The Compound Landing - 08.20.23

THE SETUP A little over a year ago, many folks were pretty convinced that we were headed for a recession. The signs were there, like two back-to-back quarters of negative GDP growth. The Macro Monkeys were caught up and positioned for the idea that a recession

THE SETUP

A little over a year ago, many folks were pretty convinced that we were headed for a recession. The signs were there, like two back-to-back quarters of negative GDP growth. The Macro Monkeys were caught up and positioned for the idea that a recession was around the corner in the past year or so. Their reasoning was mostly tied to the belief that the economy, which was already not in great shape, would take a hit from the aggressive interest rate hikes that were happening.

But here's the twist: those recession predictions didn't pan out as expected. Bonds went down by 16%, and stocks are actually up around 4% over the past year. Luckily, the tools we use at Market Radar are pretty sharp and helped us steer clear of these risky recession-related plays when things were uncertain. Now, it seems like more and more people are jumping on the "soft landing" bandwagon, and that's where things get interesting.

Towards the end of last year, as the stock market started to bounce back from its lows, people started talking a lot about the idea of a soft landing. So, what's that all about? Well, it's kind of an alternative to the classic recession scenario. When we usually hear about a "real" recession, it's usually a "hard landing." But a soft landing is more like a controlled slowdown. The economy eases down a bit, and inflation gets under control, but it's not such a big slowdown that it messes up jobs and growth in a major way.

The whole soft landing versus hard landing debate has been quite a talking point in the past year. You've got the pessimistic folks, often called the "bears," who are pretty convinced that a rough landing is coming. On the other hand, you've got the more hopeful crowd, the "bulls," who are rooting for a smoother landing.

At Market Radar, we're not just going with the flow of the latest economic trends. Back in early 2023, we spotted a potential soft landing on the horizon, and we've stuck with that hunch all year. We came up with a saying in the first few months of 2023 that goes something like this:

“The impossible soft landing will continue until all faith in the hard landing is lost”.

Now, that might seem a bit puzzling at first glance. It's not saying that the soft landing keeps going even when folks are worried about a hard landing. Instead, it means the soft landing will happen in a way that makes people believe the toughest part of a recession is actually this soft landing phase. Those who believe in a hard landing will fight this, ultimately throwing the towel in after either blowing their books up or the hard landing taking too long to seem probable. And that's when the cycle will shift, leading to a hard landing, catching most people off guard.

I know this can all sound a bit confusing, especially with all the chatter in the media about soft, hard, or no landings at all. But think about it—your investments aren't just about what happens in the next few months, right? We need to consider where we are in the larger economic cycle. And that's where the Compound Landing comes in.

The Compound Landing isn't just picking one of those scenarios we talked about earlier. It's a blend of all of them. It's the idea that we move from a bit of an economic slowdown (soft landing) to a time with no major economic slump (no landing), and then to a point where nobody's really worried anymore (hard landing). Surprisingly, that soft landing phase is what sets the stage for the eventual hard landing. Our understanding of this economic puzzle is based on the tools we use, and we're open to tweaking it as our tools give us more insights.

THE STAGES

#1 Lags

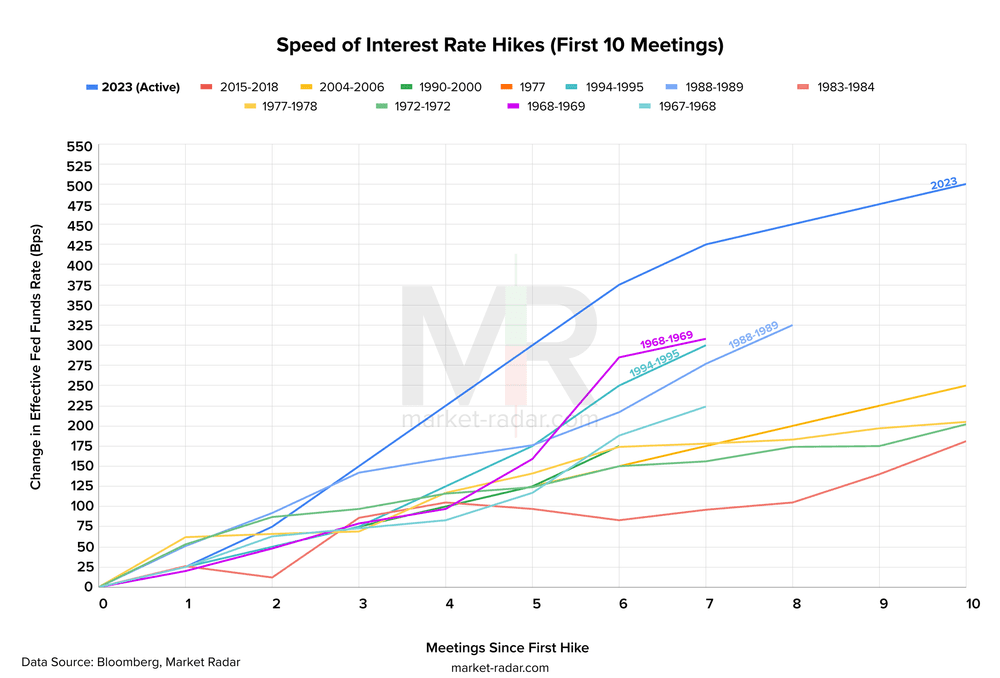

What makes the Compound Landing really stand out is the journey that's brought us to where we are now. Picture this: in just three years, we've gone from a time of massive financial support and quantitative easing (QE) to a record-breaking cycle of raising interest rates and tightening up on the money supply (QT). The combined impact of all these changes has created some serious time delays in how things are playing out. I've covered these delay details and how extreme they are in a previous post, which you can find HERE.

In a nutshell, we're smack in the middle of the most extraordinary interest rate hike spree we've ever seen, and that's causing some really extraordinary lags in the process.

Now, those gaps are going to open up some windows of opportunity where it might make sense to take on more risk as we move through different phases on our way to completing this compound landing journey. When we're in the softer or no-recession stages, it could mean good things for the stock market as worries about big economic slumps start to fade away. As we approach the last phase, the hard landing, folks will likely have thrown the towel in on a recession, which will all add to the complexity of how it unfolds.

#2 Policy (where we are today)

It's all about considering the early phases like soft and no landings, which have some implications for rate cuts. We're looking at whether it's a good move to put those rate cuts on the back burner for now. Here's why:

🚀 Join the Radar Community

Get free access to MacroBase and notifications about new posts and updates.

Imagine we're not facing a full-blown recession, but rather a situation where growth is slower than usual yet we're still dealing with some inflation. If we were to cut rates right now, it could actually give a boost to the job market, which is already pretty tight, and potentially fuel more economic growth. Just to give you a heads-up, the Atlanta Federal Reserve's GDPNow model suggests we could be looking at a solid 5.8% growth in GDP for the upcoming quarter. This is still early and can obviously change with additional data. So, the general idea that rates will stay relatively high for a good while longer will continue to shape how the market behaves.

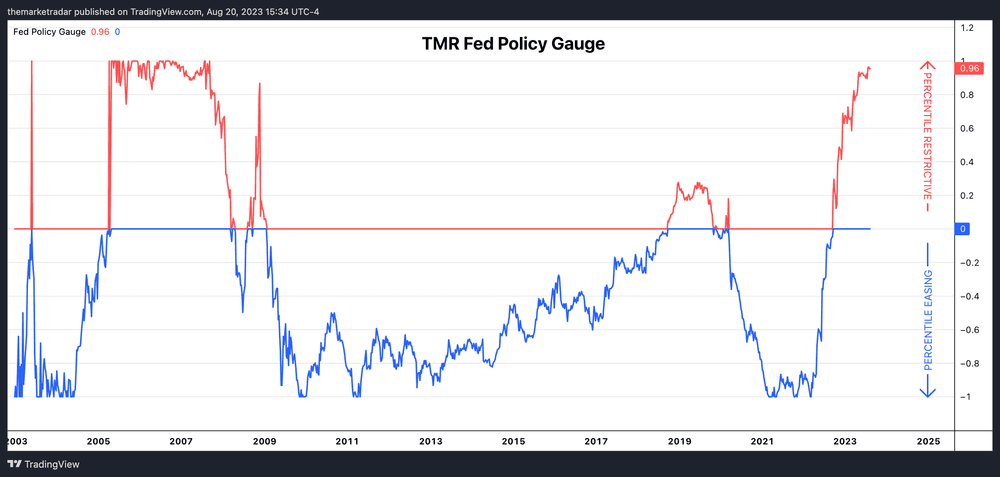

This doesn't mean the Federal Reserve has to crank up rates further. Instead, it's about keeping rates steady where they are for a more extended period. Right now, the Federal Reserve's approach to policy ranks in the top 4% when compared to historical data from 2003. So, the remaining piece of the puzzle involves giving these recent policy moves that inherently have lags attached to them enough time and room to melt and flow through the economy.

#3 Normalization

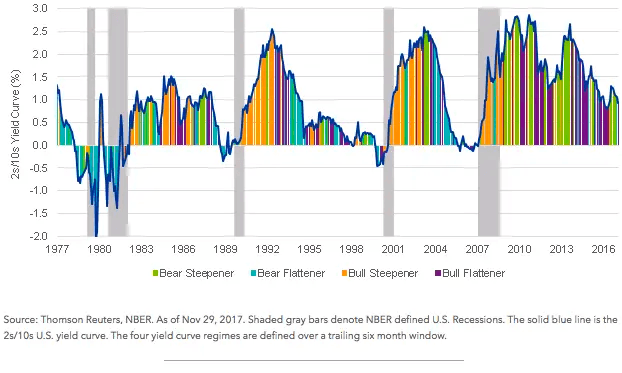

Let's dive into what's been going on with the yield curve and how it connects to the Compound Landing idea. For those that don’t know, the yield curve shows how interest rates are different for short-term and long-term loans. It's kind of like a roadmap for how the economy is doing.

The yield curve sometimes flips upside down, which is called an inversion. This is primarily due to the fact the Fed has more control over short-term interest rates than they do long-term rates. As the Fed raises rates to slow the economy and fight inflation, they’re primarily lifting short the front end of the yield curve. If inflation is excessive, they usually have to lift short-term rates above the market average (long-term rates) and they end up putting the curve into an inverted state. This is where we are today.

Typically, the way the yield curve normalizes or reverts is by what is called a bull steepener. This is the process where the inverted difference between short and long-term yields is resolved by reducing front-end rates below long-end rates. As you can see in the below chart, the bull steepener is illustrated by the orange bars. This steepener usually occurs before/during all recessions and is driven by Fed rate cuts.

Now, picture this: if everyone starts thinking there won't be a recession, then there's not much reason to settle for lower long-term rates or the Fed cutting short-term rates. It's like saying, "Hey, if things are looking good and the Fed doesn’t need to cut rates, there may be a new higher average long-term interest rate." What happens then, is instead of the yield curve reverting through a bull steepener as illustrated above, it reverts in a way that is known as a bear steepener. This is where longer-term rates rise above the current higher short-term rates reverting the curve into a normal state with new higher long-term yields. Again, all this is doing is adding more restrictive pressures to the economy.

Speaking of long-term rates, the Treasury, which handles government finances, plays a role too. If people believe a recession is off the table, the Treasury doesn't have to keep borrowing for the short term, expecting rates to fall lower than long-term rates during a recession. Instead, they'd focus more on longer-term borrowing, where the costs might be better. We've actually seen this trend already – more borrowing for the long haul in recent months. The risk continues here as we’ve seen an acceleration in longer-term borrowing, which pulls duration risk out of the market. Uncertainty remains here on how this will continue in the upcoming borrowing schedules from the Treasury over the next six to twelve months.

There are some additional risks that are hidden, they may not show themselves but we have to take them into consideration. Remember, this Compound Landing thing isn't just happening in the US. Other countries are dealing with their versions of it too. Take Japan, for instance. If things keep going as they are there, they might have to make some serious changes in their policies. And guess what? That could lead to them moving their investments from the US and back home.

So, the point here is that the shift in the long-term yields isn't just about inflation. It's more about this Compound Landing concept, which is basically a sequence of economic phases. These phases are affecting how interest rates move, and it's way more intricate than just inflation accelerating.

#4 The Final Straw

So, let's talk about what happens next in the Compound Landing journey. After going through two out of the three stages, we hit a crucial moment. Now, you might be thinking, "What if we've really found a better way to manage interest rates and we smoothly pull off the soft landing? Can we dial down inflation without messing up the economy's growth?" Well, here's the thing - that idea often forgets about the frozen lags of monetary policy and how they melt and flow through the economy in the future.

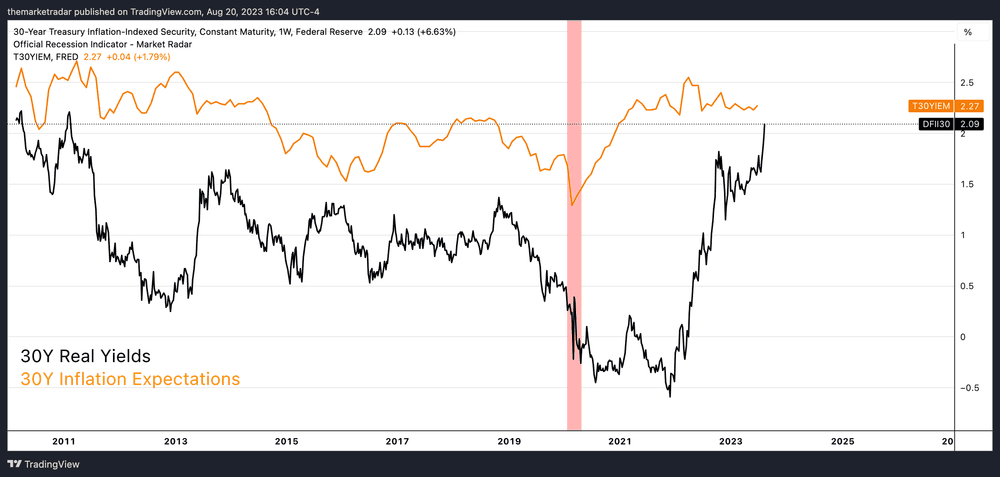

As we travel through the Compound Landing phases, especially the soft and no-landing ones, a sneaky outcome shows up - we unintentionally end up putting more constraints on the economy. Imagine this: the yield on 30-year bonds that factor in inflation keeps climbing, even though the expected inflation itself isn't really changing much. To put it simply, this means the return on investments after accounting for inflation is going up, hinting at higher risk-adjusted return levels. This kind of trend can make sense if we're not expecting a recession anytime soon - which is exactly what the middle part of the Compound Landing scenario assumes.

As the market keeps considering the chance of a soft or no landing, it's likely that the longer-term yields and these real yields will remain pretty strong. But in a regular recession, both of them would usually drop because the economy would be weaker and the Fed would be trying to give it a boost. However, without a recession in sight, the economic grip keeps getting tighter, even if the Fed just pauses on its path of policy. This is when we transition from the middle part of the Compound Landing and start moving toward the hard landing.

Here's the kicker: as we transition, we're not just carrying over the constraints from the previous soft and no-landing stages. We're also dealing with the effects of Fed policies that haven't fully kicked in yet because these delays have been pretty extraordinary.

So, if you believe in a soft landing, you believe in the ability of the Fed to take into account all four stages of the above compound landing in real-time, including their own lags, and then compensate for each of them as they occur. Unfortunately, while I could be wrong, I do not believe the Fed is capable of such tremendous policy execution. Instead, I do believe they will see the first two stages of the compound landing and not realize the third stage exists, or actually price out the possibility of the third stage completely and end up holding policy in too much of a restrictive state for too long.