6 MIN READ·NOVEMBER 15, 2025

When Tailwinds Disappear and the Headwinds Start to Bite

The Macro Update Markets have entered a stretch where every bounce feels fragile and every headline seems to hit harder than the last. Investors keep searching for signs that conditions are turning, yet our System has been flashing the same warning for weeks.

MR

CONTRIBUTOR · MARKET RADAR

The Macro Update

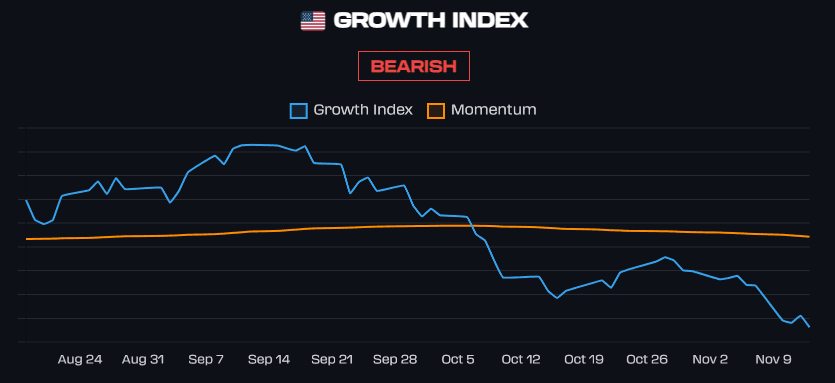

Markets have entered a stretch where every bounce feels fragile and every headline seems to hit harder than the last. Investors keep searching for signs that conditions are turning, yet our System has been flashing the same warning for weeks. Market Radar is firmly in the Risk-Off camp, and the evidence backing that stance grows clearer by the day. This shift began about a month ago when our macro regime model moved decisively into Risk-Off territory. Since then, Bitcoin has stumbled, and risk assets have taken on heavy volatility. A return to Risk-On is nowhere in sight, and conditions across the board look increasingly unstable. In this update, we break down what our System is signaling now and the risks that could surface if this regime holds.

The System & Inflation

Since our Risk-Off trigger on October 13, the growth outlook has only deteriorated. The ongoing government shutdown has deepened the uncertainty, leaving investors without key economic data such as Nonfarm Payrolls (NFP) and the Consumer Price Index (CPI) that could have provided a clearer read on the economy. With these reports delayed, markets have been left to navigate a fog of incomplete information.

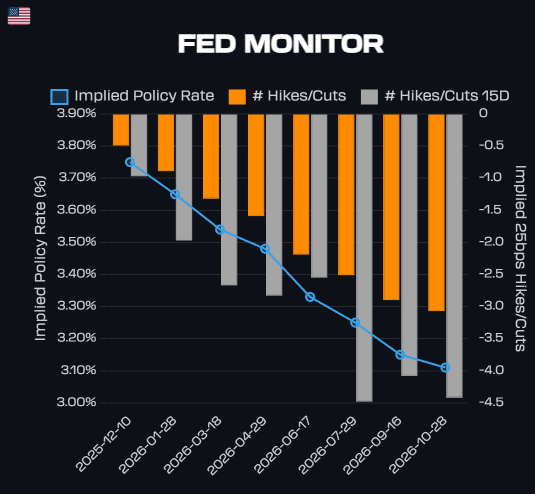

While growth signals remain weak, inflation pressures have proven more resilient than expected. This persistence has fueled a more hawkish shift in rate expectations, as traders reassess the likelihood of near-term easing. The probability of a December rate cut has fallen sharply, from near certainty two weeks ago to less than 50/50 odds today.

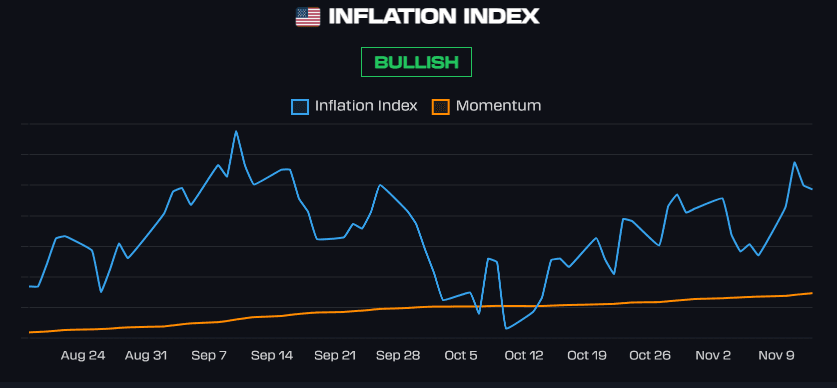

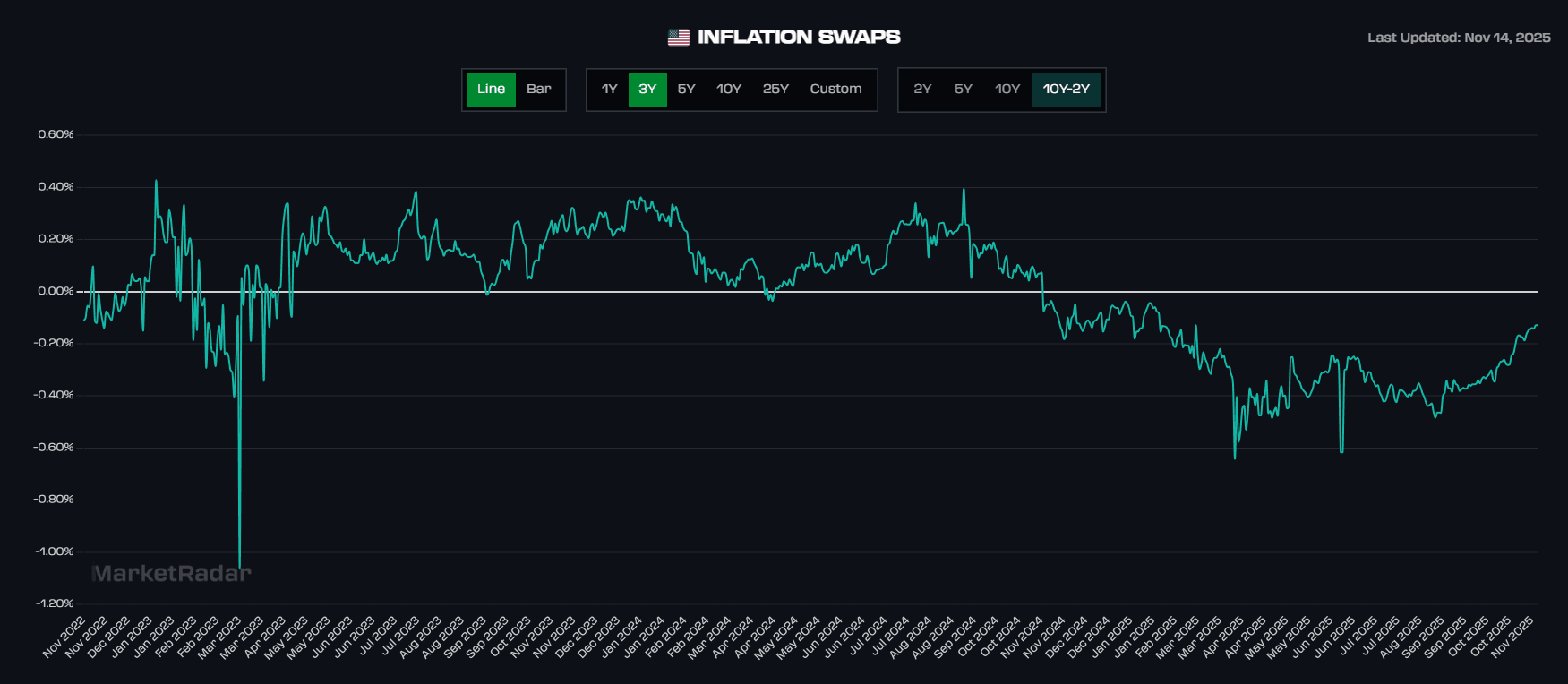

Inflation remains the central concern for the Federal Reserve, and the recent resilience in inflation impulses should not be taken lightly. That said, there are signs this momentum could be running out of steam. While we never base allocation changes solely on intuition, the inflation swap market continues to indicate a compression in inflationary risks. If this trend persists, it is likely to be reflected in the inflation indices soon.

We monitor the 10-year to 2-year inflation swap spread closely, as it provides valuable insight into both the level and structure of inflation pressures. When this spread turns negative, it indicates that near-term inflation pressures outweigh longer-term expectations, a sign of front-loaded inflation. Conversely, when the spread moves back into positive territory, it reflects a return to a more normal curve, where longer-term inflation expectations rise above short-term ones. A sustained shift toward a positive spread would suggest markets are regaining confidence that inflation will stabilize rather than accelerate in the near term.

If we had to guess, bonds appear to be waiting for confirmation from the inflation index that inflation impulses are indeed weakening, and for the swap curve to normalize with positive spreads. Based on current signals, it would not be surprising to see inflation narratives settle down in the near future, shifting the market’s focus back to growth. Historically, bonds perform best in those environments when inflation becomes an afterthought and the priority shifts toward cushioning growth risks.

Risk-Off Swans

We tend to simplify our market outlook into three broad regimes: Risk-On, Slowdown, and Risk-Off. During Risk-On phases, there’s little reason for concern; market dips are buyable, liquidity is abundant, and fundamentals often take a back seat to momentum.

It’s when markets transition into Slowdown or Risk-Off regimes that risks deserve close attention. Crises don’t emerge in Risk-On environments; they’re born when the market’s resilience begins to crack. As long as we’re outside of Risk-On, the probability of adverse events rises sharply. We’re not rooting for them, but it’s important to remember that black swans don’t appear when optimism rules, they surface when conditions tighten and complacency fades.

Artificial Intelligence

The market remains acutely sensitive to the artificial intelligence narrative, which continues to be the main force propping up equity performance. The concentration is clear, leading AI names such as GOOGL, NVDA, PLTR, and AAPL have been carrying the market higher while most other sectors struggle quietly in the background. This imbalance has created a top-heavy market structure, with valuations and expectations around AI growth stretched to levels where even a modest pullback in optimism could trigger a meaningful correction across indices.

🚀 Join the Radar Community

Get free access to MacroBase and notifications about new posts and updates.

What’s becoming increasingly concerning is that the productivity boost once attributed to AI, which used to be a tailwind for growth, as outlined in our Payrolls Don't Matter Anymore, now actually becomes a risk. In recent quarters, falling payrolls have been offset by gains in productivity, helping to stabilize GDP. However, productivity is a far less stable growth driver than employment, and sustaining recent gains will be challenging. If productivity growth begins to plateau or decline, the economy could lose its main support just as the labor market remains too weak to compensate.

We are not calling for a full-scale collapse of the AI bubble, but if such a scenario were to unfold, this is the type of regime where it would occur, a Risk-Off backdrop marked by stretched expectations and waning resilience. Even without a total unwind, a recalibration of expected productivity gains seems likely. That alone could be enough to produce growth shocks, given how reliant current market pricing has become on AI-driven optimism.

Hidden Labor Shocks

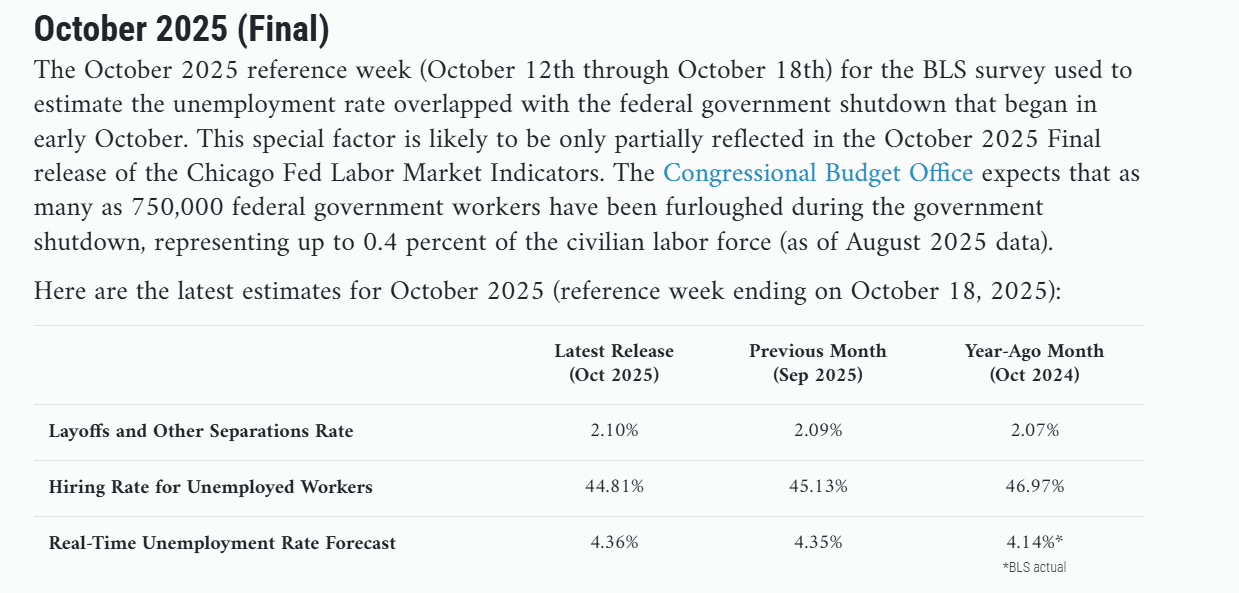

Labor dynamics remain clouded in uncertainty. With the government shutdown disrupting normal data releases, investors have now missed two consecutive employment reports. In their absence, markets have relied on ADP data and state-level jobless claim estimates to gauge national labor conditions, both of which provide an incomplete picture.

The last official Bureau of Labor Statistics (BLS) report, released in September for August data, showed an unemployment rate of 4.3%. Since then, the Chicago Fed’s real-time unemployment model has helped fill the gap, estimating that the jobless rate for the missed months has drifted only slightly higher, to roughly 4.4%. On the surface, this suggests stability in the labor market despite the shutdown.

However, the lack of verified data leaves room for surprise. If the official figures, once resumed, reveal a sharper rise in unemployment than the estimates suggest, markets could face a sudden repricing of growth expectations. With the economy already in a fragile Risk-Off regime, even a modest labor shock could act as a catalyst for renewed volatility.

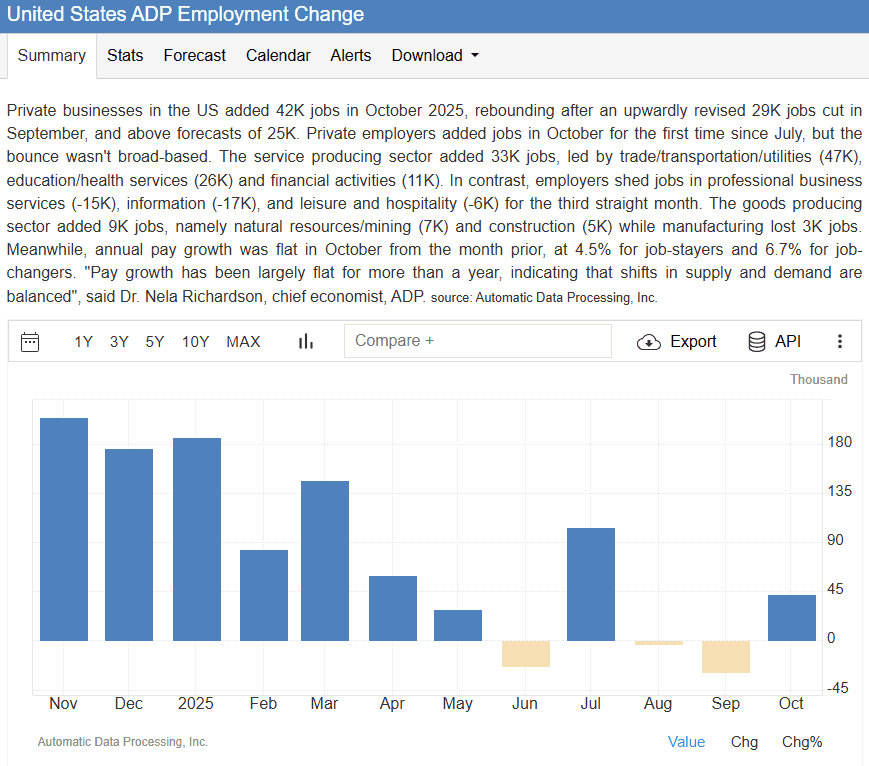

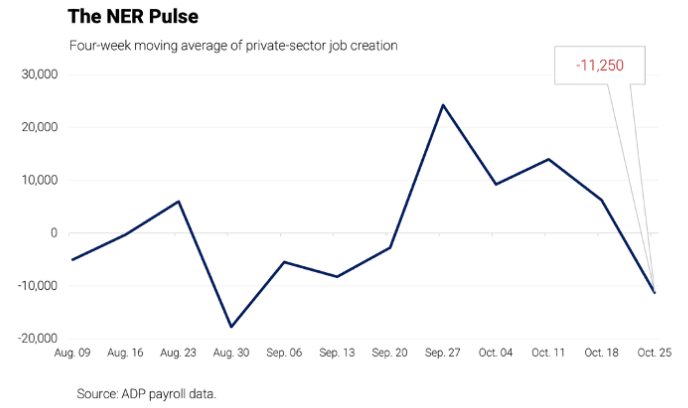

Another area of weakness that’s beginning to emerge comes from the ADP employment data. Because ADP is a private company, its release schedule has been unaffected by the shutdown, giving investors one of the few continuous labor indicators available. The latest monthly report showed a modest rebound in October, with 42,000 jobs added, a move back into positive territory after consecutive declines in August and September. While this may appear encouraging, several leading indicators suggest the rebound could be short-lived, with the potential for renewed softness in November.

Within the past month, ADP also began releasing a second payroll series, designed to capture week-over-week changes in employment based on a four-week moving average. This new measure complements their standard monthly release by providing higher-frequency insight into labor momentum. The latest estimate, ending October 25, 2025, showed that private employers shed an average of 11,250 jobs per week, indicating that job creation slowed significantly during the second half of the month.

Because this new series updates weekly, similar to jobless claims but with a short lag, it can serve as an early warning system. At roughly 11,000 jobs lost per week, or about 44,000 per month, it effectively offsets the entire October rebound shown in the last ADP report. While these figures remain preliminary, they warrant close monitoring in the coming weeks to see whether payroll estimates can stabilize and return to positive territory.

For now, this is a signal for caution rather than alarm. As we often remind readers, if the labor market were to roll over, it would likely do so in a Risk-Off regime, exactly where we are today. That is why we remain defensively positioned, recognizing that labor slippage, if it occurs, would find its footing in this environment.

Here Is How We're Managing Positions

MOST POPULAR

Unlock Premium Content

The remainder of this content is available to Radar members only. Subscribe to gain instant access.

$65/month

Billed annually at $780 (Save $120)

Access Models which boast 40%+ average yearly returns

Automated Portfolio Signals (RQF Strategy)

Live Calls with experienced traders

QuantBase Dashboard with macro regime models

DDAP TradingView Indicator

Real-time portfolio updates

Private Discord Channels

Lifetime Price Lock|Instant Access