Payrolls Don't Matter Anymore

The U.S. economy is breaking one of its oldest rules. For decades, growth and payrolls moved in lockstep: more jobs meant more output, and every jobs report offered a near-instant read on the cycle. That pattern is no longer holding. Recent benchmark revisions

The U.S. economy is breaking one of its oldest rules. For decades, growth and payrolls moved in lockstep: more jobs meant more output, and every jobs report offered a near-instant read on the cycle. That pattern is no longer holding. Recent benchmark revisions erased nearly one million jobs from last year’s totals, cutting net payroll gains to just 847,000 between March 2024 and March 2025. Payroll growth is now running at only 0.53 percent, far weaker (half) than first reported. Yet during the same period, real GDP grew steadily by 2 to 3 percent. The economy kept expanding even as hiring slowed, a clear signal that labor alone is no longer powering the recovery.

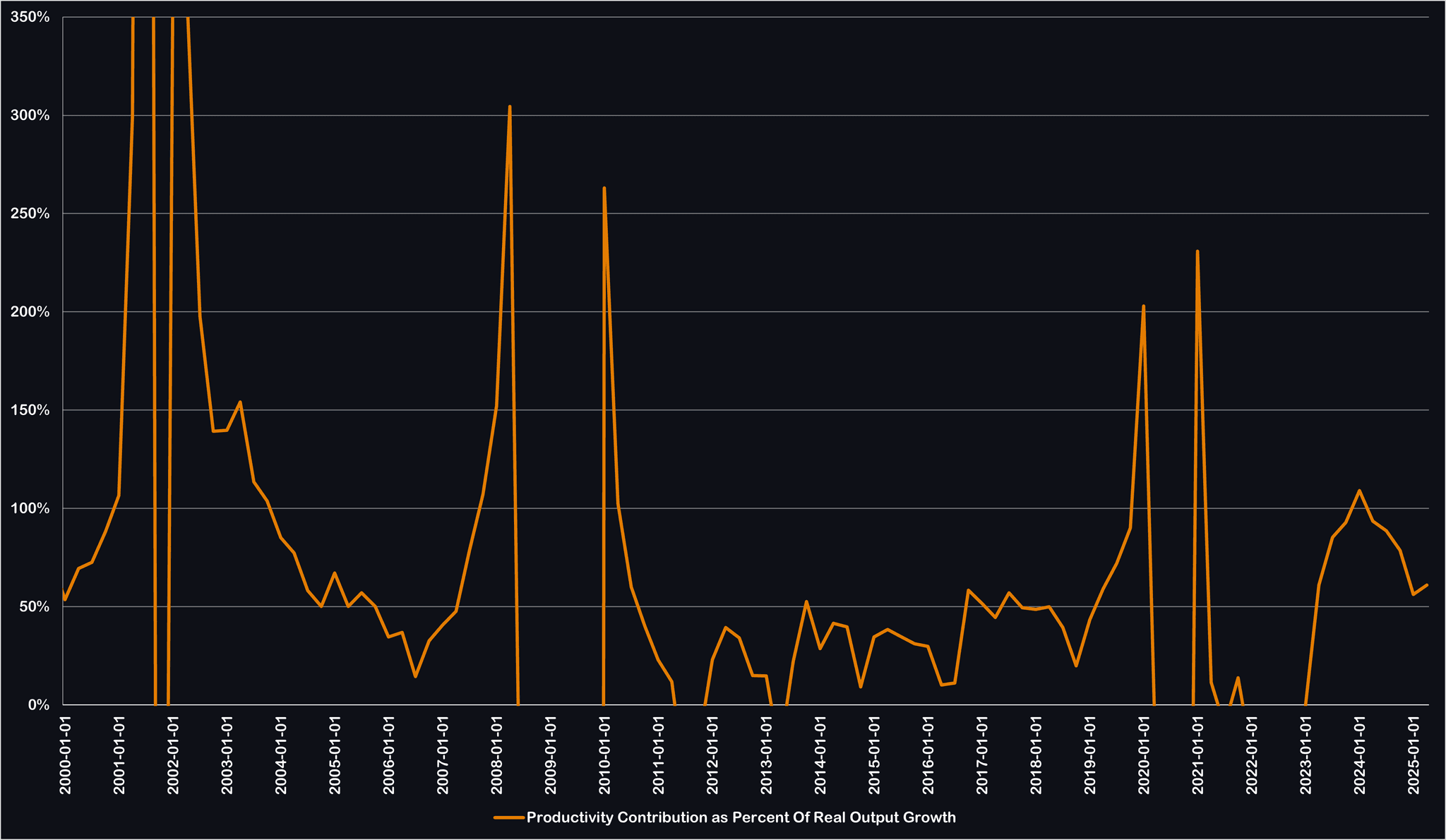

The gap is being filled by productivity, which is now at steady figures that we haven't seen since the Dot-Com bubble in the early 2000s. But productivity alone is not the whole story. Hours worked, labor force flows, immigration policy, and technology adoption are all reshaping the economy’s growth engine. The result is an environment where payrolls grow more slowly than the labor force, unemployment pressures can rise even as real output strengthens, and productivity gains deliver a buffer against inflation.

This ledger explores that shift in full: the weak payroll trend uncovered by revisions, the balance of contributions from jobs, hours, and efficiency, and the structural dynamics bending old labor reaction functions. From AI adoption to tighter immigration under the Trump administration, the composition of growth is changing in ways that will define both macro policy and market outcomes in the years ahead.

The AI Revolution

AI has become one of the most debated themes in markets. Every cycle raises the same questions: will the surge in corporate spending on AI deliver measurable returns, or is it another hype cycle? No one can fully map the economic effects of AI yet, but the timing of its rise is striking. The launch of ChatGPT in late 2022 coincided with a critical moment in the business cycle. Widespread access to generative AI tools appears to have helped the U.S. sidestep a recession and pushed productivity onto a higher trajectory.

The benchmark payroll revisions make this even clearer. By stripping out nearly one million jobs from the past year, the revisions revealed that job growth was far weaker than first reported, with payroll gains cut roughly in half over the March 2024 to March 2025 period. That matters because these revisions come from the Quarterly Census of Employment and Wages (QCEW), which is only incorporated into the official payroll series each February. Until then, the payroll data are overstated, and by extension, the job contribution to real output growth is overstated as well. This means that productivity’s role is already larger than the headline figures imply, and once the QCEW revisions are baked into the payroll level series early next year, the official numbers will likely show even stronger productivity contributions to growth.

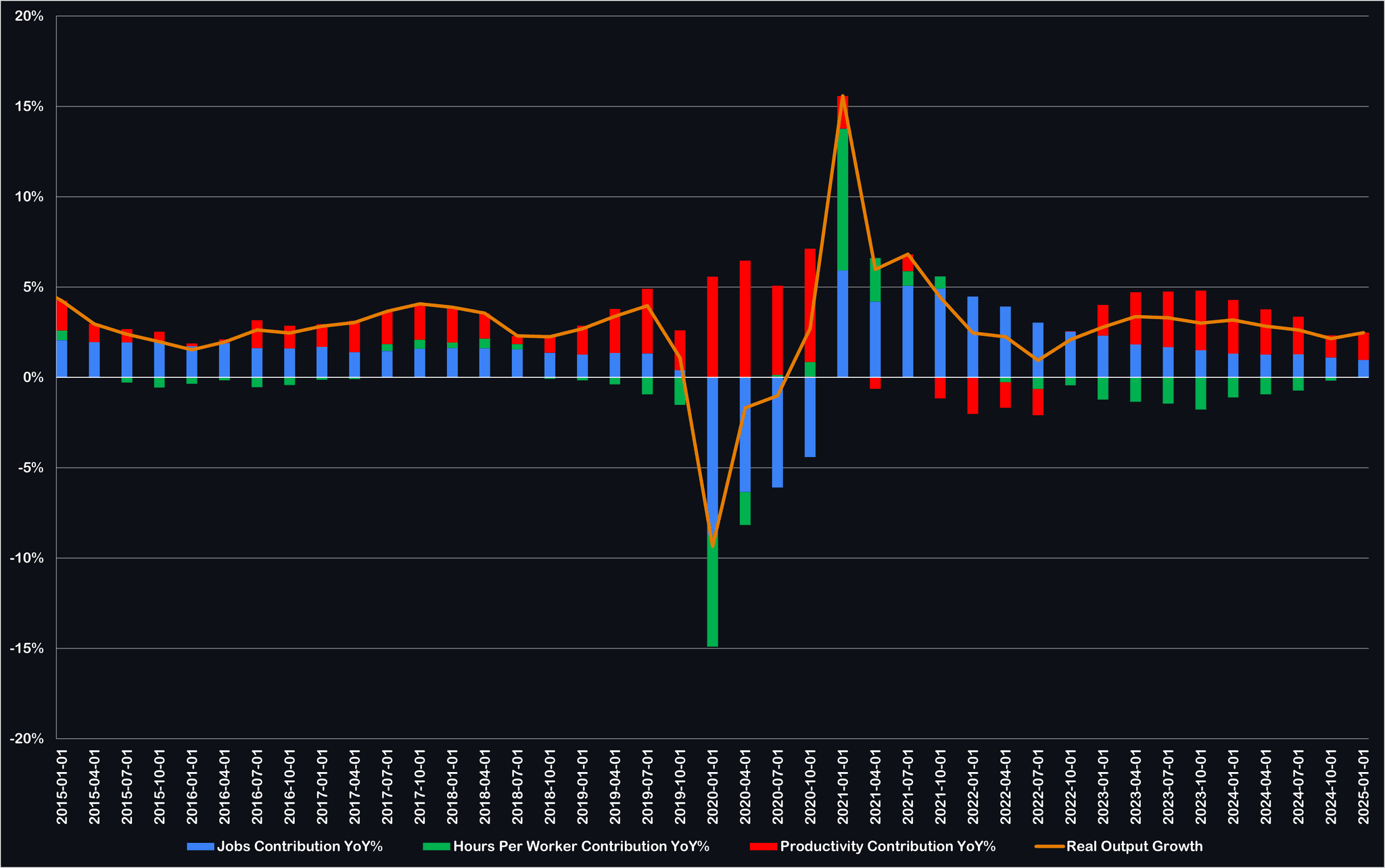

The growth accounting framework highlights the point:

Change in Real Output Growth = Change in Jobs + Change in Hours Worked + Change in Productivity

Since late 2022, jobs and hours have added less to output, while productivity has carried more of the burden. Charts from FRED show productivity growth now tracking more closely with overall real output than in the prior decade. Remember, these productivity contributions are going to be revised even higher from here as payroll revisions take effect to the payroll series early next year.

Immigration and Labor Force Dynamics

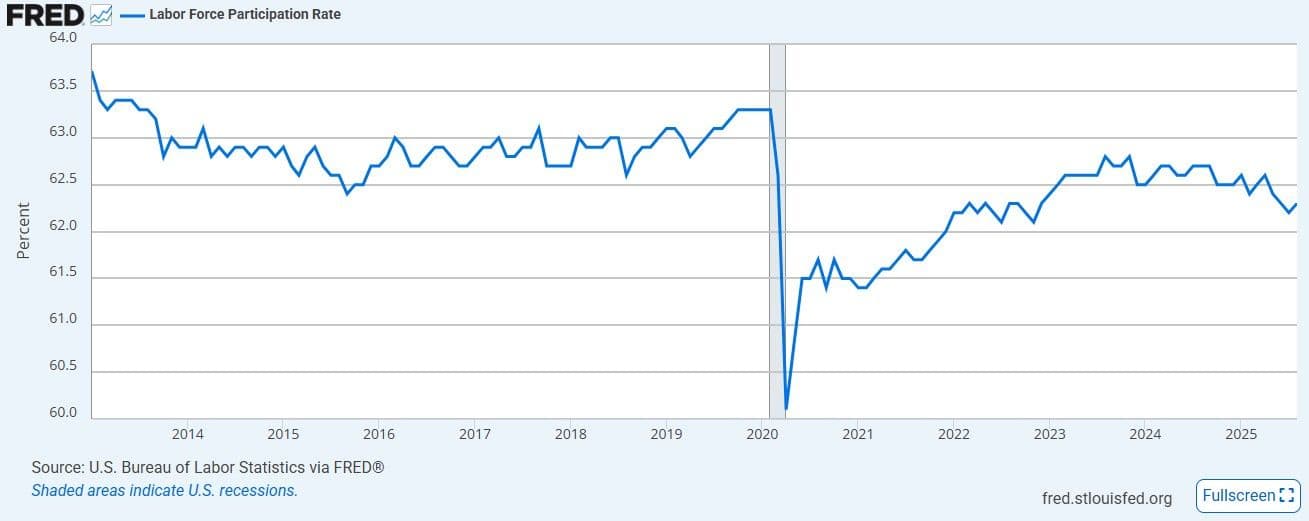

Immigration is another piece of the growth puzzle. It has a direct impact on labor force participation, which in turn shapes how we interpret payrolls and unemployment. The chart below shows that participation has eroded steadily through 2025, falling to multi-year lows. One explanation is weaker immigration flows, which reduce the inflow of prime-age workers and shrink the participation base at precisely the moment the economy needs additional labor supply.

This matters because immigration is not just about headcount; it determines how much capacity the economy can sustain. With fewer workers entering, the supply side tightens, wage pressures accelerate, and potential output is revised lower. That makes the measured output gap appear wider than it really is, exaggerating the sense of overheating when fiscal deficits are already large. Stronger immigration works in the opposite direction: it raises participation, expands capacity, and blunts the inflationary impulse from government spending.

In short, immigration functions much like AI in one critical sense: it changes the supply side of the economy. When inflows are strong, unemployment can drift higher temporarily as new workers are absorbed, but overall capacity rises and inflation pressures ease. When inflows weaken, participation falls, capacity growth stalls, and inflation risks rise. This is why today’s multi-year lows in participation matter: they reveal how immigration shocks can amplify supply constraints, distort the output gap, and complicate the policy reaction function.

Output Gap and Deficit Effects

🚀 Join the Radar Community

Get free access to MacroBase and notifications about new posts and updates.

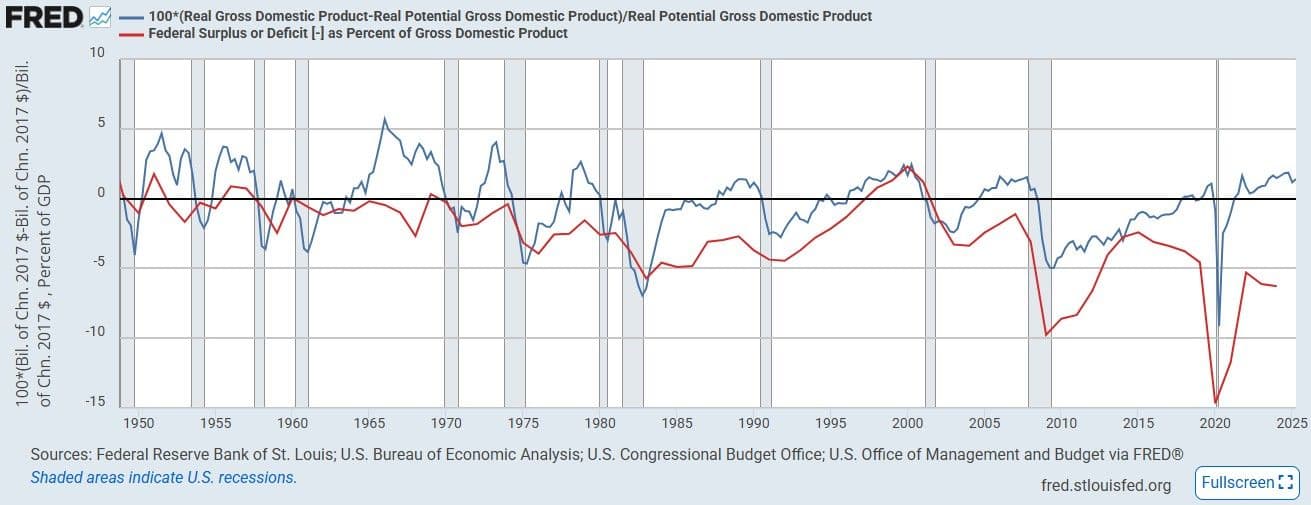

This raises an important question: are we overstating the output gap? Standard models say a 6 percent fiscal deficit added to an economy at maximum capacity should spark accelerating inflation. Yet inflation has not surged, partly because the Fed has been restrictive enough, and partly because capacity may not be as constrained as models assume.

The data show a striking divergence. After the pandemic, deficits reached record peacetime levels while the measured output gap turned positive. By conventional logic, that combination should have driven a sharper inflation surge than what actually occurred. The explanation lies in the supply side. If capacity is understated, then the “true” output gap is smaller than reported. AI adoption expands capacity quickly in a service-driven economy, while immigration restrictions shrink it. These opposing forces explain why deficits and positive output gaps have coincided with only moderate inflation.

The conclusion is that the economy may not be as overheated as headline figures suggest. Instead, it may be closer to balance: deficits are still stimulating, the Fed is restrictive enough to offset demand, and AI-driven productivity gains are offsetting immigration-driven supply constraints. The result is sticky but not runaway inflation.

Unemployment Dynamics

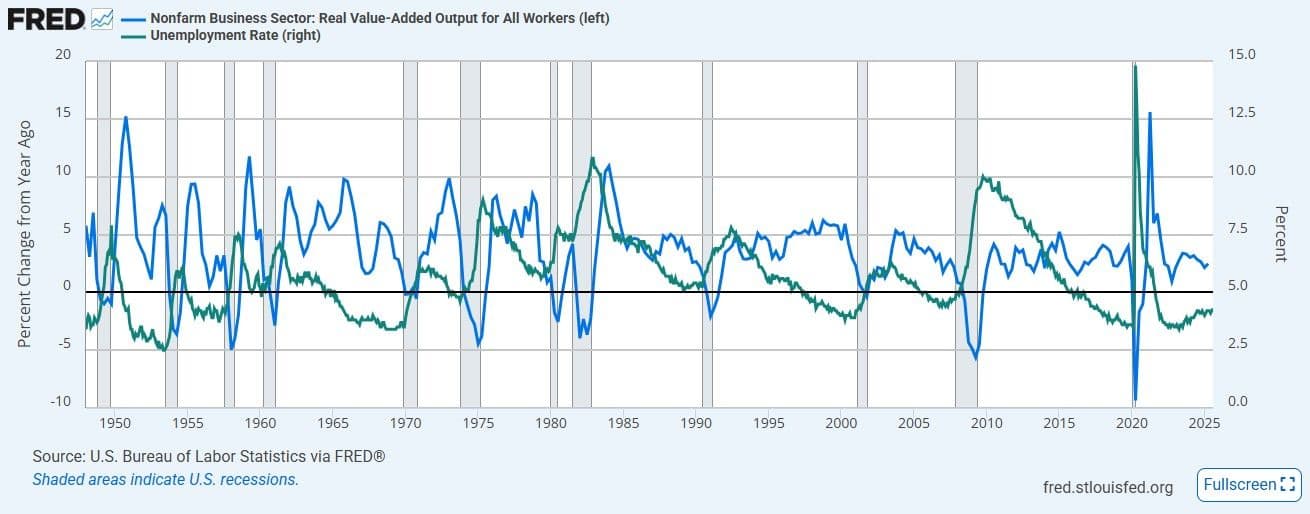

The chart comparing real output growth (blue) with the unemployment rate (green) highlights the traditional output–unemployment relationship. Historically, the pattern has been consistent: when output growth is strong and accelerating, unemployment falls or remains suppressed. When unemployment rises, it almost always coincides with a slowdown in output. That correlation has long guided how markets interpret labor market signals.

For now, the relationship still appears intact, with unemployment broadly flat even as output growth holds up. The Fed’s latest Summary of Economic Projections reflects this nuance. Policymakers see unemployment drifting higher over the forecast horizon, yet in their latest FOMC meeting, they judged unemployment risks as balanced against inflation. In other words, unemployment has not risen to levels that the Fed views as destabilizing. The labor market remains historically tight, and there is a broad perception that unemployment can climb modestly from here without signaling recessionary stress.

For companies, this dynamic looks very different than a traditional labor-driven cycle. Normally, expectations of higher unemployment signal weaker demand, softer sales, and margin pressure. But in the current regime, unemployment can rise while corporate earnings remain intact because the growth is being driven less by headcount and more by efficiency. Productivity gains mean firms generate more output per worker, while new business formation provides an outlet for displaced labor, cushioning the demand side. In effect, unemployment becomes less of a signal about collapsing growth and more of a byproduct of structural reallocation. This is an environment where unemployment can prove tricky as sporadic moves can appear as supply surpluses emerge and get reabsorbed rather quickly, neutralizing momentum in unemployment indicators.

Markets appear to be pricing this distinction correctly. A modest uptick in the unemployment rate alongside strong real output growth and rising productivity is not the same as a recessionary surge. It implies that the labor market is evolving, automation and AI adoption are allowing margins to improve even as payroll growth slows. That’s why equities can remain resilient despite the drift higher in unemployment: the driver isn’t contraction, it’s transformation.

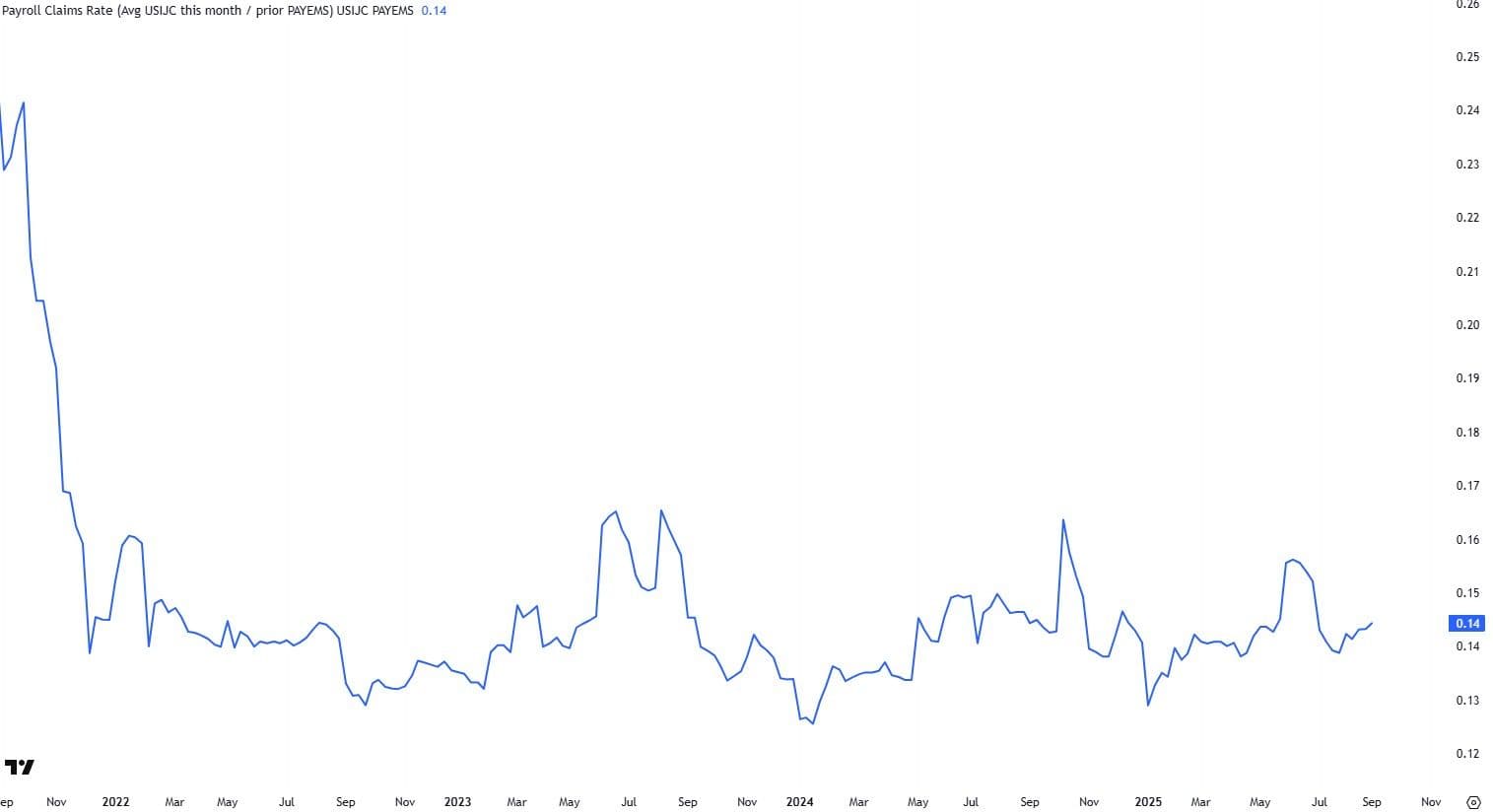

Another area of resilience is the claims rate, which measures new unemployment claims relative to the size of the labor force. The claims rate has held in a tight range, showing little sign of the stress that would normally be breaking out amidst a sharp rise in unemployment. We explained the claims rate in greater depth in a prior note here, but the conclusion is the same today: labor market conditions are not as weak beneath the surface as broader unemployment headlines might suggest.

The Fed's Dilemma

The U.S. economy is evolving into a structure where output growth is less tied to payroll expansion and more dependent on productivity. AI adoption plays a central role here. Its integration is steady, not explosive, but firms are generating more output with fewer workers, margins are improving, and displaced labor is often reabsorbed into new business formation and emerging industries. This explains why unemployment can drift higher without signaling collapsing demand.

Immigration adds a second, opposing force. Restrictive inflows shrink labor force participation, reducing the supply of available workers just as AI boosts efficiency. Together, these forces create labor market signals that look contradictory: unemployment can rise because immigration cuts tighten participation, while output continues to expand because AI allows firms to do more with less. The traditional link between payrolls, unemployment, and growth has become much harder to interpret.

For the Fed, the danger is misreading these signals and overreacting to short-term labor spurts. A modest rise in unemployment might prompt policymakers to ease prematurely, even if the increase reflects supply frictions or AI-driven reallocation rather than weak demand. Such easing can inadvertently feed back into conditions that are too loose, keeping inflation elevated as the economy continues to work through the combined effects of immigration constraints and productivity gains.

The balance is delicate. AI and productivity improvements have given the economy breathing room, supporting output growth and containing inflation. But immigration restrictions reduce labor supply, tightening capacity. If fiscal deficits remain large and policy reacts too quickly to noisy labor data, the result could be inflation that proves stubborn rather than contained. The lesson is that this new phase of growth requires a different reaction function: one that accounts for productivity-driven resilience, immigration-driven supply constraints, and the risk of policy overcompensation in the face of confusing labor dynamics and innovating technologies.