This Is How Melt-Ups Start

The Fed is about to choose between “measured” and “mistake.” If they become too easy into an economy that’s still running above capacity, we don’t just grind higher. We melt up. Think late 1990s vibes, but with AI-boosted productivity and a central bank traine

The Fed is about to choose between “measured” and “mistake.” If they become too easy into an economy that’s still running above capacity, we don’t just grind higher. We melt up. Think late 1990s vibes, but with AI-boosted productivity and a central bank trained to chase every wobble in labor.

In today’s note, we break down why policy that leans easy into a positive output gap is rocket fuel, why the “neutral premium” is the real tell, and how further dovishness surprise would pour gasoline on small caps, cyclicals, and anything duration-sensitive. If you care about catching the next vertical leg rather than watching it, read on.

Easy policy fuels melt-ups

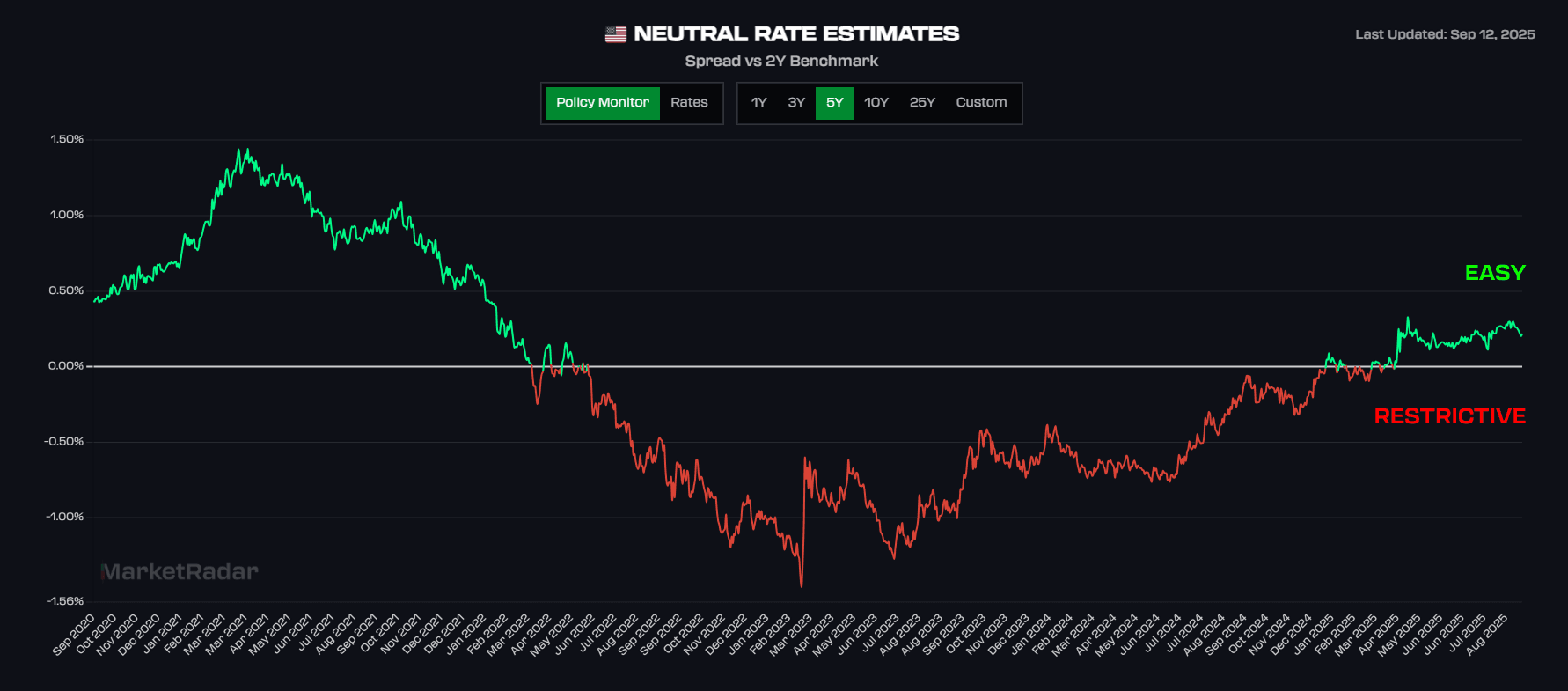

Melt-ups don’t happen when conditions are tight. They happen when the Fed is looser than neutral. Our neutral-premium read shows the Fed is already leaning easy. With the current policy floor hovering around 3% we have entered back into easy territory, we'll be watching this closely, if the Fed comes out as more dovish than expected in their SEP next week the floor will definitely move lower and open the doors to melt-up.

🚀 Join the Radar Community

Get free access to MacroBase and notifications about new posts and updates.

Output matters more than jobs

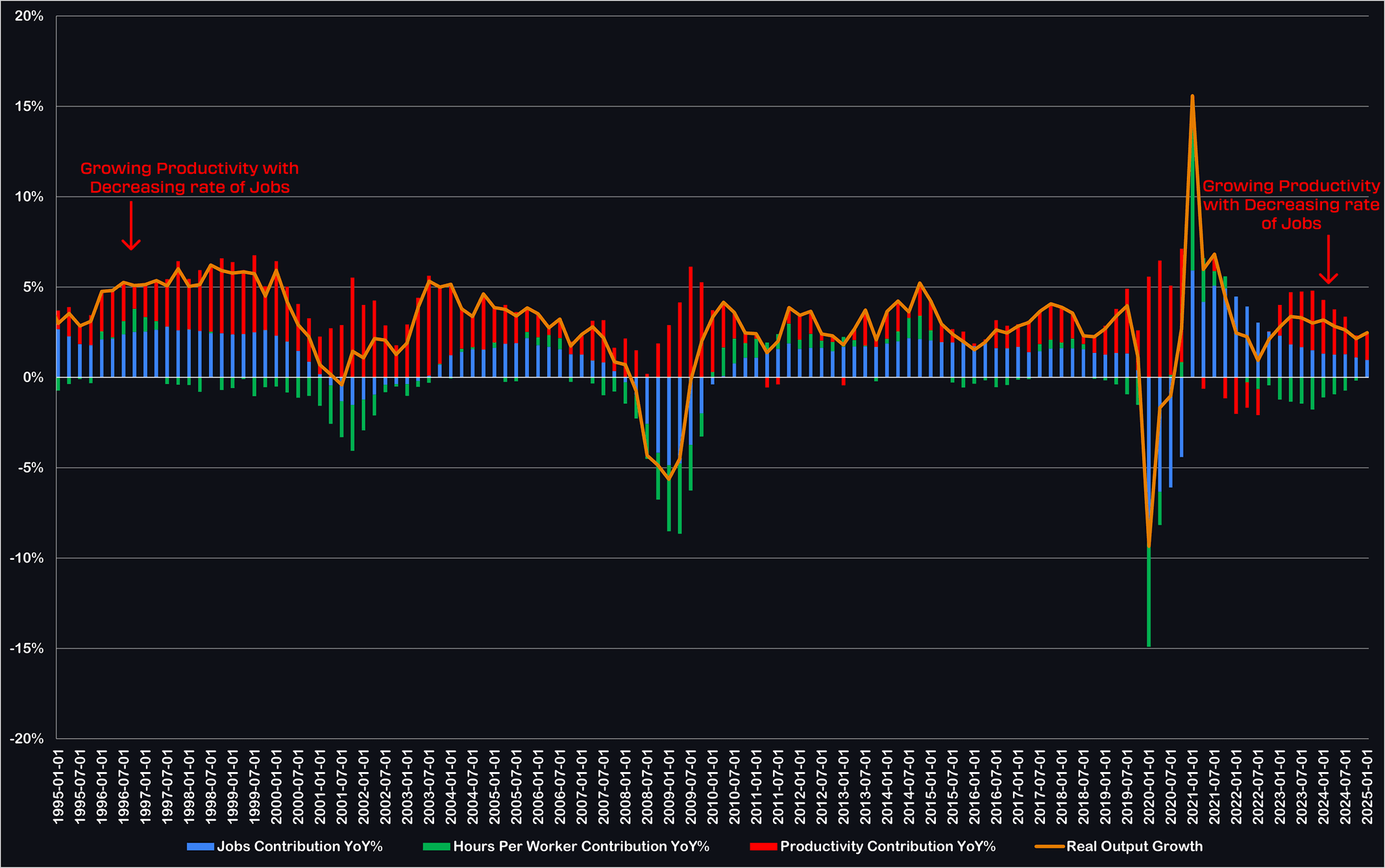

The unemployment rate has drifted from 3.4% to 4.3%, but GDP growth is still running ~2% real. Why? Productivity has stepped up, similar to 1995–1998, when the economy grew despite weaker payroll numbers. Stocks care about earnings and output, not headcount, I highly suggest you read our deep dive on this topic Payrolls Don't Matter Anymore. Since the 2000s growth has been highly dependant on payroll growth to boost GDP, this may be the first time since the 90's that we see a majority of growth produced by productivity increase rather than labor force increase. If the Fed doesn't see this new dynamic, and continue to ease policy at every sign of labor deterioration they will walk into a policy mistake by easing too much.

The Fed’s Blind Spot

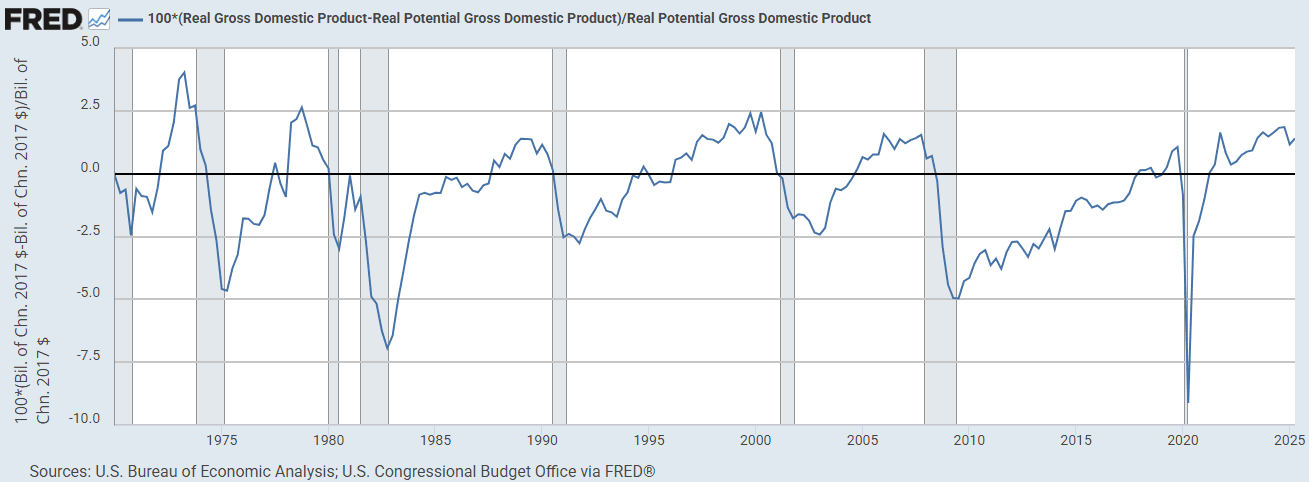

Every current Fed member came in after 2011. They’ve only ever set policy in a world shaped by deflationary fears and weak demand stemming from the 2008 financial crisis. They are trained to react to labor market weakness with stimulus. A clear difference between today and the post GFC economy can be seen through the output gap and inflation rates. After 2008 the output gap remained negative until 2018 while inflation was barely able to stay at 2%, this was fragile deflationary economy that was very sensitive to labor shocks. But today’s economy is above capacity, mainly driven by increase productivity, cutting into that environment risks reigniting growth and inflation too strongly and sending asset prices vertical.

Most traders are staring at payroll revisions. The market is trading the output gap. As long as output remains strong, dovish moves into temporary labor softness could be the match that lights the melt-up.