Rivian: The Bull Thesis

We’ve been following Rivian for a while now, sharing quick thoughts on X and our podcast since early 2024, but it’s time to go deeper. In this piece, we’re laying out our full bull thesis and why we believe Rivian has the potential to be a long-term winner. Bu

We’ve been following Rivian for a while now, sharing quick thoughts on X and our podcast since early 2024, but it’s time to go deeper. In this piece, we’re laying out our full bull thesis and why we believe Rivian has the potential to be a long-term winner. Buckle up, because this is where the story really accelerates.

Rivian doesn’t need much introduction. The company builds electric vehicles, specializing in SUVs and commercial vans, and has quickly carved out a unique spot in the EV landscape. Founded in 2009 by RJ Scaringe, Rivian spent over a decade in stealth before starting production in 2021, and now it’s preparing for the most important chapter in its history.

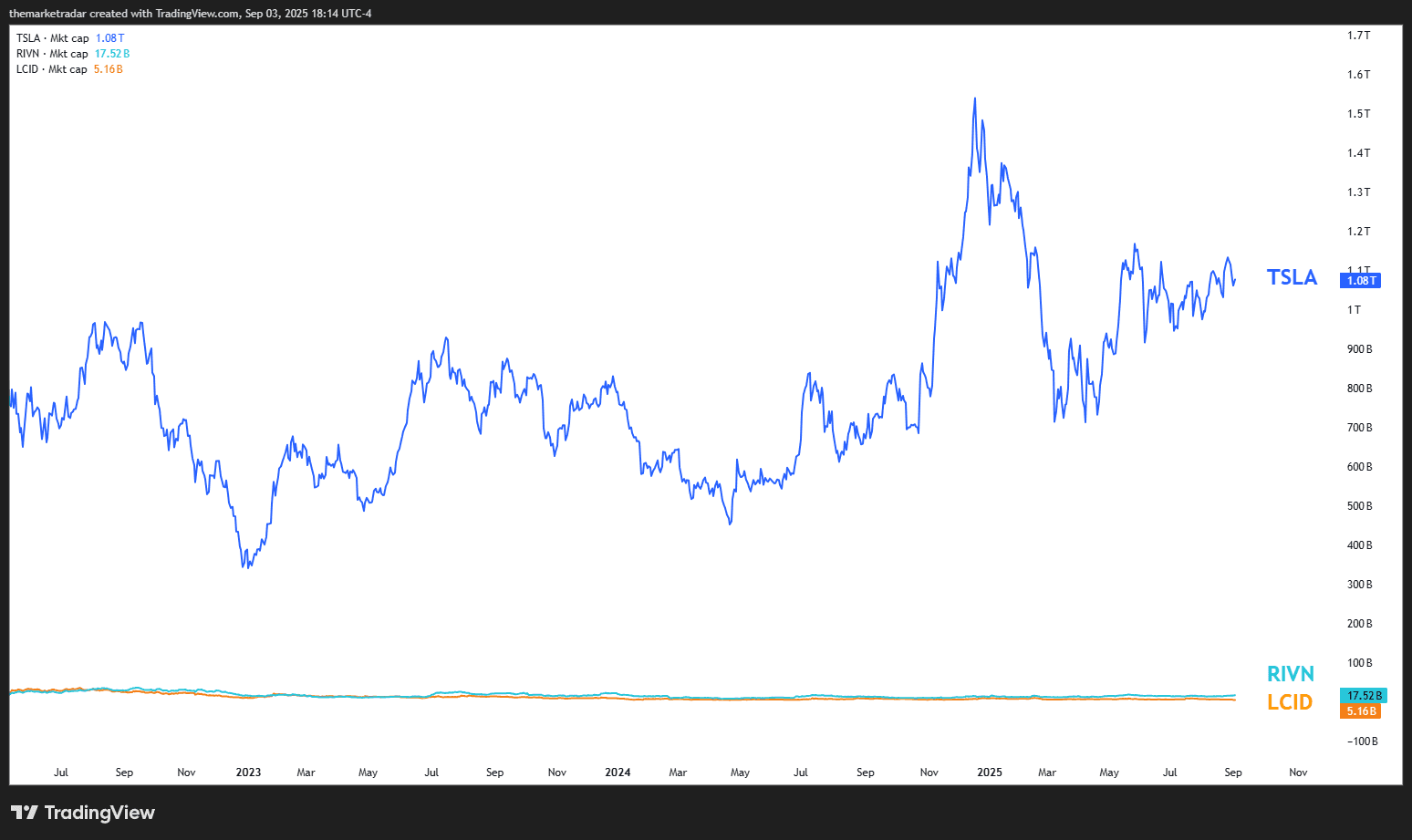

What makes the setup so interesting is how few players are in Rivian’s lane. In North America, there are only three pure EV automakers listed publicly: Tesla (TSLA), Rivian (RIVN), and Lucid (LCID). With a market cap of about $17.5 billion (around $14.44/share), Rivian sits squarely between Tesla’s trillion-dollar behemoth and Lucid’s $5 billion niche. That positioning makes it a rare, high-upside name in a very thin field.

Before we dive into Rivian’s future, it’s important to frame the competitive landscape. Yes, Tesla is still the undisputed king of EVs, but comparing Rivian’s $17.5 billion market cap to Tesla’s trillion-dollar behemoth is apples to oranges. Tesla isn’t just a car company; it’s a sprawling business with energy storage, solar, and even long-term bets on robotics and AI. Rivian, by contrast, is a focused EV manufacturer, carving out its own lane in adventure SUVs and commercial vans. The point here isn’t to label Rivian “the next Tesla”, that’s lazy analysis. It’s to recognize Rivian as its own company with a different strategy, different hurdles, and in many ways, a different era of EV adoption.

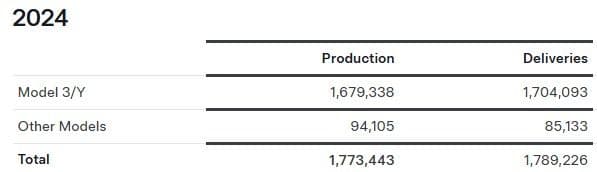

Now let’s ground this in numbers. In 2024, Rivian delivered 49,476 vehicles, a tiny fraction of Tesla’s 1.77 million, but still meaningful for a young automaker. Importantly, Rivian already sells over five times as many vehicles as Lucid, which managed just 9,029 deliveries. That puts Rivian firmly in the number two spot among pure EV players in North America, with a real chance to widen the gap.

One of Rivian’s key differentiators is its commercial vehicle strategy, anchored by Amazon. Amazon isn’t just a customer; it’s Rivian’s largest institutional shareholder, holding about 158 million shares (~14%). The partnership gave Rivian a guaranteed launchpad for its electric delivery vans (EDVs), with Amazon deploying over 20,000 vans already. And since exclusivity ended in 2023, Rivian has started offering these vans to other fleet customers as well. It’s estimated that roughly half of Rivian’s 2024 output went to Amazon, providing steady, large-scale demand that cushions the volatility of consumer EV sales. Neither Tesla nor Lucid has this kind of recurring fleet anchor, which gives Rivian a unique edge in balancing growth with stability, especially in its early growth stages.

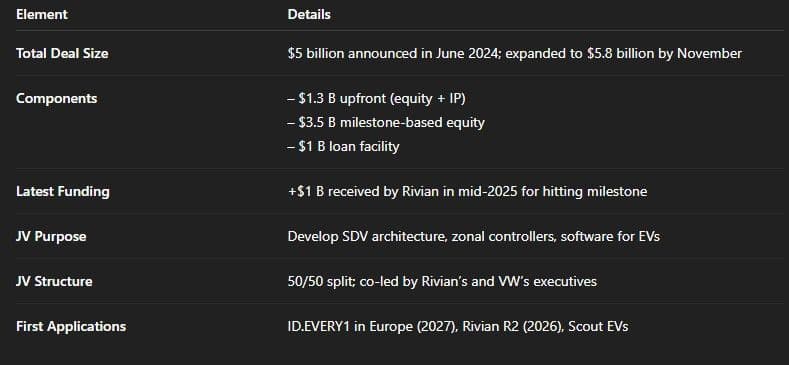

Rivian also benefits from a deep-pocketed strategic partner: Volkswagen. In mid-2024, the two companies formed a 50/50 joint venture to co-develop next-generation software-defined vehicle (SDV) platforms, including Rivian’s zonal electrical architecture and advanced software stack. The deal was originally announced at $5 billion but was quickly expanded to $5.8 billion by November.

The structure is straightforward. Rivian has already received about $3.3 billion, an initial $1 billion convertible note, $1.3 billion tied to equity and IP licensing, and a $1 billion milestone payment in mid-2025 after achieving positive gross profit. Another $2.5 billion remains outstanding, split between a $1 billion testing milestone due in 2026, a $460 million start-of-production milestone expected by 2028, and a $1 billion loan facility Rivian can draw on starting in 2026.

For Rivian, the benefits are twofold: critical capital at a time when scaling production is cash-intensive, and external validation that its electrical/software architecture has real value in the broader industry. For Volkswagen, the partnership accelerates its EV software roadmap and helps spread development costs across a partner that has already proven technical strength. The first real-world applications of this joint venture are expected in VW’s ID.EVERY1 in Europe (2027) and Scout EVs shortly after.

Rivian’s partnerships with Amazon and Volkswagen are impressive, but they’re not the core of the bull thesis. They provide stability and credibility, yes, but the real story lies in Rivian’s consumer lineup. Fleet and commercial sales are icing on the cake, giving Rivian exposure to a market Tesla and Lucid can’t touch directly, but the heart of this investment case is how well Rivian executes on its private vehicle strategy.

Financially, Rivian is still in the “prove it” stage. The company ended Q2 2025 with about $7.8 billion in cash and equivalents, down from more than $9 billion a year earlier. With cash burn running at over $1 billion per quarter, Rivian has roughly seven to eight quarters of runway left, less than two years, before additional capital would likely be needed if operations don’t materially improve. The Volkswagen joint venture, worth up to $5.8 billion with about $2.5 billion still pending, is a critical cushion that buys time. But investors know Rivian can’t rely on partner funding forever; the company must prove it can stand on its own.

That proof starts with its consumer vehicles. The journey began with the R1T, Rivian’s flagship pickup, which rolled off the line in September 2021. It wasn’t just Rivian’s first consumer vehicle; it was the first electric pickup ever delivered in the U.S., beating Ford’s F-150 Lightning, Chevy’s Silverado EV, and even Tesla’s Cybertruck to market. Unlike traditional work trucks, the R1T was designed as a luxury adventure vehicle, a “sports pickup” that blended real capability with premium design. Soon after, Rivian followed up with the R1S, a full-sized SUV built on the same platform, further cementing its brand as the premium EV choice for outdoor lifestyles.

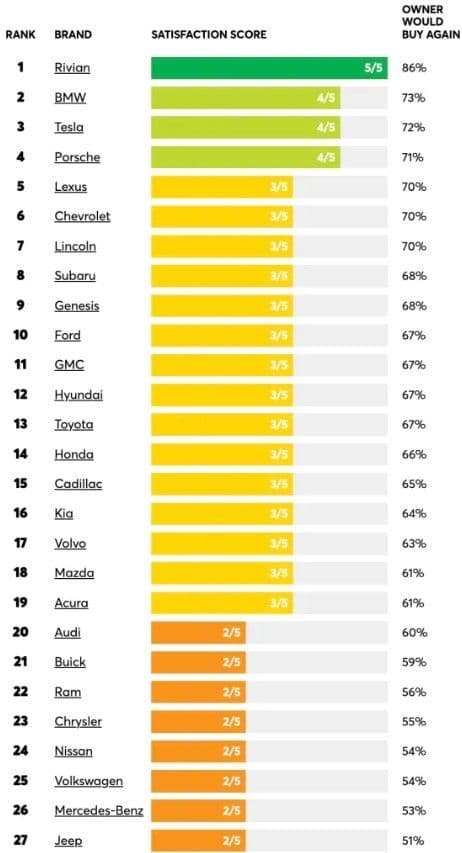

Where this company truly wins is in their brand awareness and high likability. In the electric vehicle space, the company has a highly ranked pickup truck and some of the best brand satisfaction, ranked by Consumer Reports.

🚀 Join the Radar Community

Get free access to MacroBase and notifications about new posts and updates.

On a personal note, having owned Teslas, other luxurious vehicles, and having driven one of these cars firsthand before (I currently do not own one), I can tell you they design some of the most beautiful and aesthetically appealing interiors out there for the price point.

The R1T and S established Rivian’s credibility and brand strength. But as we’ll get into, they’re only the first chapter. The company’s long-term future depends on whether it can take what it learned from the R1 lineup and scale it into a broader, higher-volume product strategy. Strong satisfaction scores and being first to market are great, but they’re not enough to form the bull thesis. The major journey for Rivian is still ahead, and it’s the one that will define the company’s future. As RJ Scaringe himself has said, this “has to work, there are no other options.”

The major journey? Production of their mass market model, R2. To put it in context: the R1T and R1S are Rivian’s premium products, much like Tesla’s Model S and Model X. The R2, however, is designed to be Rivian’s equivalent of Tesla’s Model 3/Y, a lower-priced, high-volume crossover that can reach the broad middle of the market. The R2 is priced at $45,000 and is forecasted to immediately be gross margin positive for the company, which should slow cash burn considerably.

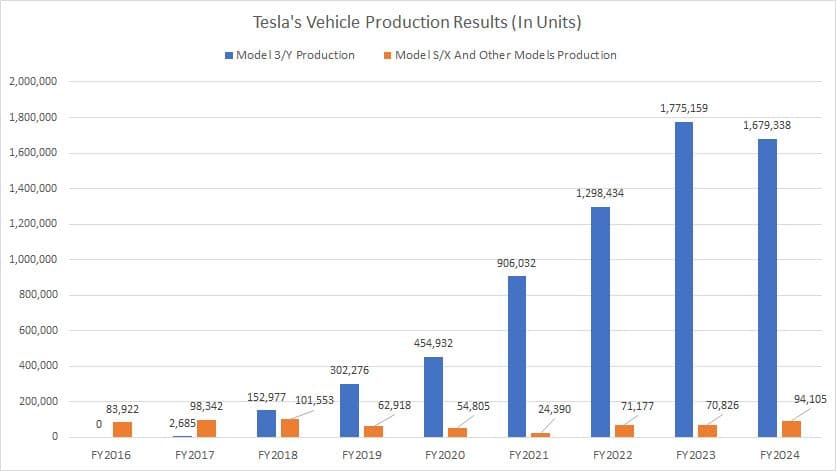

Go back to the numbers we mentioned earlier: in 2024, Rivian sold about 49,000 vehicles, while Tesla sold 1.77 million. At first glance, that gap seems insurmountable. But here’s the catch: roughly 95% of Tesla’s sales come from the Model 3 and Model Y. Strip those out, and Tesla’s production scale before the mass-market push looks much closer to where Rivian is today. In other words, Rivian doesn’t look so far behind when you realize what a single mass-market launch can do.

This is why the R2 launch is everything. Production is scheduled to begin in the first half of 2026 at Rivian’s Normal, Illinois plant, which has been retooled to support up to 155,000 R2 units annually within a broader 215,000-vehicle capacity when including R1s and vans. Industry analysts and Rivian’s own guidance suggest that in its first year, the company could deliver 40,000–60,000 R2s in 2026, depending on how quickly the ramp progresses. If Rivian nails that trajectory, the company enters a new phase of growth and investor perception shifts dramatically. But if the launch stumbles, the downside is severe, as Rivian will have burned precious cash runway without proving it can scale to mass-market volumes.

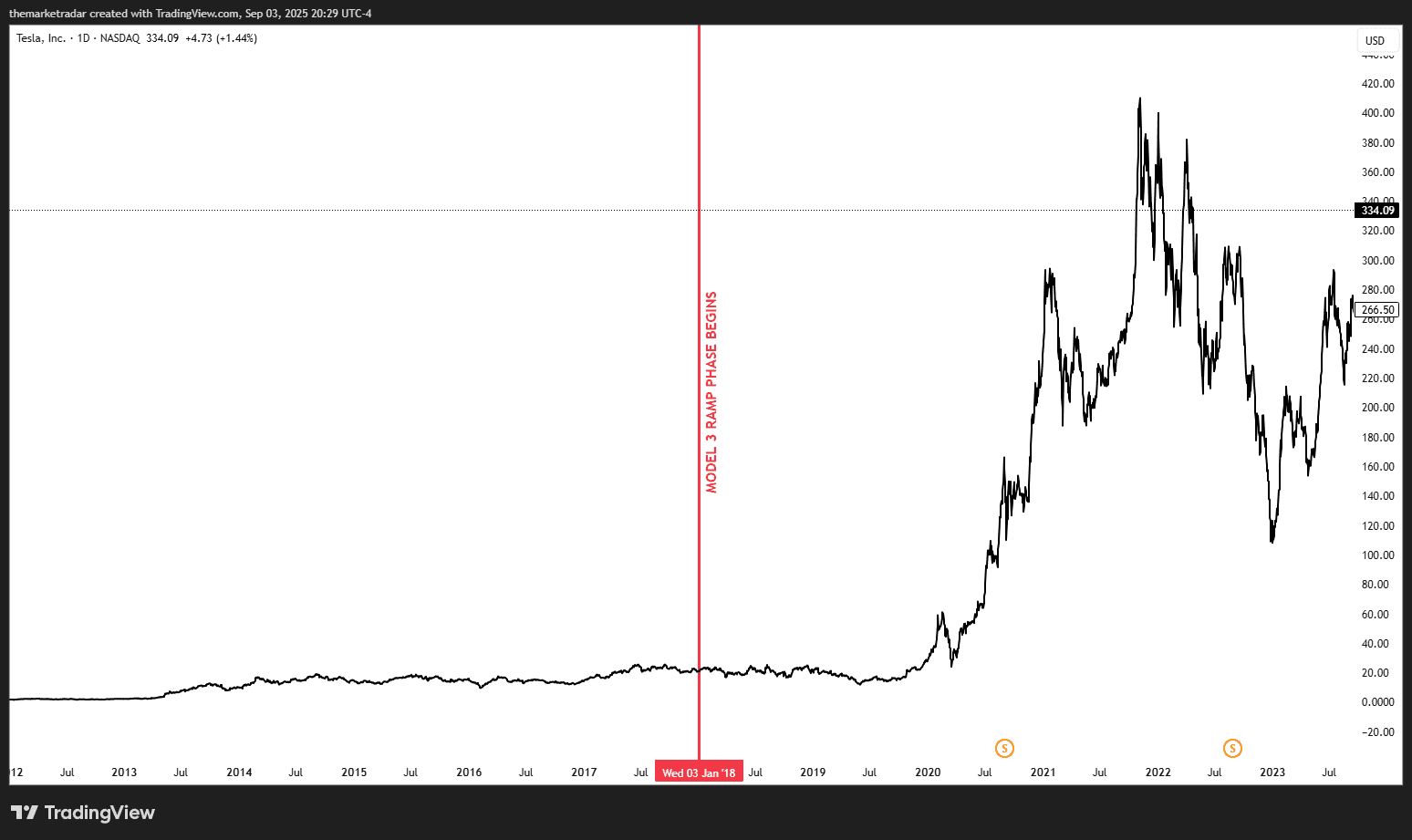

For more perspective, we can look back at Tesla in 2017–2018, just before the Model 3 scaled. At that point, Wall Street valued Tesla at about 3x sales, both trailing and forward. Rivian today is valued at just under 3x sales as it heads into the R2 ramp. In other words, the market is valuing Rivian in almost the exact same way it once valued Tesla, right before Tesla’s business was transformed by the Model 3/Y. If Rivian can pull off the R2 ramp, revenue will rise, and the multiple the company is valued at will too.

The key difference is that Tesla had been selling higher-end vehicles for nearly a decade before introducing the Model 3/Y, while Rivian is approaching its mass-market equivalent with fewer than five years of production under its belt. This is where Rivian needs to execute; the R2 production ramp is critical to the future of the business.

Currently, Rivian’s Normal, Illinois, plant can produce up to about 155,000 R2 vehicles annually within a broader 215,000-unit capacity that also includes R1 models and vans, meaning the company will be effectively capped near 200,000 total vehicles per year until 2028. To break through that ceiling, Rivian has secured a $6.6 billion Department of Energy loan to build its new Georgia plant, which is scheduled to start vehicle production in late 2028 and will eventually add up to 400,000 vehicles of annual capacity, dedicated primarily to the R2 and R3 (R2 is their future line that was revealed but not prioritized for current production roadmaps).

For context, when Tesla launched the Model 3, its production levels were similar to Rivian’s current R2 capacity of about 155,000 units annually, suggesting Rivian should have ample near-term capacity to scale and build enough volume to successfully get the R2 off the ground.

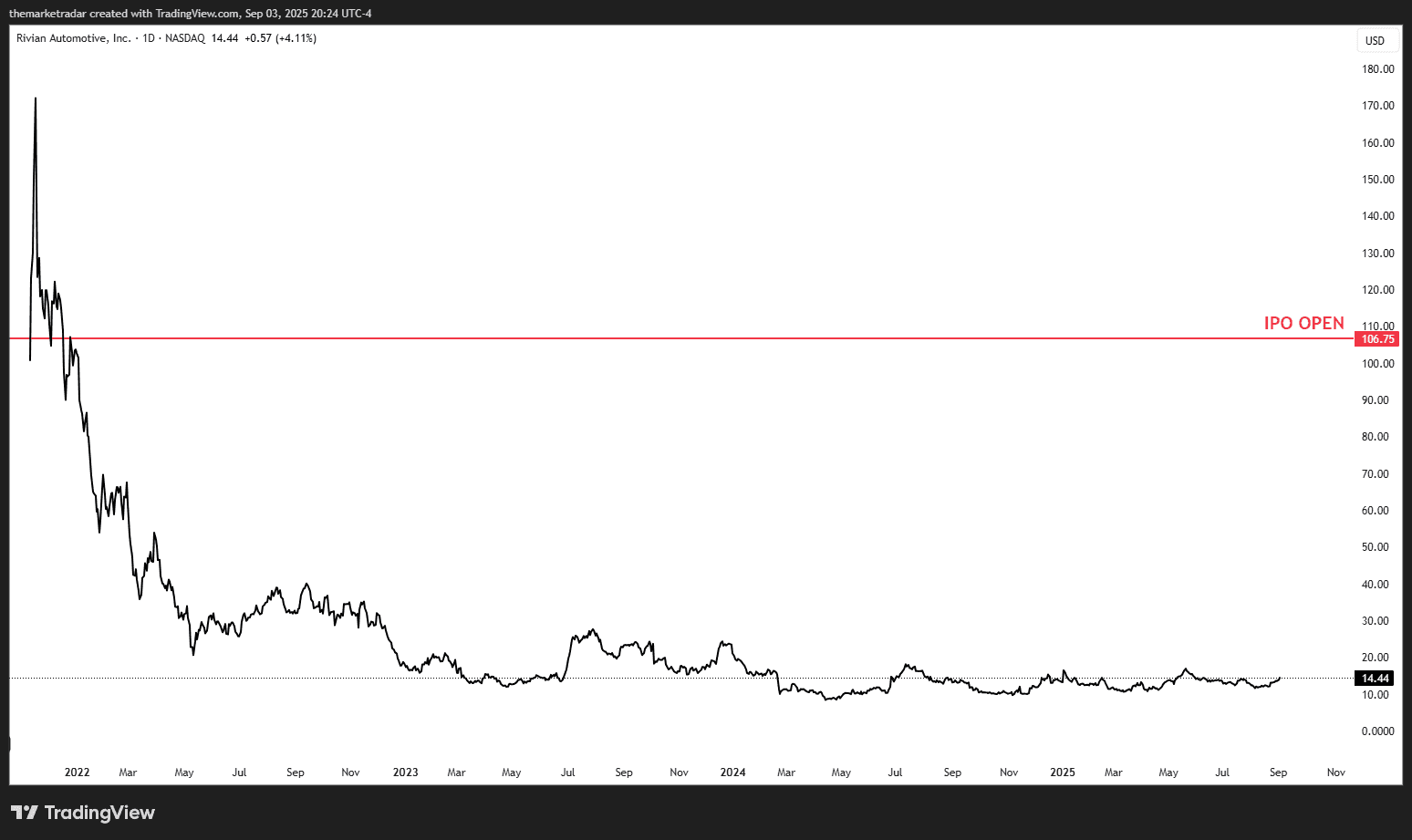

Let’s wrap this together into what we’ll call the bull thesis for Rivian. The company is still in its early stages as an automaker: it has proven it can engineer award-winning vehicles (the R1T and R1S), but it has yet to launch its true mass-market product, the R2, scheduled to start production in the first half of 2026 at its Illinois plant. Since its IPO in November 2021, Rivian’s stock has dropped more than 90% from its peak, a collapse driven less by company fundamentals and more by the broader unwinding of the EV bubble. Add in weakened EV appetite under the current administration, the loss of regulatory credit tailwinds, and sour sentiment across the sector, and it’s clear Rivian is operating in one of the most hated corners of the market. Yet that’s precisely what makes it compelling: unlike many peers, Rivian actually builds great products and has a clear path to scale.

The R2 is the catalyst. Priced around $45,000, it enters the heart of the U.S. crossover/SUV market, a segment that represents more than half of all U.S. vehicle sales. If Rivian executes the ramp, it has the potential to transform investor perception much like Tesla did when it scaled the Model 3 and Model Y. This is Rivian’s shot to move from niche to mainstream.

In other words, Rivian’s stock today reflects skepticism and execution risk, not optimism. The upside is simple: if the R2 proves Rivian can scale, it unlocks lasting gross margin gains and forces Wall Street to rethink how the company is valued. At that point, today’s beaten-down share price stops looking like “fair value” and starts looking like the ground floor, the launchpad before Rivian’s next big run. If they pull it off, we’ll look back and wonder how obvious the opportunity was. This is one of those names that, if it can get out of the dumps and trade to $30, it could easily trade to $50 and beyond. This is Rivian’s ultimate challenge. It’s zero or hero, and I’m long in the $13s.

Good luck.