5 MIN READ·OCTOBER 11, 2025

From Strength to Stagflation: Inside the Market’s Quiet Regime Change

It's So Over Anyone who’s been following our work knows we don’t chase headlines or panic at the first sign of a dip. We stay grounded in data, not emotion. Over the past few weeks, we’ve been waving quiet warning flags while still holding long exposure to ris

MR

CONTRIBUTOR · MARKET RADAR

It's So Over

Anyone who’s been following our work knows we don’t chase headlines or panic at the first sign of a dip. We stay grounded in data, not emotion. Over the past few weeks, we’ve been waving quiet warning flags while still holding long exposure to risk assets, because the signals were clear that something was shifting beneath the surface. The signals were clear—change was coming—and those tuned in early could see the turn long before the headlines caught up. We reiterated to members in our Discord that the Risk-On backdrop was losing momentum fast.

We’ll walk through exactly how our models detected weakness weeks in advance, the discretionary cues we shared with members, what our core signals are telling us now about risk assets, and what that likely means for the next major move in markets.

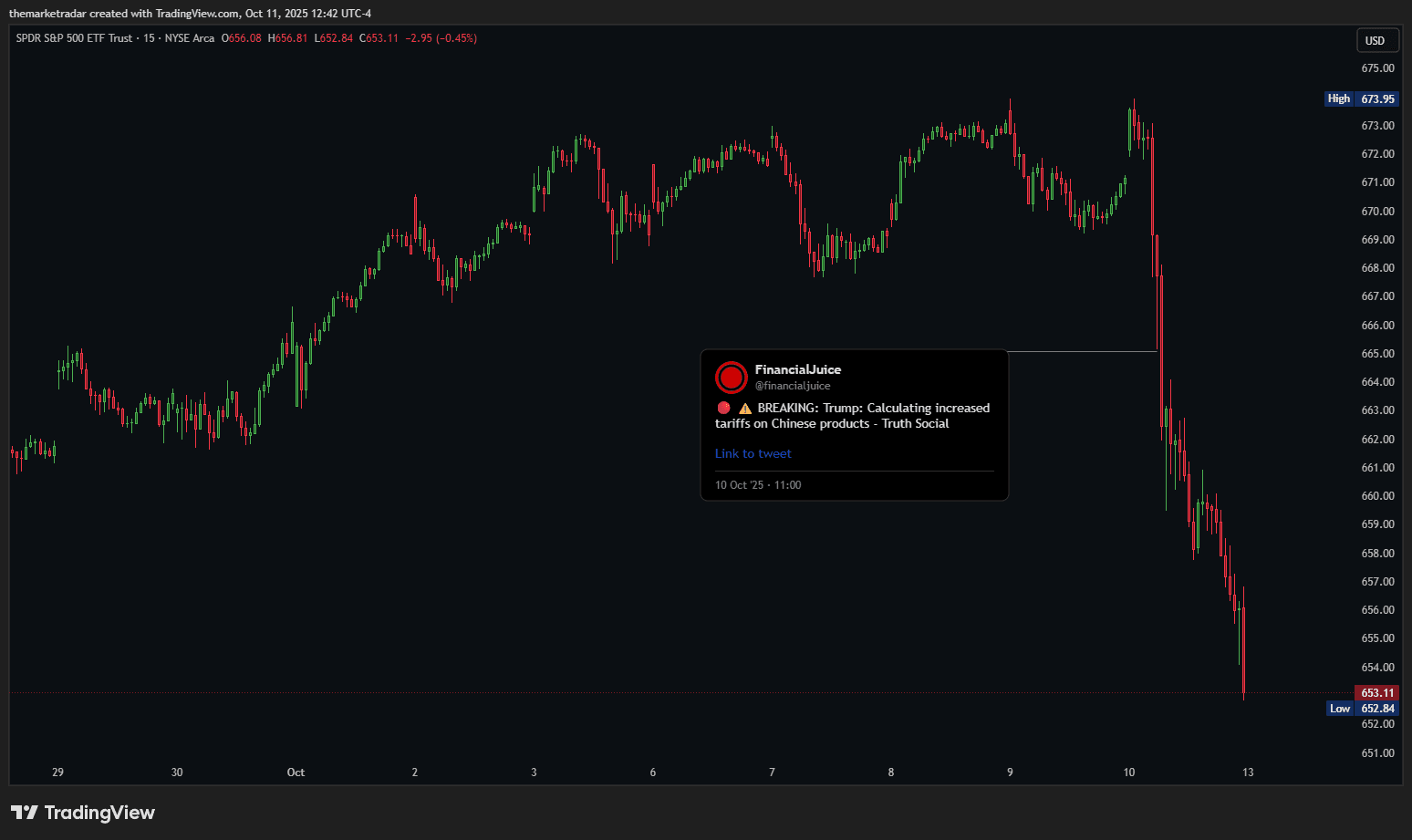

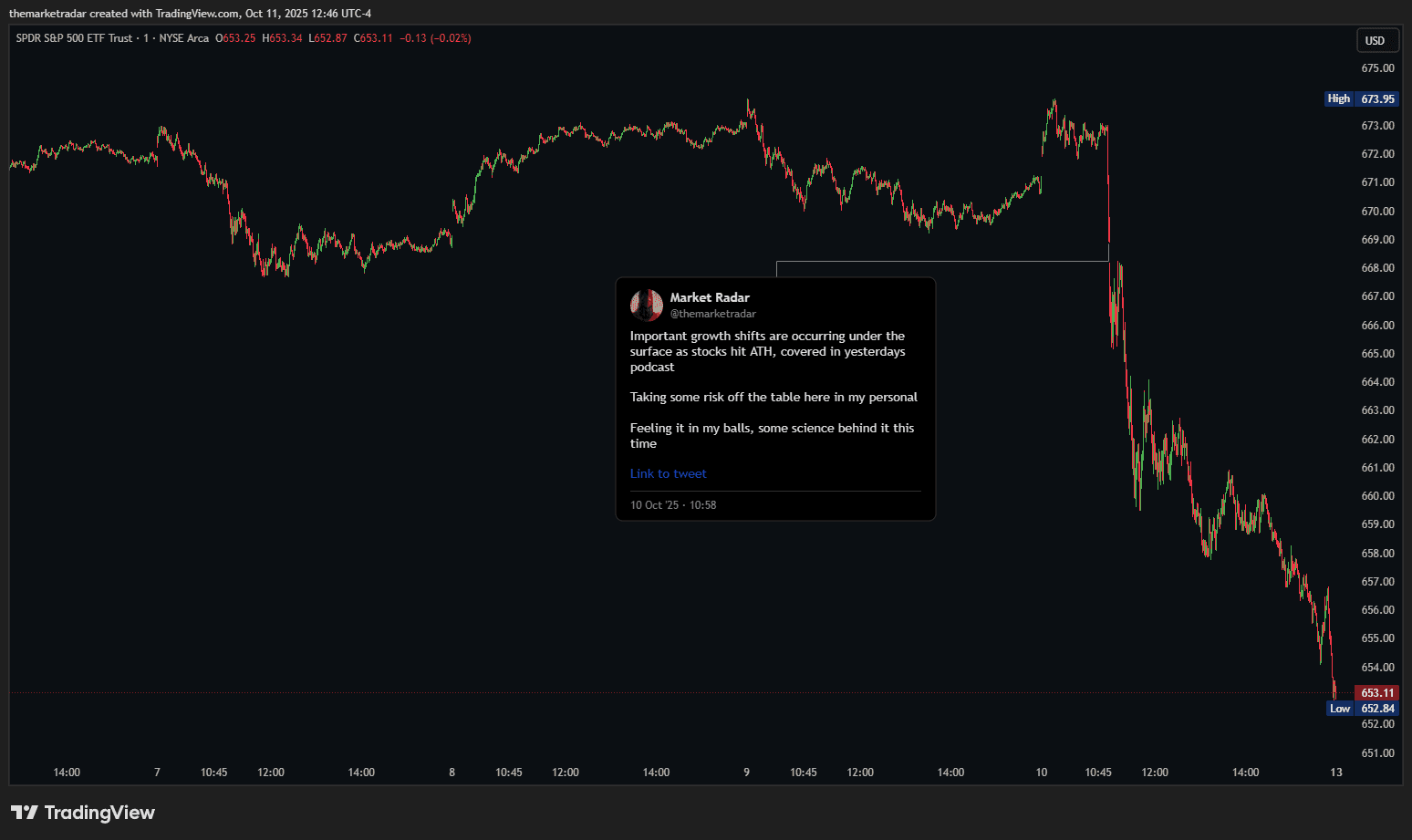

Before we go any further, it’s worth addressing Friday’s events. President Trump announced countermeasure tariffs on China in response to their export controls on rare earth minerals, triggering a sharp liquidity cascade across risk assets and crypto. Moves like this fall squarely into the category of “headline risk”, unpredictable shocks that no model or indicator can foresee. All he did was light the fuse on pressures that were already building up.

The reason I mention this is to make one thing clear: our growth impulse models had been trending lower well before Friday’s announcement. The decline in markets that followed had little to no influence on our current regime outlook. If anything, it simply added noise to a deterioration that was already in motion.

In our livestream earlier this week, we discussed that the market was nearing a potential transition out of Risk-On. By Thursday’s close, the data made that shift feel imminent, likely within a few days. Seeing the increased risk, we made a discretionary decision to trim some of our personal holdings early in Friday’s session. Coincidentally, this occurred just minutes before the tariff headlines hit, pure luck, as I’ll readily admit. But as we’ve been emphasizing to members for weeks, the signals pointing to weaker growth impulses have been lining up for some time.

Fortunately, our members were able to act on our early warnings by making simple leverage reductions, small adjustments that can materially cushion the kind of hit we saw on Friday.

Now, turning to RQF, our fully systematic model that is tracked daily in the QuantBase and accessible to members. The model remained long risk assets through Friday, meaning our public portfolio absorbed the drawdown alongside the market. However, the move was well within normal historical ranges of expectations, simply giving back a portion of last month’s gains while remaining positive on the year. However, things are changing now that we're no longer in Risk-On, more on that next.

What's Next For Risk

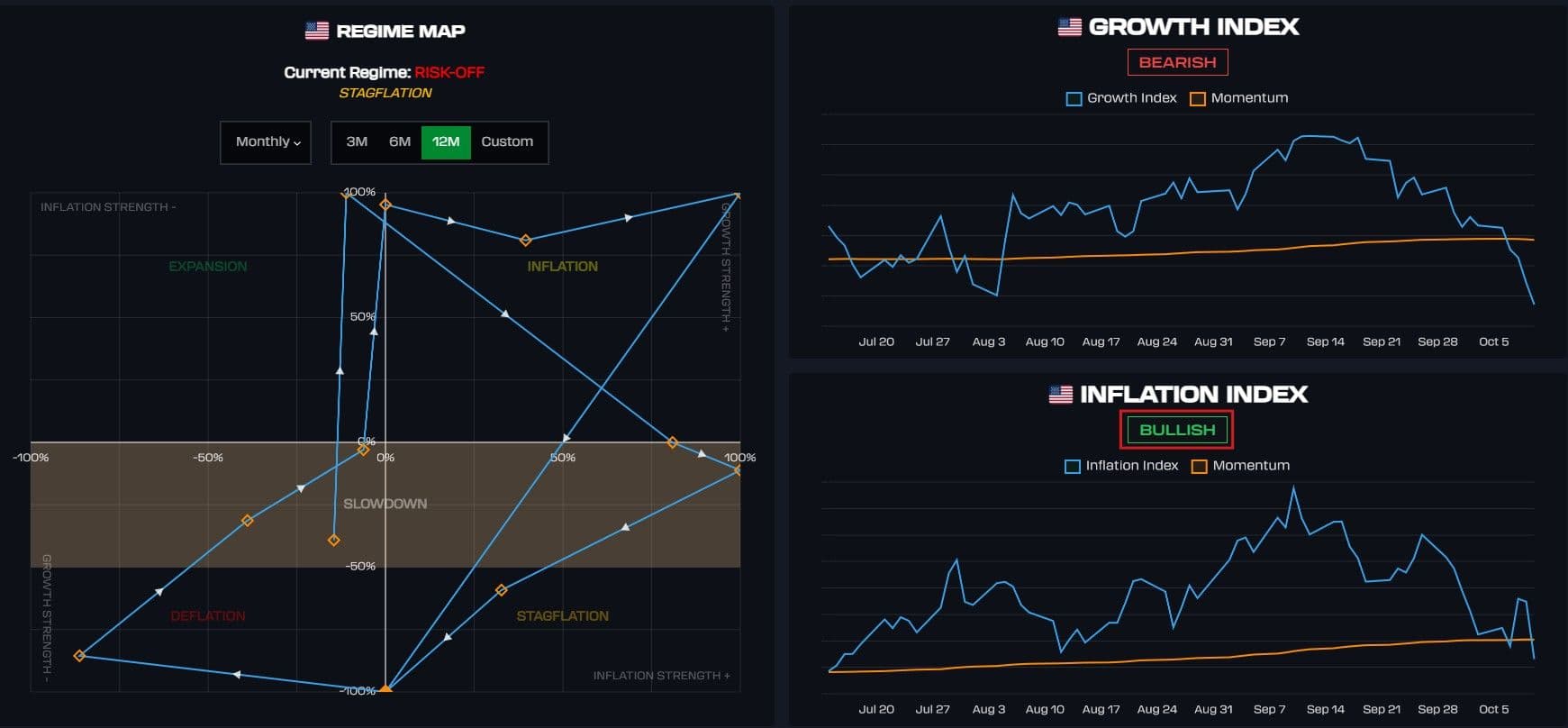

Now that you understand the system driving our regime signals, and that it was showing weakness well before Friday’s crash, it’s important to clarify that this shift isn’t a reaction to a single day of price action. As of now, we’ve officially pivoted out of Risk-On and into a Stagflation Risk-Off regime.

🚀 Join the Radar Community

Get free access to MacroBase and notifications about new posts and updates.

Stagflation comes from the fact that while growth impulses have turned lower, inflation impulses have not yet followed suit. However, early signs suggest a potential shift there as well, meaning a Deflationary Risk-Off regime could emerge in the near future.

It’s important to emphasize that our risk regimes are not recession calls. While we’ve now exited Risk-On, we at Market Radar DO NOT forecast recessions. Historically, recessions tend to occur during Risk-Off regimes, but not every Risk-Off period leads to one.

There’s also a meaningful chance that the current Risk-Off regime transitions into a Slowdown regime later this month. Such a shift would broaden the opportunity set, potentially reopening the door for more diversified equity exposure and renewed interest in Bitcoin. For that to occur, though, we’ll need to see growth impulses stabilize and avoid deteriorating much further from current levels.

For context, the last time we shifted to Risk-Off was on December 24th, 2025, and markets went on to decline more than 20% in the months that followed without a recession.

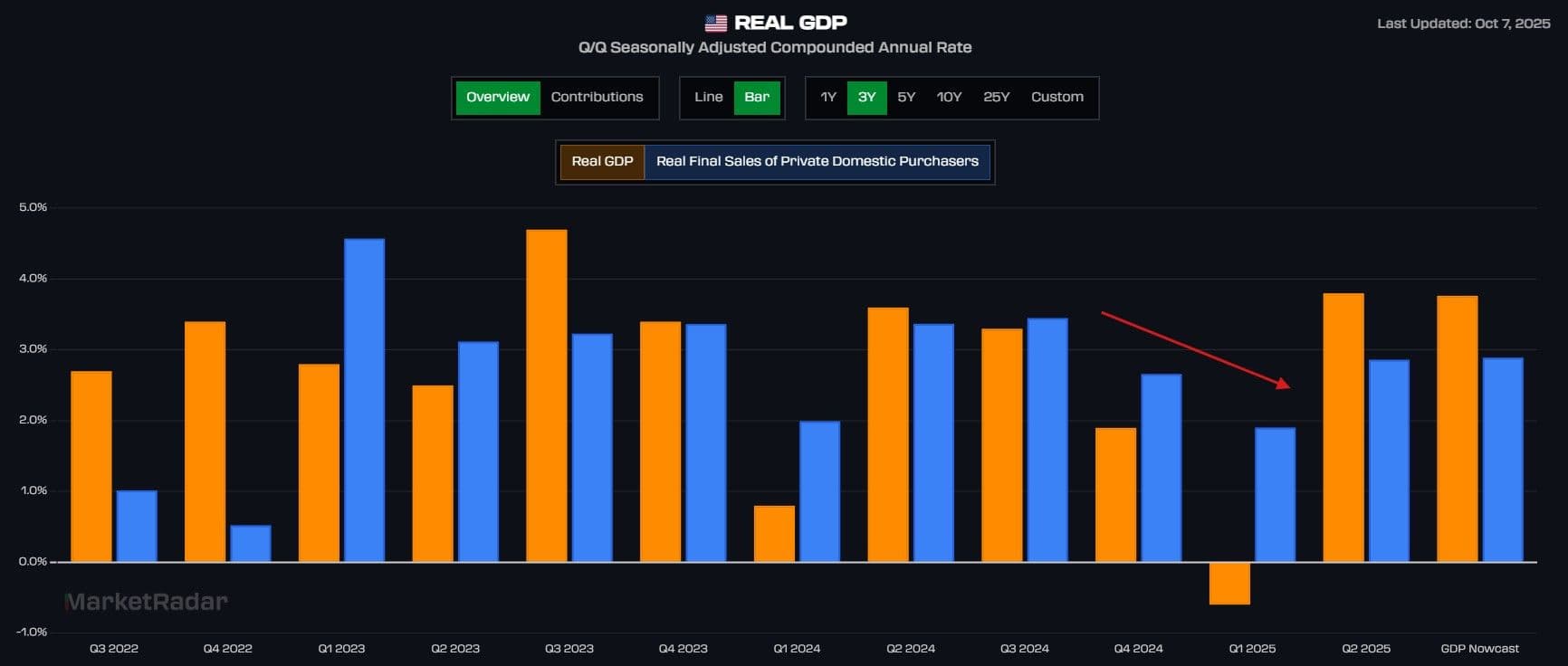

Now that we’ve entered Risk-Off, the next question is what catalysts could be driving it. A straightforward interpretation is that the System is sensing an environment where expectations have simply become too rich. After two exceptional quarters of growth following the weak Q1 print, which was largely import-driven due to tariffs but still showed marginal slowing of consumption, the bar has been set quite high.

We’re likely looking at back-to-back quarters of roughly 3% real GDP growth, which is impressive given the Q1 shock and all the tariff headlines. But that strength may now be working against the market. If Q4 comes in closer to 2% real growth, for example, still a solid number, but it might simply fall short of elevated expectations and sentiment, creating the backdrop our models are already detecting.

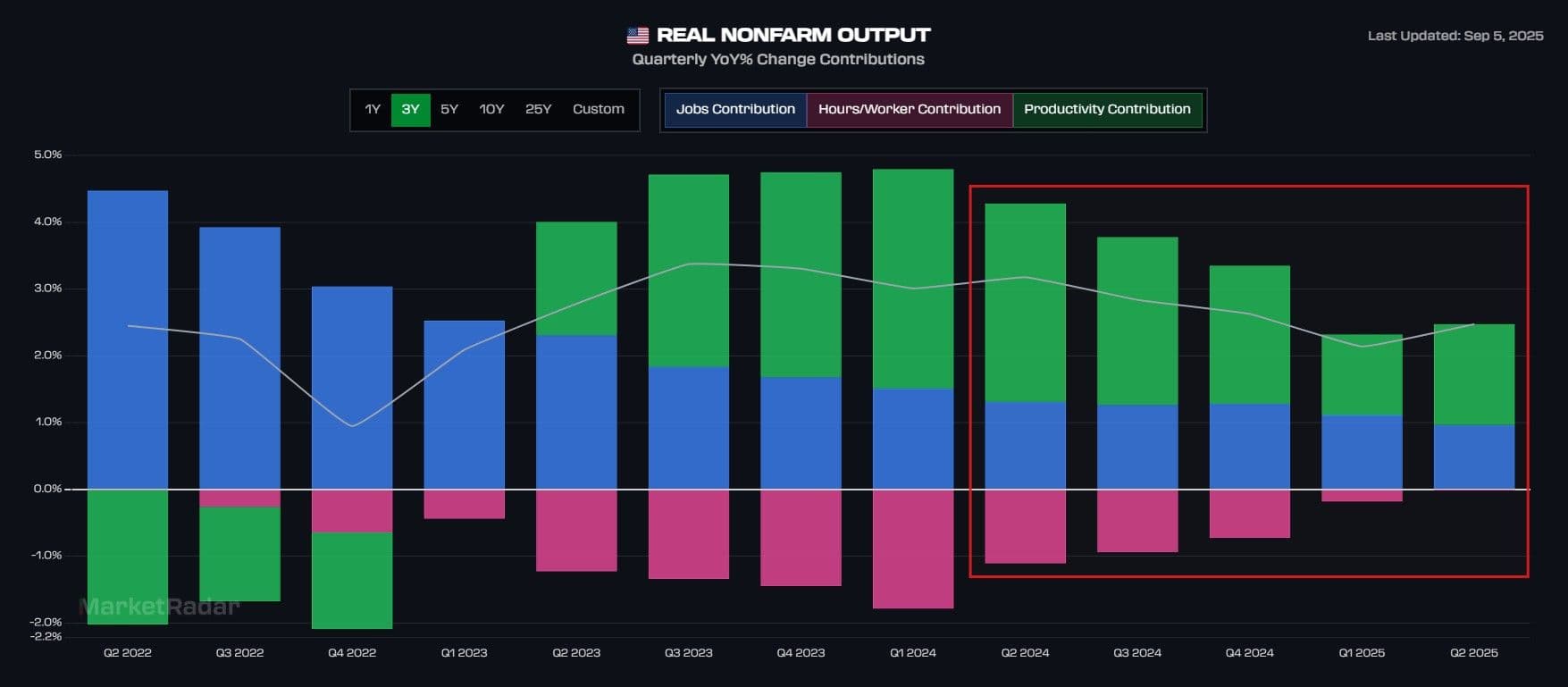

Another factor at play could be that recent growth has relied more on productivity gains than on payroll expansion. As shown here, payroll contributions now make up a smaller share of total real output. With the significant negative payroll revisions we’ve seen, it’s clear that earlier data overstated labor’s contribution. In other words, productivity has been carrying even more of the load than initially thought.

Essentially, the economy has been propped up by strong productivity enhancements, and even a modest slowdown in those gains could directly translate into weaker growth, given that payrolls and hours worked now carry less weight. This dynamic stems partly from advances in AI and immigration policy shifts, both of which have lowered the breakeven payroll rate. We covered this in a previous ledger note here. These dynamics make it easier for productivity to sustain growth, but it also means the economy has become increasingly sensitive to any pullback in productivity contributions going forward.

Positioning Changes - SELL RISK ASSETS

Since we're now in Risk-Off, it also means a positioning shift is coming for RQF. The rules for our positioning keep us allocated to positions with the highest conviction where BOTH our System (regime map shown above) and our trend model align. If one of them is off, conviction isn't there. Given we've left Risk-On, a change is coming as the tides turn. You can read more about our positioning rules in our guide.

With the regime officially shifting out of Risk-On, we now have a clear signal to SELL ALL RISK ASSETS. This will take place at Monday’s close, in line with our standard process. The timing has nothing to do with Friday’s volatility; all updates are executed at the close of the following session by design.

Here's what we're buying after selling risk assets on Monday...

MOST POPULAR

Unlock Premium Content

The remainder of this content is available to Radar members only. Subscribe to gain instant access.

$65/month

Billed annually at $780 (Save $120)

Access Models which boast 40%+ average yearly returns

Automated Portfolio Signals (RQF Strategy)

Live Calls with experienced traders

QuantBase Dashboard with macro regime models

DDAP TradingView Indicator

Real-time portfolio updates

Private Discord Channels

Lifetime Price Lock|Instant Access