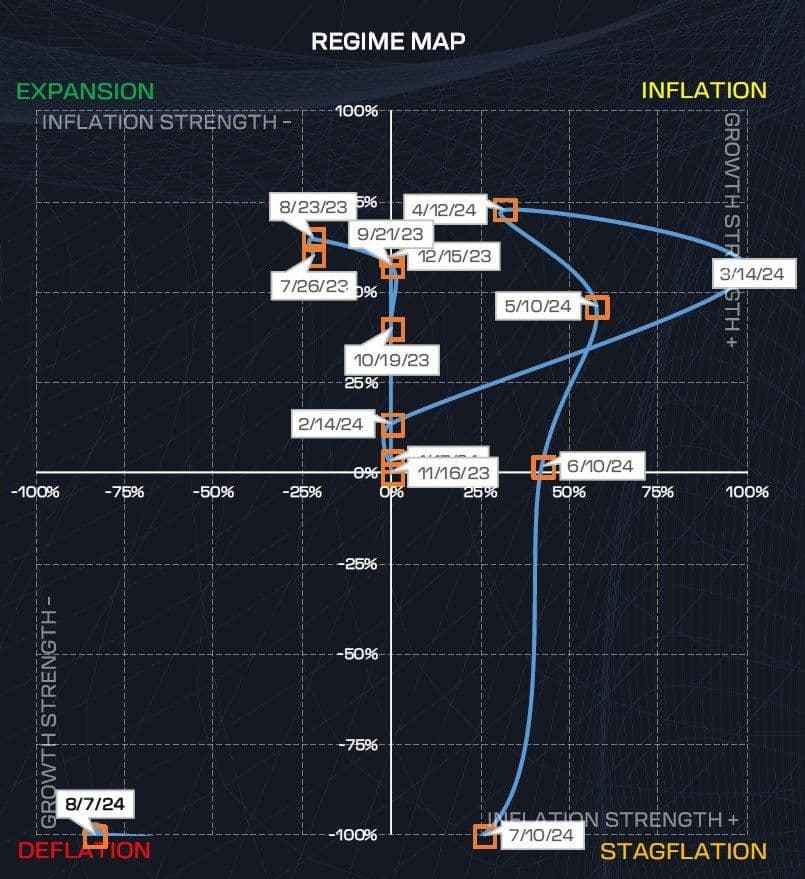

We're over a month into the new risk-off environment, and the landscape has evolved since our last update. Back then, we mentioned that "an acceleration in disinflation without corresponding growth strength could lead us into a Deflation regime." True to form, we've seen a pivot from a Stagflation to a Deflation regime. The System is now signaling Deflation with an extreme level of confidence.

Even with this shift, we remain firmly in what we define as a Risk-Off environment. Both Stagflation and Deflation fall into this category, as they are characterized by negative growth strength. Given the current readings, a transition back to a Risk-On environment, marked by positive growth strength, seems unlikely without a significant reversion in growth strength. While it's not impossible, the path ahead appears challenging.

OUTLOOK

For those unfamiliar with our Compound Landing framework, here's a brief overview. Over the past two years, discussions around soft, no, and hard economic landings have been widespread. The consensus is that soft landings are rare, often merely lulls before a recession. Our Compound Landing framework was specifically crafted for this economic cycle.

It all began when the Fed lagged at the start of the rate-hiking cycle, forcing them to raise rates more aggressively than usual. Although rates have been in restrictive territory for a while, the economy appears to be normalizing. However, the wildcard here is the policy lag – an unpredictable factor. The Fed has maintained peak policy for about a year now, and we are only just starting to observe signs of a softening labor market and slower growth drivers. The economy has been adjusting to these higher rates, but the real concern arises when conditions start to deteriorate.

Our framework consists of four stages, with Stage 3 representing economic normalization at higher interest rates. The catch? Inflation is now close to pre-pandemic levels, and labor markets are weakening. The same policy lags that have allowed the economy to adjust to higher rates with minimal disruption could exacerbate a slowdown as the Fed gradually lowers rates to stimulate growth. This scenario defines Stage 4 of our framework: a recession. In essence, Stage 3 is the soft landing, and Stage 4 is the recession. We believe recessions are unavoidable, and that the soft landing (Stage 3) has already occurred. The key question the market is grappling with now is whether we can maintain Stage 3, or if a material deceleration will push us into Stage 4.

Currently, our outlook, guided by our System, is risk-off. However, being risk-off doesn’t necessarily mean we’re bearish on equities. We don't foresee a full-blown bull market in equities, but if indices can maintain bullish trends, they could see gradual gains. Since we don’t short equity indices or bullish trends, our risk-off stance is more bond-focused. Historically, risk-off periods have presented phenomenal bond opportunities. While it’s rare, there are instances where equities outperform bonds in risk-off regimes. More commonly, both assets can rise, with bonds generally offering more stability and less downside risk.

🚀 Join the Radar Community

Get free access to MacroBase and notifications about new posts and updates.

Given our leveraged position, we focus on high probability opportunities with minimal resistance. In this context, we believe bonds have the potential to outperform equities, especially when leverage is applied. The distinction between Stage 3 and Stage 4 in our Compound Landing Framework is particularly important for bonds. While equities may continue to rise as the economy works towards normalization (Stage 3), bonds also stand to gain if interest rates gradually decline more than what is currently expected. It's reasonable to anticipate slowdowns as the economy adjusts to higher rates. However, if we transition into Stage 4, equities are unlikely to fare well, and bonds should provide a strong hedge against potential equity declines. In our current outlook, bonds offer two distinct advantages, whereas equities present only one. The longer we remain in a risk-off environment, the greater the likelihood of progressing from Stage 3 to Stage 4.

Our base case scenario points to an economic slowdown, with the potential to shift into a recession if left unaddressed. Indicators of such a shift include collapsing commodities, a rise in continuing claims above 2.5 million, and widening credit spreads. While we've observed some pullback in commodities, a slight increase in claims, and widening spreads, we have yet to definitively enter Stage 4. For now, we remain in the “slowdown stage” of Stage 3.

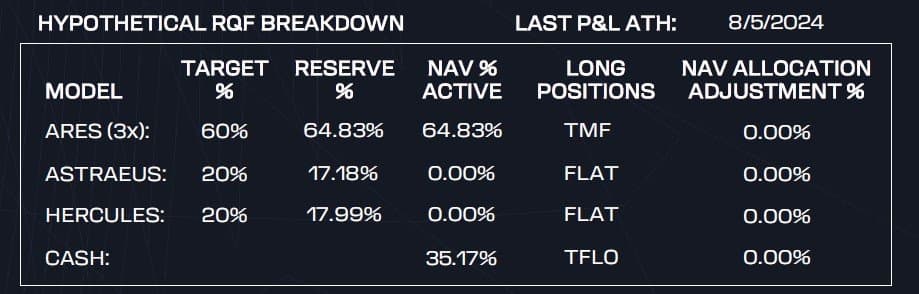

RADAR QUANT FUND (RQF)

The RQF is currently positioned heavily long in US Treasury bonds with leverage, but we've since closed out our short volatility position from the last ledger note. In the past month, we took another stab at Bitcoin, as our Bitcoin model (Astraeus) gradually re-entered a position. Unfortunately, we took that position off at a small loss. I'll be candid—I'm not a fan of Risk-Off regimes. Bonds lack the excitement, and watching economic data decline isn't exactly thrilling. I'd much rather be fully engaged in Risk-On regimes, but this is where the market has led us.

As of this week, the RQF has reached a new all-time high, with over a third of our net asset value currently held in cash. Both our short volatility and Bitcoin models (Hercules and Astraeus) are designed to be dynamic, and capable of opening positions even in Risk-Off regimes, though with smaller allocations. We're staying vigilant for any reversions in volatility or crypto that could present new opportunities. But for now, bonds are the name of the game.

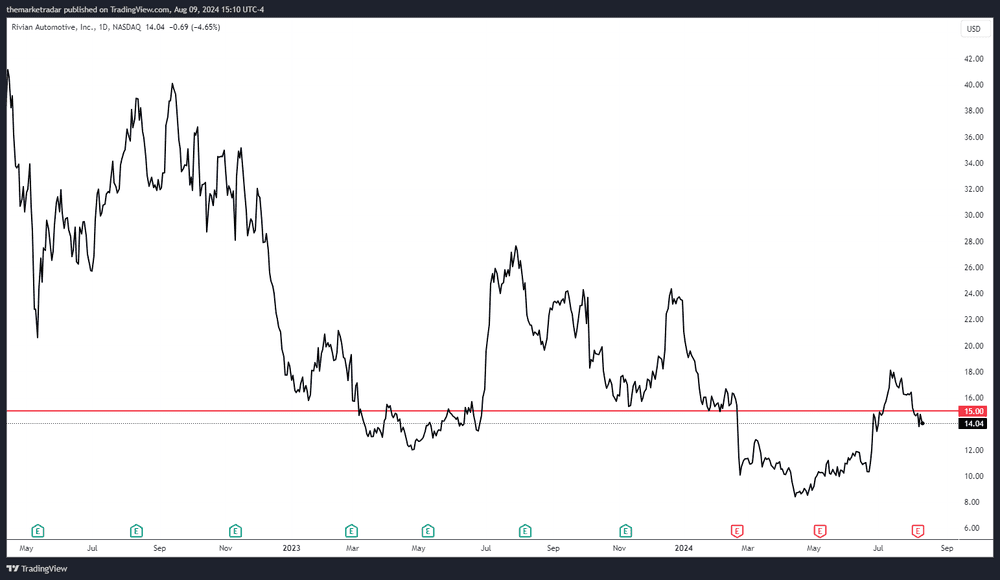

RIVIAN

We started covering Rivian in Q4 of 2023, around $15/share and we formally laid out our thesis in an earlier ledger note which can be found HERE.

Since we laid out the thesis, Rivian is up roughly 40%+ from the $10/share mark to nearly $14/share. We own Rivian around $15/share and we’ve seen the price recover nicely since Q1 of this year. This has been a fundamental play for us from the beginning, exempting it from some of the economic and momentum conditions we’ve explained throughout this post. We’re aware that if we tip into a recession, Rivian’s stock price likely will not bode too well, but we’re buying it today under a long-term vision as a real EV alternate to the behemoth Tesla. If we were to experience a recession, and Rivian were to display improved liquidity and fundamental conditions at that time, we’d likely be open to adding to our position.

Recently, the company released its second-quarter results, reinforcing its confidence in achieving positive gross margins by the fourth quarter. They’ve already begun to see favorable effects from the optimization-related factory shutdowns earlier this year. Our long-term outlook on this company remains unchanged and we look forward to the company meeting and possibly exceeding expectations.