8 MIN READ·JANUARY 12, 2026

What Happens When the Bear Case Fails to Escalate

The Macro Update This is the moment investors get trapped: the risks are still real, but the market stops acting as if it cares. It has been nearly three months since our Risk-Off call, which is long enough for two things to be true at the same time. The risks

MR

CONTRIBUTOR · MARKET RADAR

The Macro Update

This is the moment investors get trapped: the risks are still real, but the market stops acting as if it cares. It has been nearly three months since our Risk-Off call, which is long enough for two things to be true at the same time. The risks we laid out in October were real, and they deserved respect. But if those risks are not getting worse, then the market is not obligated to keep behaving as if it's in danger. That is the part people miss. Markets do not stay defensive because a narrative was once compelling. They stay defensive because the evidence keeps stacking.

Before we go further, read the original Ledger if you have not: When Tailwinds Disappear and the Headwinds Start to Bite. The reason we are revisiting it now is not that we are bored, and it is not because we want a new story. It is because the last few months were unusually difficult to judge in real time. From October 1 through November 12, a federal government shutdown disrupted economic data collection and delayed releases that people treat as the gold standard, including CPI and other major BLS series. The market spent a meaningful stretch trading in a fog, and in Slowdown or Risk-Off conditions, fog has a way of making everything feel worse than it is.

That fog is finally lifting, and the backlog is clearing, which means we can do the only thing that matters: run the October thesis back through the tape and the data, and see what held up, what softened, and what is quietly running out of fuel. Our macro regime model gives us the direction to build from, but the job is always the same. We have to keep the narrative on a leash and let reality lead.

The Battle of Risk-Off

Risk-Off is not a mood swing. It is a regime where the market stops giving the benefit of the doubt. In those environments, rallies are treated as opportunities to reduce exposure, not add it. Weakness spreads instead of staying contained, leadership narrows instead of rotating, and anything crowded starts to feel heavy. You do not need to be told Risk-Off is here. You feel it because the tape stops forgiving mistakes.

The confusion comes from the fact that Slowdown can masquerade as Risk-Off for long stretches. You still get ugly days. You still get unsettling headlines. Volatility stays elevated enough to keep everyone on edge. But the market never fully commits to the downside. Instead of a clean break, you get hesitation. Instead of follow-through, you get chop. That distinction matters because real Risk-Off regimes do not linger politely. They accelerate.

Since October, we have lived in that gray area. The market has repeatedly tested whether it wants to tip into something worse, and each time it has stalled. That does not mean risk disappeared, but it does mean the burden of proof stayed on the bearish case. In a true Risk-Off environment, the original pressure points do not just show up once. They compound. They spread. They start feeding on each other.

So the only way to approach this update honestly is to go back to those pressure points and see which ones actually gained traction. Not which ones sounded scary, but which ones followed through. The first place to start is the one narrative that has carried more weight than any other over the past year.

Artificial Intelligence

When we closed out the last Ledger, we were very deliberate about how we framed AI risk. We were not calling for a collapse. But if the AI narrative was going to crack, a Risk-Off backdrop was exactly the environment where it would happen. Expectations were stretched, positioning was crowded, and the entire growth outlook had become increasingly reliant on future productivity gains showing up on schedule.

That test arrived quickly.

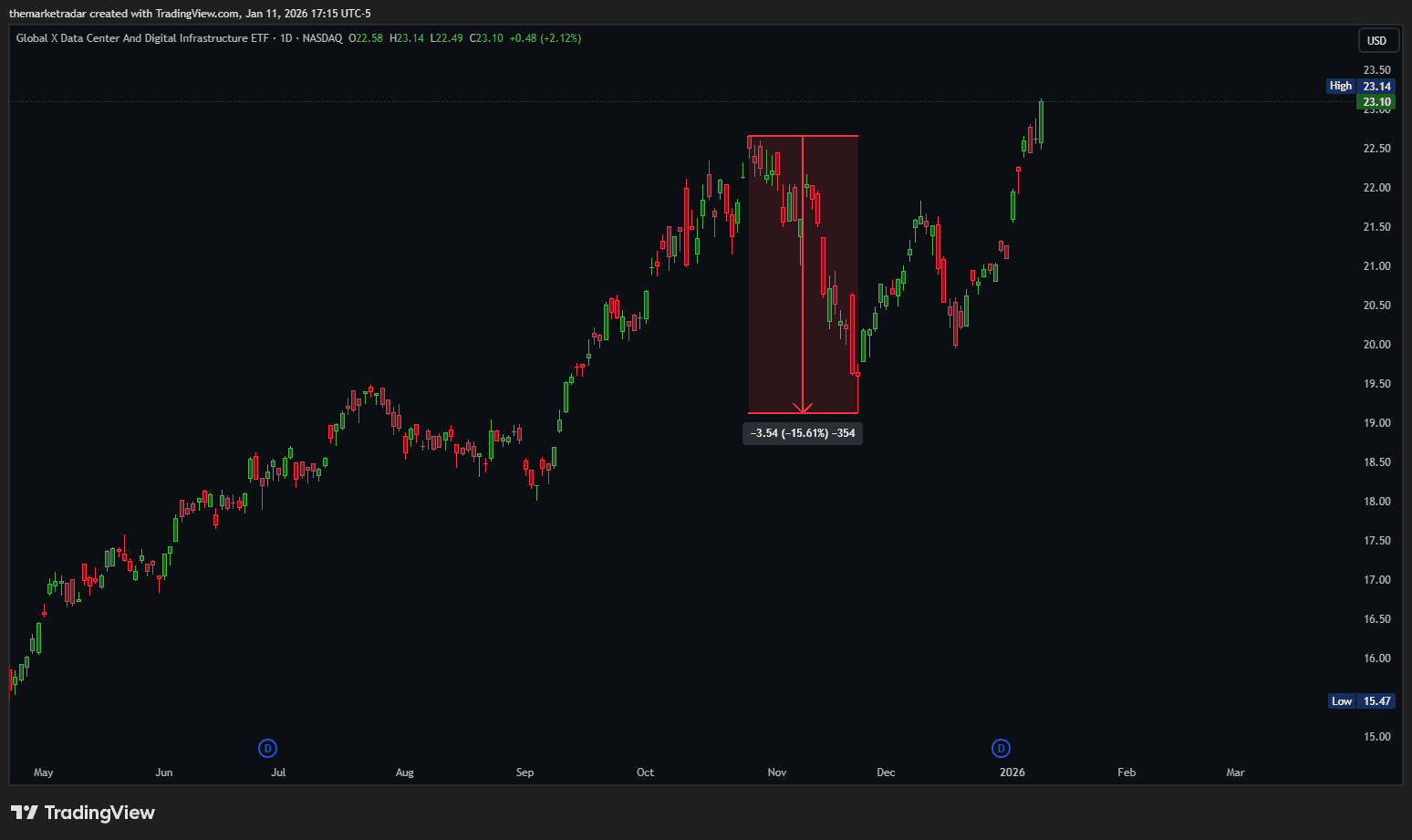

CapEx concerns surfaced. Infrastructure spending came under scrutiny. Several high-profile names tied to data centers and digital infrastructure saw sharp drawdowns, and for a moment, the market looked like it might turn a healthy reset into something more structural.

This chart tells the important part of the story. The drawdown was real. The volatility was uncomfortable. But the unwind never materialized. Instead of breaking down and staying broken, the group stabilized, churned, and eventually pushed back toward highs. That is not how fragile narratives behave when the macro backdrop is truly hostile.

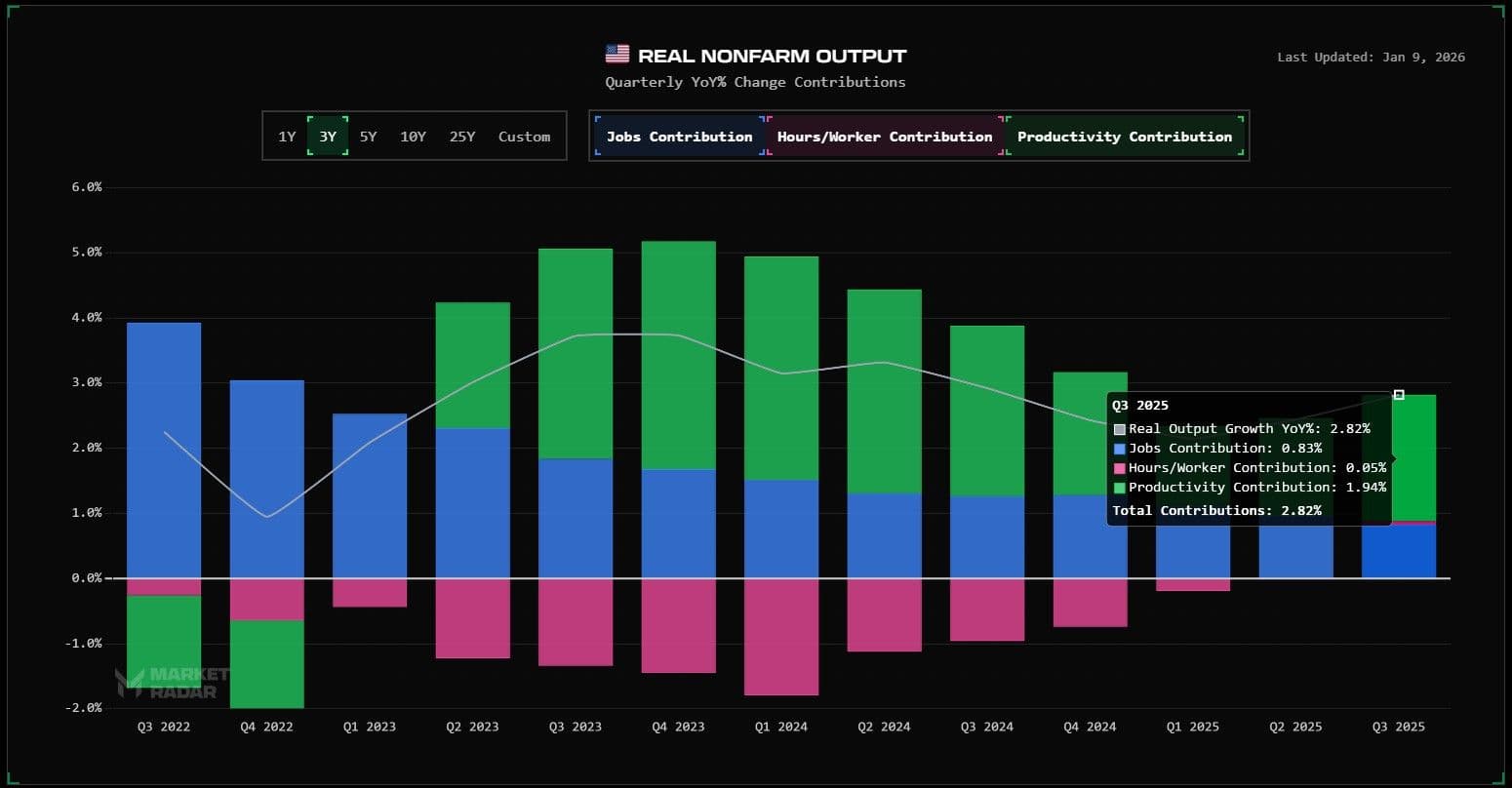

The bigger risk we outlined in October was not about price action alone. It was about the economy losing its main offset. Falling payroll growth had been masked by rising productivity, much of it tied to AI-driven efficiency gains. If productivity rolled over at the same time labor softened, growth would have lost its buffer.

That is not what the data showed. Recent productivity releases confirmed that output per hour continued to rise, while unit labor costs eased. In other words, the very mechanism we feared could fail ended up doing the opposite. Instead of becoming a headwind, productivity remained a stabilizer with nearly all the output growth in the quarter coming from productivity increases. This does not mean AI is risk-free. It means the specific failure mode that would have validated a deeper Risk-Off regime did not occur. The market pressured the AI narrative, questioned it, and then backed off. That is information. Once that pillar held, the focus naturally shifted to the next one.

Hidden Labor Shocks

🚀 Join the Radar Community

Get free access to MacroBase and notifications about new posts and updates.

If AI was the narrative pillar, labor was the structural one. This is the part of the economy that turns slowdowns into something more serious, and it is why labor always matters most in Risk-Off discussions, even when markets pretend otherwise.

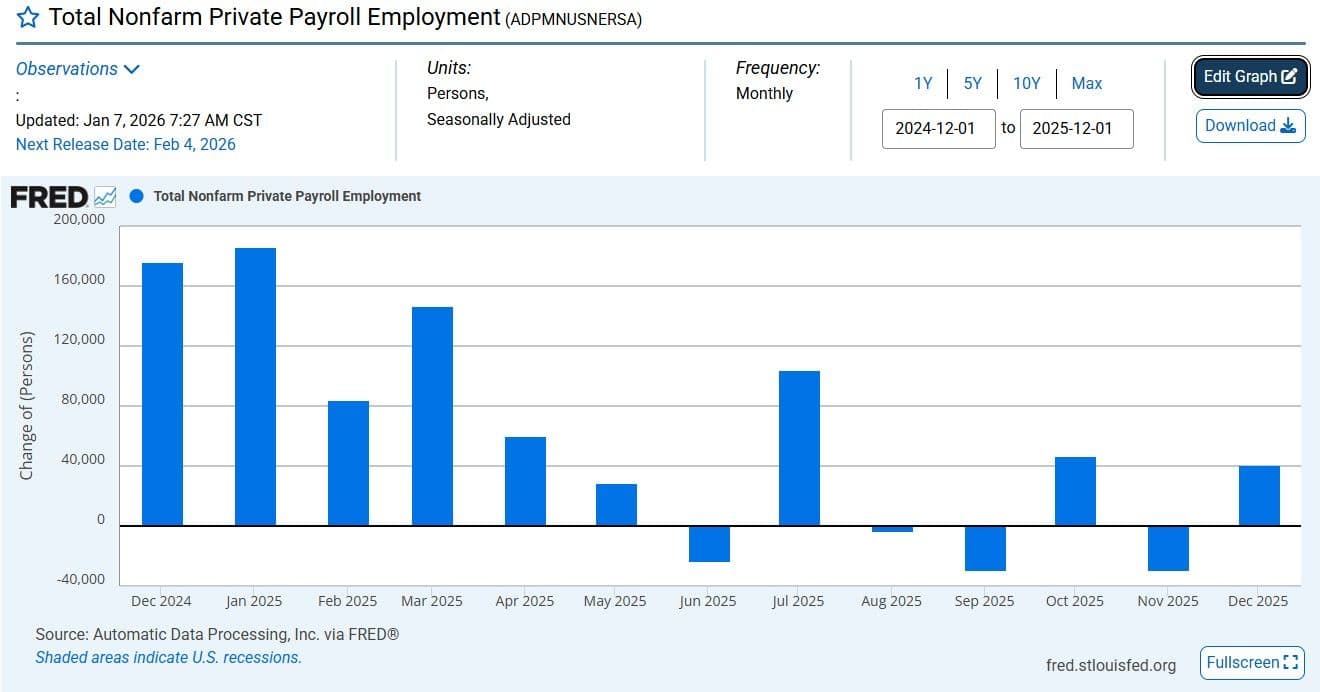

Back in October, the concern was not that hiring was cooling. Cooling is normal. The concern was that cooling could turn into something reflexive, where weaker job growth feeds softer consumption, which feeds weaker earnings, which feeds more caution from employers. That is how economies cascade, and it is why we were watching labor so closely. The timing could not have been worse. The government shutdown distorted the data flow right as the labor market was losing momentum, which made it difficult to separate signal from noise. ADP prints weakened. Revisions muddied the picture. Markets were left reacting to fragments, and fragments tend to feel worse than reality, especially when sentiment is already fragile.

Once the backlog began clearing, the picture became less dramatic and more frustrating. Hiring did slow, but it did not cascade. Weak months were followed by rebounds. Negative prints failed to turn into a trend. Even where payroll growth disappointed, unemployment did not surge in the way it typically does when the labor market is breaking down.

This chart captures the story better than any headline. Strong early-year momentum gave way to softness, then chop, then signs of stabilization. That is not a healthy labor market, but it is not a collapsing one either. It looks like an economy running at stall speed, not one falling off a cliff. That distinction matters more than people want to admit. In real Risk-Off regimes, labor does not stall quietly. It rolls over decisively. Job losses accelerate, confidence erodes quickly, and recession signals begin feeding on themselves. We simply did not get that feedback loop.

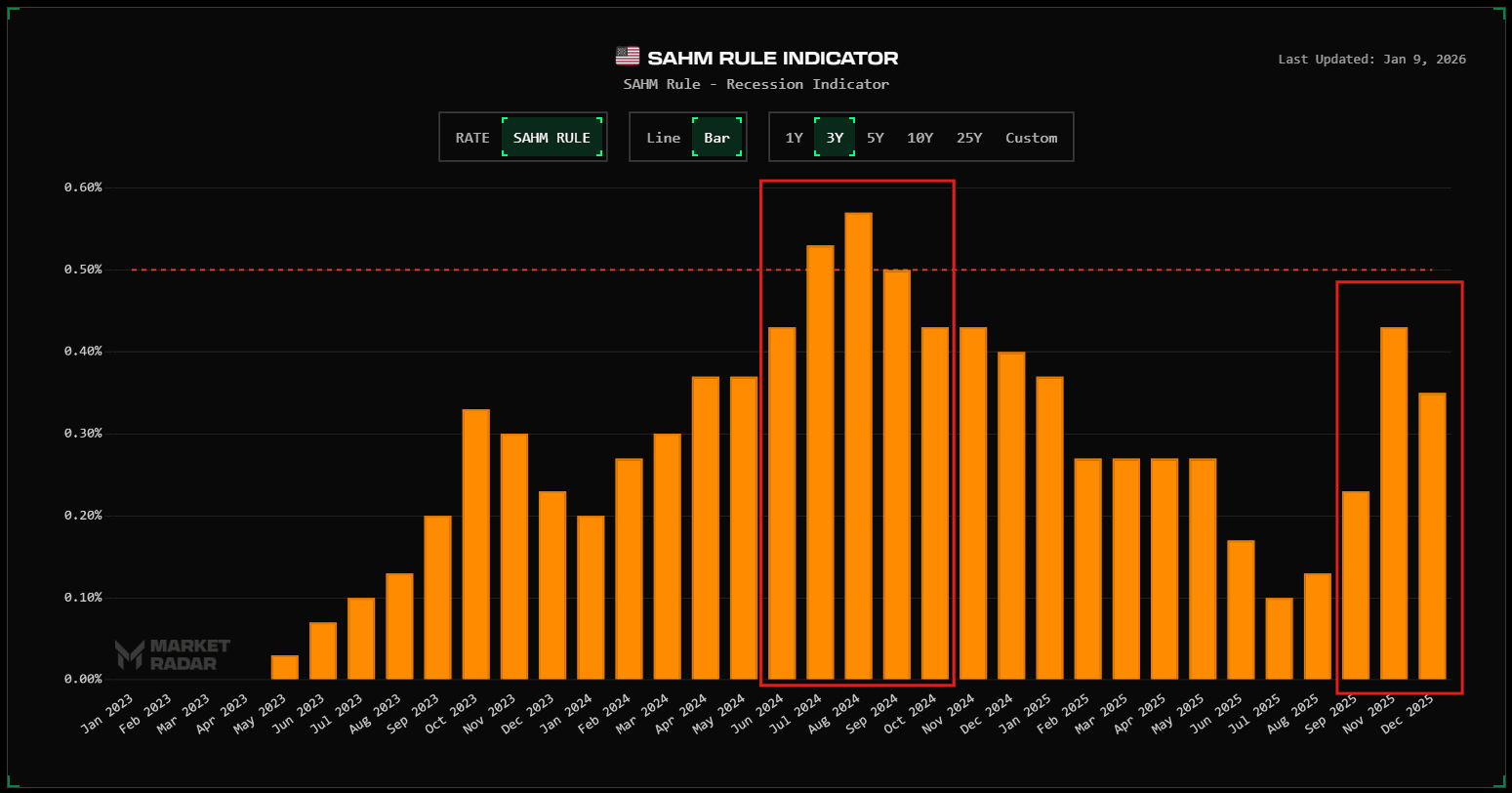

The Sahm Rule is also a good example of this tension. It moved higher and triggered understandable concern, but it never accelerated the way it has in past downturns. Instead of building momentum, it plateaued. Elevated, yes. Escalating, no.

That does not mean labor is suddenly strong, and it does not mean risk is gone. It means the labor market failed to deliver the confirmation that a deeper Risk-Off regime required. The slowdown showed up, but the break did not.

And when labor refuses to break, it forces the market to reassess everything built on top of that assumption.

Pulling Risks Together

Stepping back, this is where the story starts to matter more than any single data point.

What we are watching does not look like a late-cycle economy running out of ideas. It looks more like an economy in the early innings of a structural shift, with all the messiness that comes with it. In that sense, the current setup has more in common with the 1920s than with a typical post-cycle slowdown. Back then, the assembly line did not produce an infinite straight line higher in markets. It produced bursts of optimism, periods of excess, sharp resets, and then a much larger trend that only became obvious in hindsight.

Artificial intelligence fits that pattern almost uncomfortably well. Adoption is still early, uneven, and experimental across most sectors. Companies are only beginning to understand how to embed AI into workflows beyond surface-level use cases. Over time, that experimentation turns into process, and process turns into productivity. That is not a quarterly story. It is a multi-year one.

What we saw in Q4 2025 was not the failure of that trend. It was a familiar side effect of it. Expectations ran ahead of reality, pricing got stretched, and the market forced a reset. That does not negate the underlying force pushing forward. It reminds you that even transformative technologies move in waves, not straight lines.

This is where labor and AI intersect in a way that often gets missed. Productivity gains allow the economy to absorb slower hiring without immediately breaking. That is exactly what we have been seeing. Labor has cooled, but it has not cracked, because efficiency gains are still doing real work under the surface. That combination is uncomfortable for both bulls and bears. It denies the bear case the collapse it needs, and it denies the bull case the clean acceleration it wants.

Inflation sliding into the background only sharpens that tension. As inflation pressures ease, policy constraints loosen. That does not guarantee rate cuts or easy money tomorrow, but it does change the asymmetry. In an environment where growth remains acceptable and productivity continues to improve, disinflation becomes a release valve, not a warning sign.

This is the mistake people make when they treat every pocket of weakness as a verdict. Structural shifts do not eliminate volatility. They create it. You get moments where expectations outrun adoption, markets correct, and narratives flip bearish just long enough to reset positioning. Then the larger trend quietly resumes.

That is the backdrop coming out of the last few months. AI did not break. Labor did not spiral. Inflation stopped acting like a constraint. The risks that mattered were tested, and instead of compounding, they stalled. That does not mean the path forward is smooth. It means the dominant forces shaping it are still intact.

Here Is How We're Managing Positions

MOST POPULAR

Unlock Premium Content

The remainder of this content is available to Radar members only. Subscribe to gain instant access.

$65/month

Billed annually at $780 (Save $120)

Access Models which boast 40%+ average yearly returns

Automated Portfolio Signals (RQF Strategy)

Live Calls with experienced traders

QuantBase Dashboard with macro regime models

DDAP TradingView Indicator

Real-time portfolio updates

Private Discord Channels

Lifetime Price Lock|Instant Access